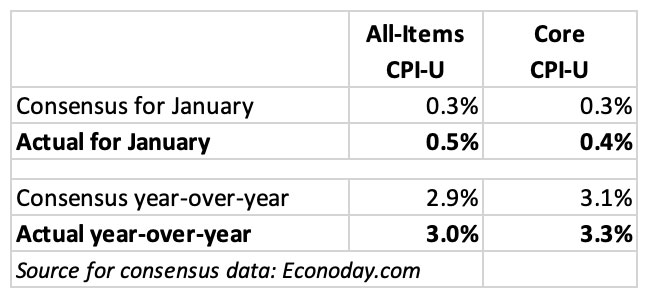

All-items and core inflation both rose much higher than expectations.

By David Enna, Tipswatch.com

The January inflation report, just released by the Bureau of Labor Statistics, demonstrated that U.S. inflation is far from tamed. This was not good news.

There is no silver lining here. Seasonally-adjusted all-items inflation increased 0.5% for the month and 3.0% for the year, both above expectations. Core inflation, which removes food and energy, rose 0.4% for the month and 3.3% for the year, also above expectations. Annual inflation by both measures increased over December levels.

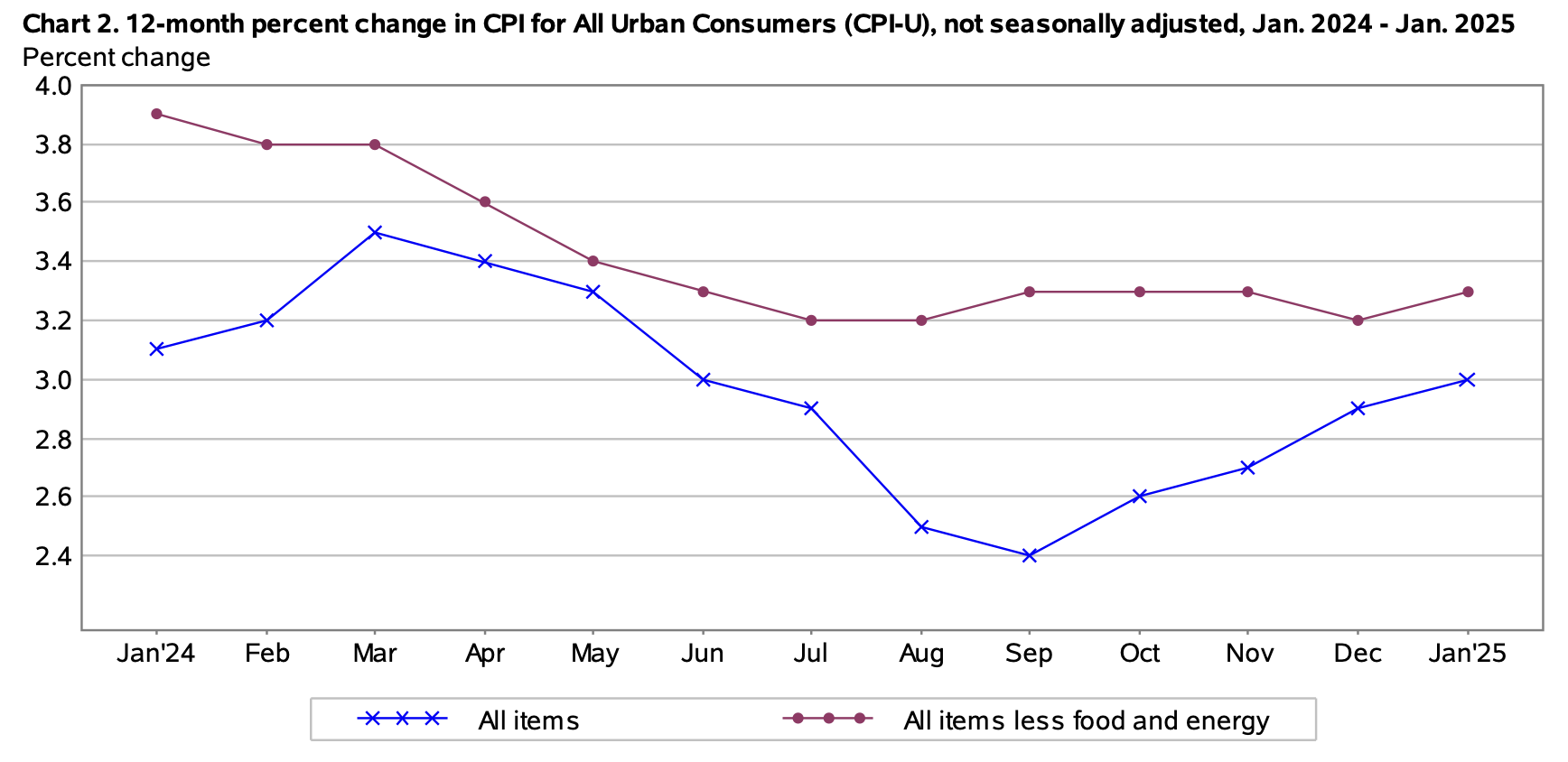

This one graph, tracking the year-over-year trend line, shows it all, with all-items inflation steadily rising higher since fall 2024 and core remaining stubbornly above 3.0%:

