By David Enna, Tipswatch.com

The Federal Reserve got the sort of inflation report it desired for July, with the U.S. annual rate dipping below 3.0% for the first time since March 2021. There were no surprises, with annual core inflation dropping to 3.2% from 3.3% in June.

The Bureau of Labor Statistics reported seasonally adjusted inflation for July of 0.2%, which matched economist expectations. Core inflation, which eliminates food and energy, also ran at 0.2% for the month.

The BLS noted that shelter costs — a notorious inflation factor over the last 18 months — increased 0.4% for the month and 5.1% year over year. The BLS added this shocking fact: Shelter accounted for nearly 90% of the monthly increase in the all-items index. Other items from the report:

- Gasoline prices were unchanged in June and down 2.2% over the last year.

- The costs of food at home increased 0.1% for the month were up only 1.1% for the year.

- Costs of motor vehicle insurance continued rising at a ridiculous pace, up 1.2% for the month and 18.6% year-over-year.

- Airline fares fell 1.6% for the month and are down 2.8% for the year.

- Costs of used cars and trucks fell 2.3% for the month and are down 10.9% for the year.

- New vehicle prices also fell 0.2% and are now down 1.0% over the year.

- Apparel costs fell 0.4% for the month.

Overall, most categories in this July report showed a declining trend for inflation, with the exception of shelter, which is considered a lagging indicator. But economists have been noting the lag factor for more than a year. It’s time to recognize that shelter costs are still rising, despite higher interest rates.

Here is the one-year trend for all-items and core inflation, with recent data showing steadily declining U.S. inflation:

What this means for TIPS and I Bonds

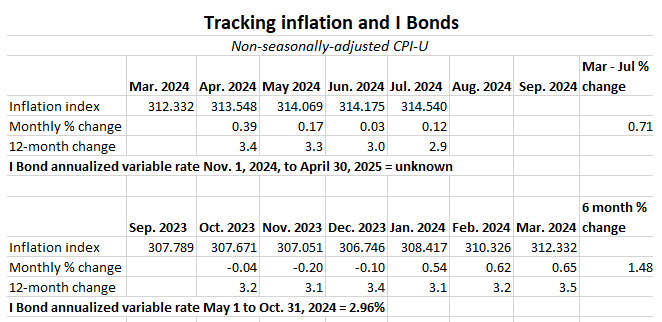

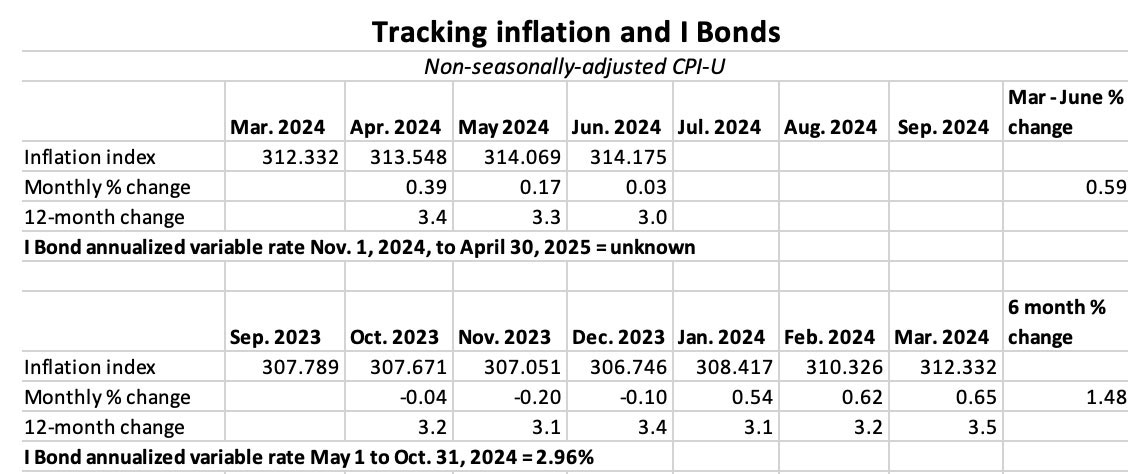

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on TIPS and set future interest rates for I Bonds. For July, the BLS set the inflation index at 314.540, an increase of 0.12% over the June number.

