But … no clarification yet on delivery of gift-box purchases.

By David Enna, Tipswatch.com

The U.S. Treasury just announced a 1.20% fixed interest rate for the Series I Savings Bond, creating a new six-month composite rate of 3.11% for purchases from November 2024 through April 2025.

No surprises there. This is exactly what I was predicting in my preview article posted earlier this week.

At this point, it appears the Treasury is holding the annual purchase cap at $10,000 per person per year. But it has not yet posted the full news release on the rate change. That could be coming tomorrow.

Nov. 1 update: Here is the Treasury announcement, which confirms the fixed and composite rates.

In addition, Treasury has issued no clarification on delivery of I Bonds held as gift-box purchases. In a recent email, TreasuryDirect had asked investors to deliver those gifts “as soon as possible.” The site continues to say this:

Savings bonds you purchase as gifts aren’t included in your annual limit. The purchase amount of electronic savings bonds you transfer, deliver as gifts, or de-link to another TreasuryDirect account holder is applied to the annual purchase limit of the recipient. It is applied in the year the bonds are delivered to the recipient’s account.

In recent days, some callers to TreasuryDirect have received advice to 1) go ahead and deliver all gift-box savings bonds to recipients, and 2) face a temporary ban on future purchases because of those deliveries. The still-active statement from the Treasury’s Research Center contradicts that feedback.

So … we are still awaiting clarification. It could be that changes are coming January 1, so we may need to wait for detailed information.

The I Bond rate reset

The interest rate on a Series I Savings Bond changes every six months, based on inflation. The rate can go up, or as in this case, down. The overall rate is calculated from a fixed rate and an inflation-adjusted variable rate. The fixed rate never changes. The variable rate is reset every six months and so is the composite rate.

