By David Enna, Tipswatch.com

We are halfway through the I Bond’s interest-rate-setting period, with the next reset coming on Nov. 1 — or more probably on Halloween Day, Oct. 31. On that day, the U.S. Treasury will announce both a new fixed rate and inflation-adjusted variable rate for the U.S. Series I Savings Bond.

The new fixed rate will apply to I Bonds purchased from November 2024 through April 2025. The fixed rate is crucial because it remains with the I Bond until it is redeemed or matures in 30 years.

The inflation-adjusted variable rate will apply to all I Bonds for six months, no matter when they were purchased. When combined with the fixed rate, it forms the I Bond’s composite rate. As things stand today:

- I Bonds purchased through October 2024 have a fixed rate of 1.3%.

- The current variable rate is 2.96%.

- And that creates an annualized composite rate of 4.28% for six months.

Now the bad news …

It’s early to make a projection, but after looking at the numbers I would guess that both the I Bond’s fixed rate and variable rate will be falling at the November reset. A lot will depend, of course, on where real yields (which are currently falling) and non-seasonally-adjusted inflation (also falling) end up in the next three months.

The fixed rate

The Treasury has no announced formula for setting the I Bond’s fixed rate. TreasuryDirect provides only this cryptic information:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

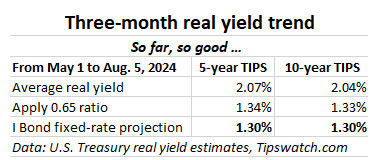

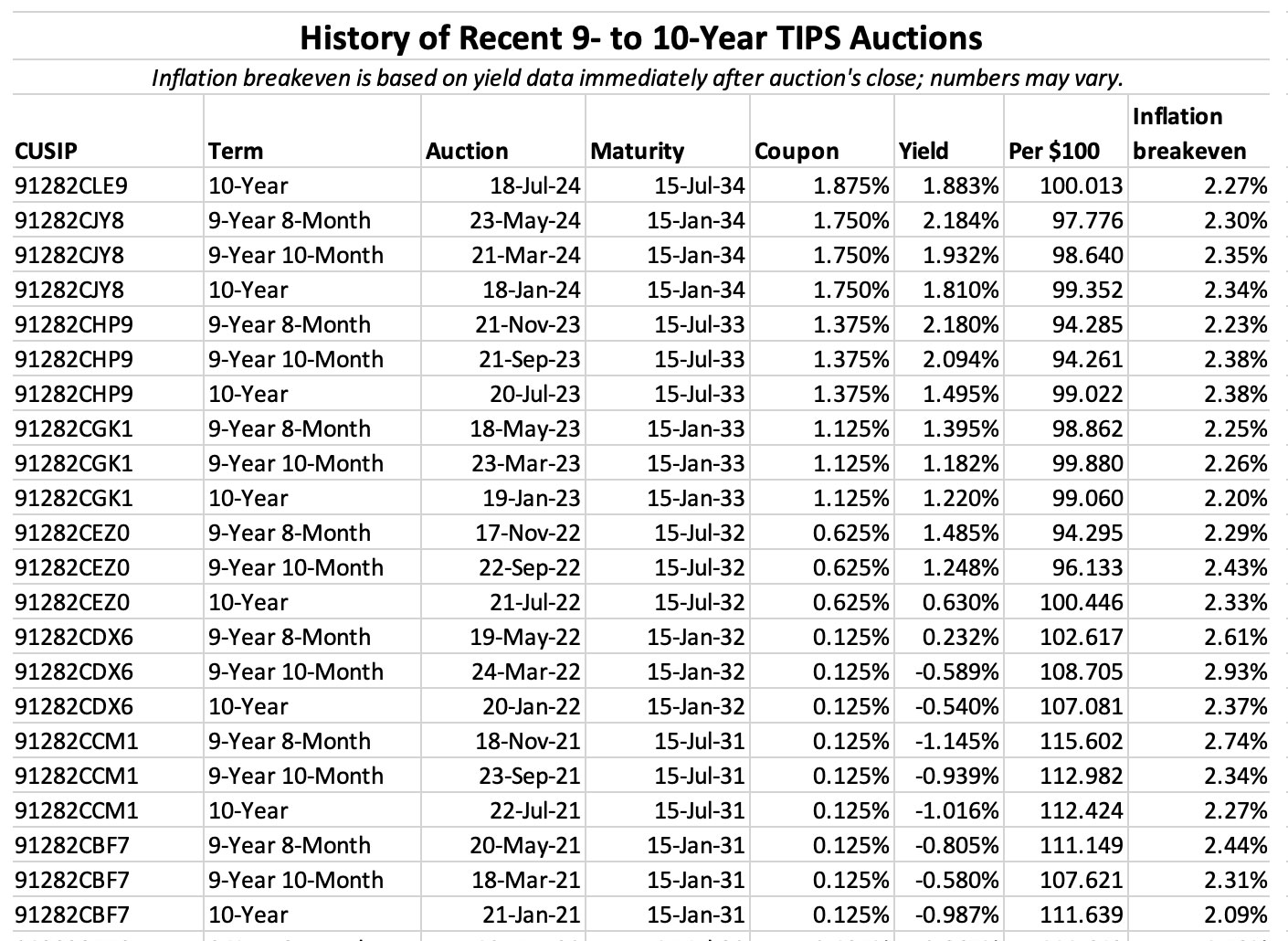

After years of monitoring this fixed-rate decision, (and getting help from clever Bogleheads) I have settled on a formula for forecasting what the Treasury is likely to do. The idea is to look at average real yields of 5- and 10-year TIPS in the six months leading up to the rate decision, and then apply a ratio of 0.65 to those averages.