The BLS noted that shelter costs increased 0.4% for the month and 4.4% for the year, a major factor in the overall increase. And gasoline prices rose 1.8% for the month, after rising 4.0% in December. Food at home prices increased 0.4% for the month and are now up 2.5% for the year. The price of eggs, for those curious, rose 15.2% for the month. It’s time to switch to breakfast cereal, where prices declined 3.3% for the month.

The BLS said prices were up across all major categories except apparel, which saw costs decline 1.4%.

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which adjusts principal on TIPS and sets future interest rates for I Bonds.

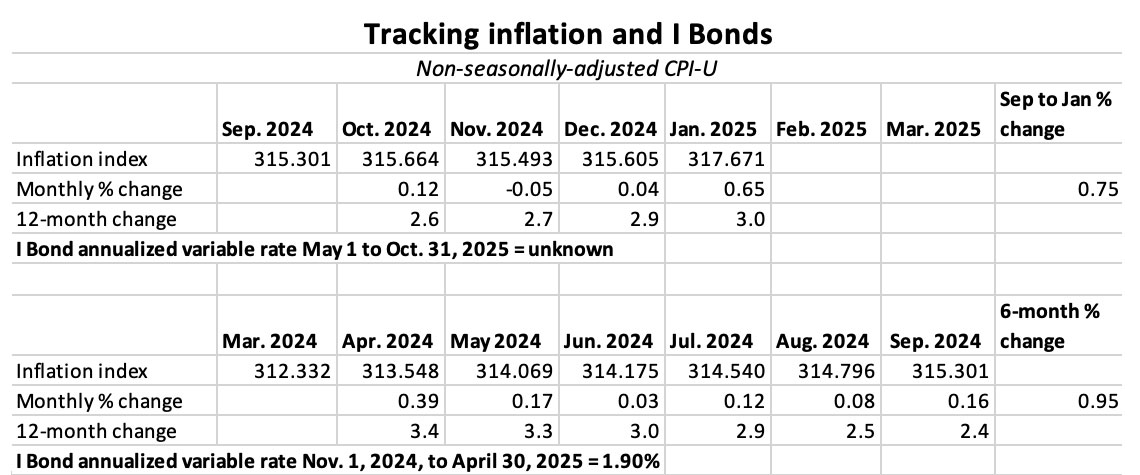

The BLS set the January inflation index at 317.671, a sharp increase of 0.65% for the month. A high number was expected, because non-seasonally adjusted inflation runs higher than adjusted inflation from January to June. But 0.65% was higher than I expected.

For TIPS. The January inflation number means that principal balances for all TIPS will increase 0.65% in March, after rising just 0.04% in February. For the year ending in February, principal balances will have increased 3.0%.

For I Bonds. January is the fourth of a six-month string that will determine the I Bond’s new variable rate, which will be reset on May 1 and eventually roll into effect for all I Bonds. At this point, with two months remaining, inflation has increased 0.75%, which translates to a variable rate of 1.50%. The next two months are likely to push the variable rate up to around 3.0%, or higher. We’ll have to wait and see.

Here are the numbers so far:

What this means for future interest rates

The January surge in inflation (which has been a January trend for several years) supports the Federal Reserve’s decision to hold interest rates at current levels, and probably means no rate-cutting is coming for many months.

This is from Bloomberg this morning:

Seema Shah, chief global strategist at Principal Asset Management, says these numbers are “very uncomfortable” for the Fed. Here’s her view: “If this persists into the next few months, inflation risks may become too heavily weighted to the upside to permit the Fed to cut rates at all this year.”

And this:

The danger is that this elevated inflation reading and the news headlines it produces will add to inflation expectations. They had already been ticking up amid all the discussion of tariff hikes from the Trump administration.

In essence, it would make no sense for the Federal Reserve to make any rate decisions (or even signals) for several months. We are on pause and the potential for rate increases is slightly rising.

I am writing this morning from Santiago, Chile. That is the reason for the abbreviated analysis. And it is time for my vacation to continue!

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UrsaTaurus, I have been contemplating similarly, buying long without the expectation of holding to maturity (I will be dead). I…