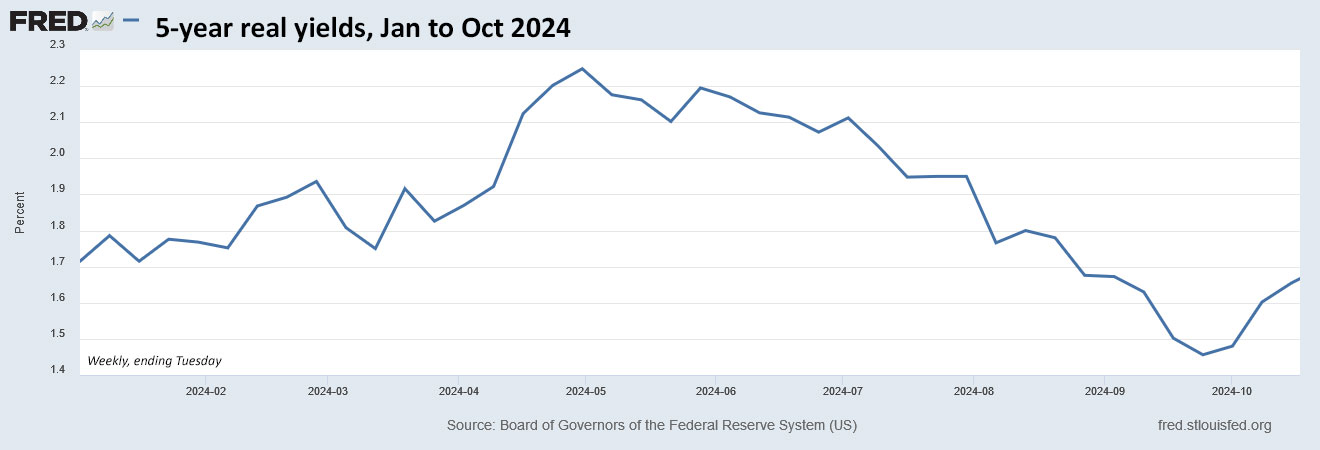

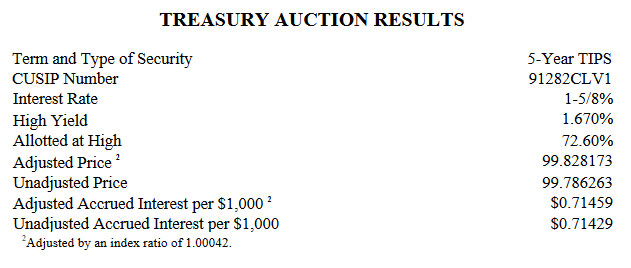

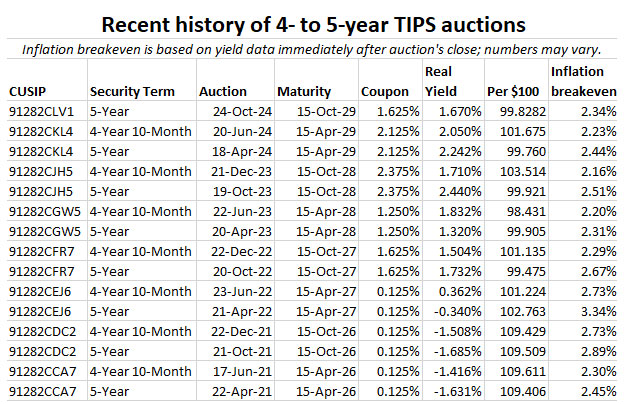

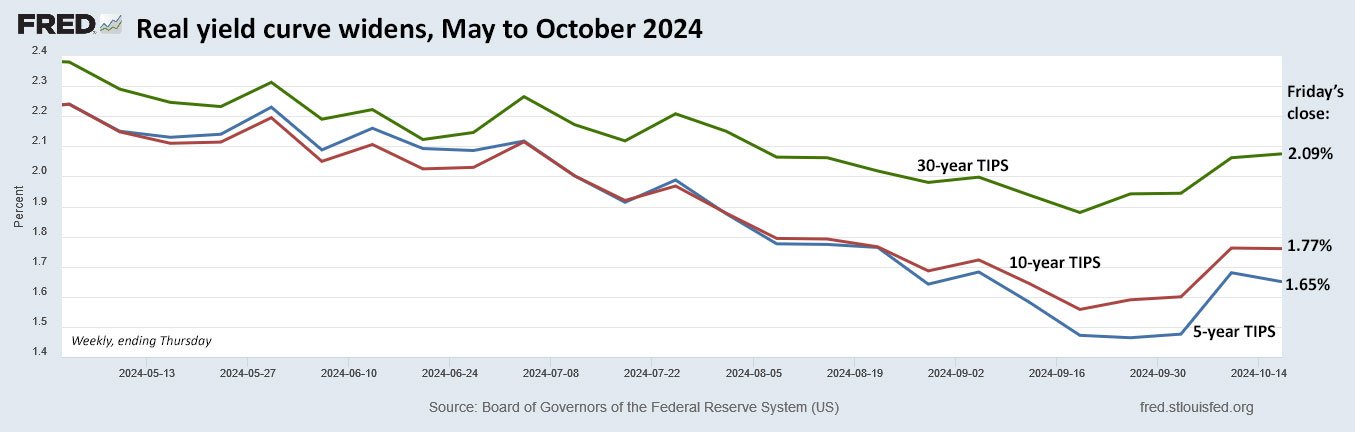

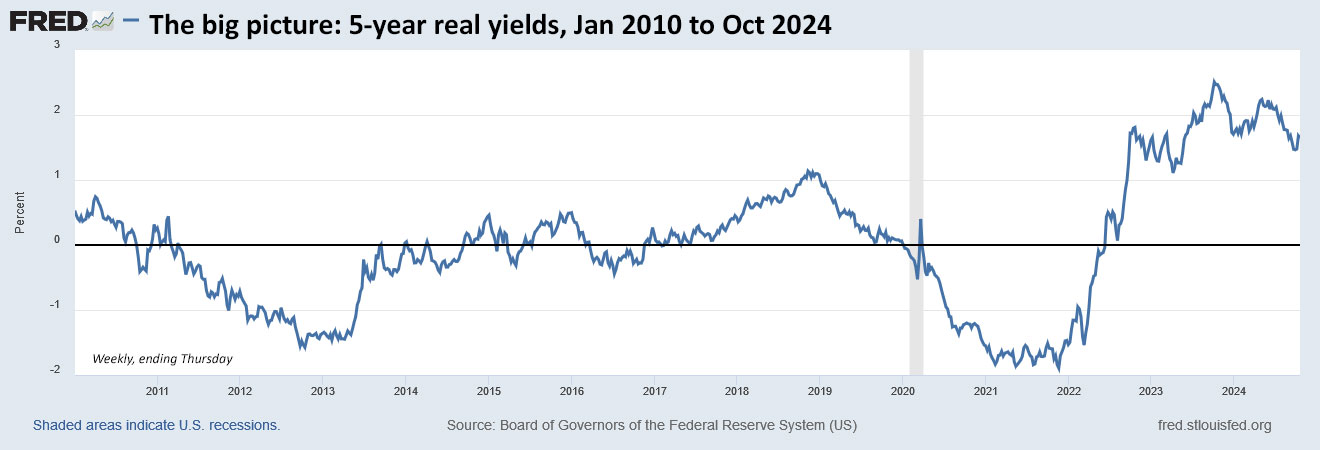

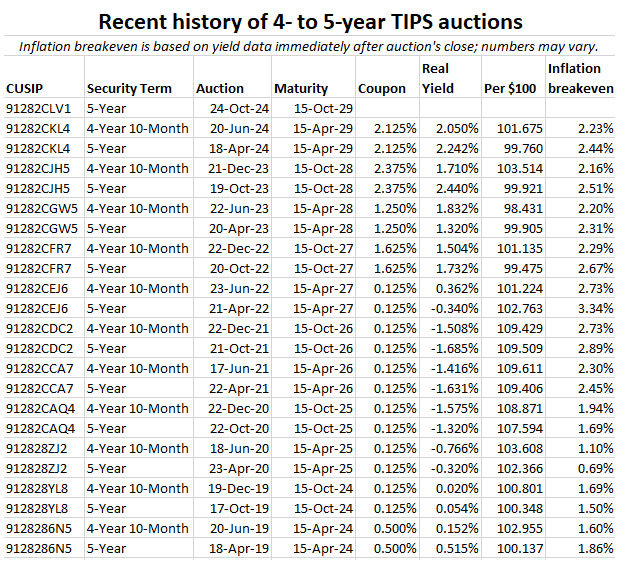

The fixed rate was set at 1.20%, which is in line with the formula the Treasury appears to have been using for a decade: Applying a ratio of 0.65 to the six-month average of the real yields of the 5-year Treasury Inflation-Protected Security. The rate of 1.20% was consistent with my forecast:

The fixed rate is always set to the 1/10th decimal point, so variations in the ratio reflect rounding. But the 5-year TIPS yield has been a good forecast tool.

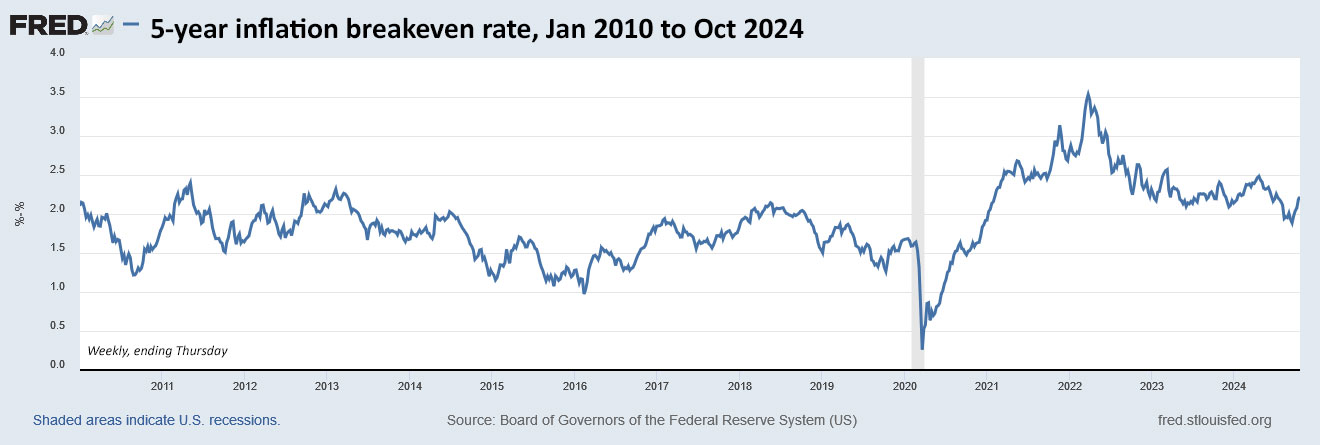

The variable rate was based on six months of inflation data from April to September 2024. The increase was 0.95%, which is doubled to determine the six-month, annualized variable rate of 1.90%.

You can view the history of I Bond variable rates and fixed rates on my Q&A on I Bonds page. Also, you can see historical inflation data on my Inflation and I Bonds page.

The composite rate doesn’t simply combine the two rates, but uses a formula to reflect potential compounding during the six-month term. The end result was 3.11% instead of the 3.10% you’d get from simple addition.

The new six-month, annualized composite rate for purchases through April 2025 will be 3.11%, down from 4.28% for purchases through October. For holders of recent I Bonds with a fixed rate of 1.3%, the composite rate will be 3.21%. If you are holding an I Bond with a fixed rate of 0.0%, the new six-month composite rate will be 1.90%.

While those rates are lower than you can find on a 4-week Treasury bill (currently 4.87%), an I Bond with a fixed rate of 1.2% or 1.3% remains attractive, in my opinion. It will out-perform official U.S. inflation by more than 1.0%, with total safety, tax-deferred interest, and a flexible maturity date.

If your investment timeline is relatively short-term, go with T-bills. I Bonds are better used as a medium- to longer-term cash-equivalent investment.

EE Bonds

Also today, The Treasury set the fixed rate for the Series EE Savings Bond at 2.60%, down 10 basis points from the current 2.70%. The doubling period remains at 20 years, meaning the EE will earn 3.53% annually if held for 20 years. That rate is well below the 4.60% yield of a 20-year Treasury, meaning EE Bonds will be largely ignored unless short-term savings rates fall below 2.60% before April.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I believe you asked 'what is your money earning now?' and I answered... I'm earning a lot more real yield…