The formula recently has been accurate when applied to the average for 5-year TIPS, but I like to look at the 10-year TIPS as a backup.

Just before the Treasury’s last I Bond reset on May 1, real yields were at annual highs for 2024, hitting 2.29% for both the 5- and 10-year TIPS on April 30. For the next two months, real yields remained fairly elevated, holding above 2.0% through the beginning of July. But then the decline began, which has accelerated in recent days as the Federal Reserve moves closer to cutting short-term interest rates.

On Tuesday morning, both the 5-year and 10-year TIPS were trading with real yields of about 1.74%, down 55 basis points from the April 30 high.

Interesting thing … if you look at just the three months from May 1 to Aug. 5, the I Bond’s fixed-rate projection holds at the current level of 1.3%.

But … what if real yields continue at this 1.74% level (or lower) for the next three months? If that happens, the I Bond’s fixed rate is likely to fall to 1.2%, or lower.

Conclusion. My feeling is that we are likely to see lower real yields in the next few months, so I am going to assume that the I Bond’s fixed rate will be reset in November to a rate lower than the current 1.3%.

The variable rate

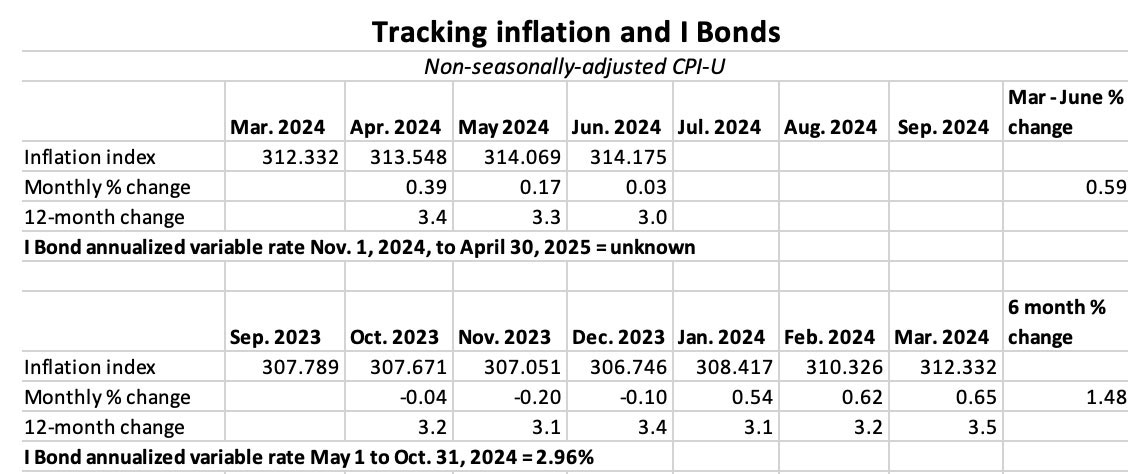

Inflation has been slowing in recent months, falling from an annual rate of 3.4% in April to 3.0% in June. (Inflation over the last six months ending in June was 2.4%, which is high for six months. But in the last three months it was up only 0.59%.) The slowdown can be seen in the three months of data we have so far for calculating the I Bond’s new variable rate:

So far, inflation from April to June would translate to a new variable rate of 1.18%, with three months remaining. Because of recent trends, I would guess inflation will average no higher than 0.20% a month for the last three months, and an even lower number seems likely.

Part of my reasoning is that inflation in August 2023 surged higher by 0.44% and then 0.25% in September 2023. I doubt we will see numbers that high this year, so keeping up with 2023 will be tough. Notice that inflation in June 2024 was up only 0.03%, compared to 0.32% in 2023. We could even see a month of deflation in July to September 2024.

Any way you look at it, the I Bond’s variable rate appears likely to fall from the current 2.96% at the November reset. Of course, inflation is full of surprises, so we can’t be sure.

Conclusion

At this point I’d guess that both the I Bond’s fixed rate and variable rate will be lower, creating a composite rate well below the current 4.28%, possibly somewhere around 3.0% to 3.6%.

What does this mean for I Bond investors?

The good news is that three months of high-ish real yields should hold the I Bond’s new fixed rate above 1.0%, even if real yields decline further. In my view, a fixed rate around 1.0% is attractive.

The bad news is that the potentially lower composite rate is going to scare off I Bond investors. It shouldn’t — because in the long term the high fixed rate is the goal.

By mid-2025 we could also see nominal T-bill rates falling to a range below 4.0%. If the I Bond’s fixed rate can hold at 1.0% or above, I would be a buyer in 2025, even with the lower composite rate. But I would also be likely to turn over some remaining I Bonds with very low fixed rates. Those could end up with a six-month composite rate around 2.0% to 2.4%.

Of course, I could be totally wrong. Nothing is certain. The good thing is that this is a very early, mid-term look at potential I Bond interest rates. So the real answer is to sit back and wait to see how things develop.

What do you think? Post your ideas in the comments section.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I found another work around. I had saved a December 2024 inventory. Opened it and 'return to savings bond calculator'…