For TIPS. The July inflation number means that TIPS principal balances will increase 0.12% in September, after rising just 0.03% in July. Here are the new September Inflation Indexes for all TIPS.

For I Bonds. The July inflation report was the fourth in a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset November 1. So far, with two months remaining, inflation has run at 0.71%, which would translate to a variable rate of 1.42%. Two months remain, and we could be looking at a new variable rate of around 2.2%, down from the current 2.96%.

See: Where is the I Bond’s composite rate heading in November?

Here are the data so far:

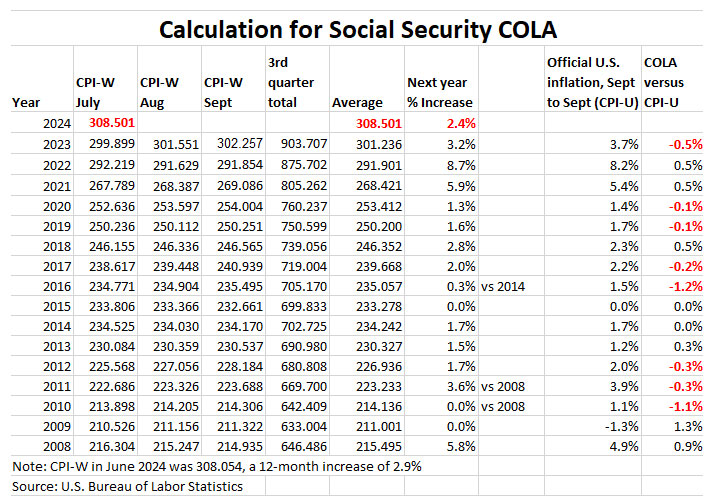

What does this mean for the Social Security COLA?

The Social Security Administration uses a different inflation index — CPI-W — to determine the next year’s cost-of-living-adjustment. And it looks only at the average of three months of data, from July to September, compared with the average for the same three months of the previous year. For July 2024, the BLS set the CPI-W index at 308.501, an increase of 2.9% over the last year.

I have been projecting an increase of 2.7% but the July monthly increase in CPI-W was only 0.1%, versus my projection of 0.2%. Too early to make any judgement.

What this means for future interest rates

The Federal Reserve has been insisting it needs to see “additional data” before it begins a course of interest rate reductions. This July inflation report looks mild enough to kick the Fed into action. From today’s Wall Street Journal coverage:

The report likely seals the case for the Federal Reserve to begin cutting interest rates at its next meeting, Sept. 17-18. … On Wall Street, the debate recently has been not whether the Fed will cut rates soon, but how much it will cut, with some betting that the central bank will reduce rates by half-a-percentage point in September rather than the more typical quarter-of-a-percentage point.

From Bloomberg‘s coverage:

Inflation is still broadly on a downward trend as the economy slowly shifts into a lower gear. Combined with a softening job market, the Fed is widely expected to start lowering interest rates next month, while the size of the cut will likely be determined by more incoming data.

Despite the tricky politics of lowering interest rates just before a U.S. election, I think the Fed is on track for a September rate cut. That’s what the Fed has been signaling and that is what the stock and bond market are already pricing in.

But here is a somewhat contrary view from inflation-watcher Michael Ashton:

(T)here is nothing here that would encourage the Fed to aggressively ease 50bps. Or, for that matter, to ease at all. If the Fed eases in September (which I expect, even though if I were a member of the Board I wouldn’t vote for one), it will be because its members fear recession and not because there is evidence that inflation is licked. That evidence is still elusive.

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing

2.5% to 2.7%+ Real yield above inflation on 20 to 30-year TIP bonds.