Social Security COLA will be 2.5% for payments beginning in January.

By David Enna, Tipswatch.com

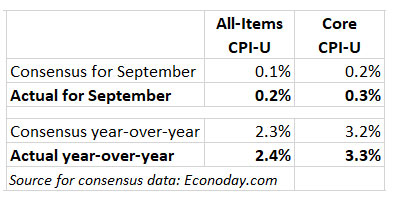

The September inflation report, just released by the U.S. Bureau of Labor Statistics, gives the final pieces of data to determine 1) the new variable rate for U.S. Series I Savings Bonds (it will be 1.90%) and the Social Security cost-of-living adjustment for payments beginning in January (it will be 2.5%).

Plus, the report may give stock and bond markets a bit of a jolt today, with inflation running at a higher-than-expected rate for both the all-items and core measurements. This news, combined with last week’s positive jobs report, could cause the Federal Reserve to scale back its planned cuts in short-term interest rates.

I Bond variable rate

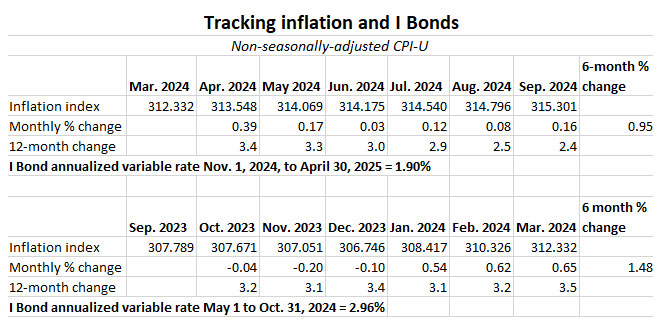

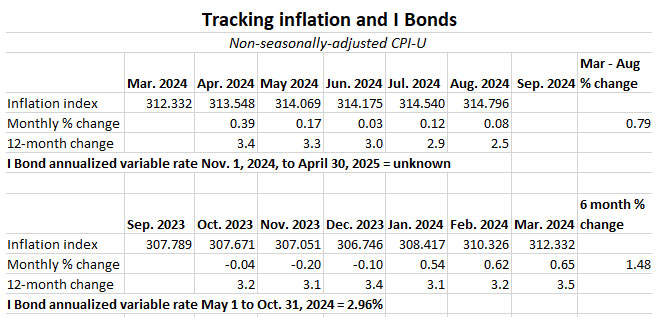

The September report provided the last month of a six-month string of inflation that determines the I Bond’s new variable rate, to be reset for purchases after November 1 and eventually rolling into effect for all I Bonds.

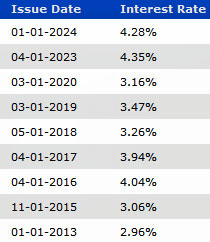

The BLS set September non-seasonally-adjusted CPI-U at 315.301, an increase of 0.16% over the August number. For the six months of April to September 2024, inflation increased 0.95%, which translates to a new variable rate of 1.90%, a sizable decline from the current rate of 2.96%. Here are the data:

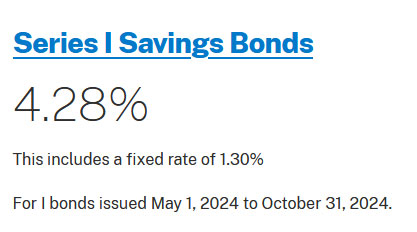

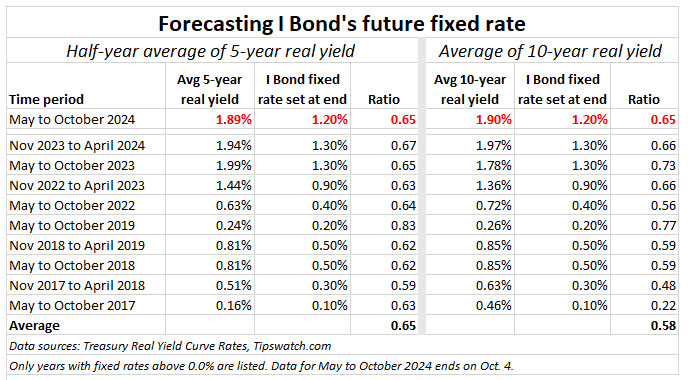

The I Bond’s permanent fixed rate will also be reset on November 1, and seems likely to fall below the current rate of 1.3%. I have projected the rate to be 1.2%, but that is an informed guess. If the fixed rate is 1.2%, the I Bond’s new composite rate will be 3.11%, down from the current 4.28%.

Keep in mind that I Bonds purchased in October will lock in the 1.3% fixed rate and get a full six months of the 4.28% composite rate. If you were planning to invest in I Bonds in 2024, or to add to holdings through gift-box or trust strategies, you should make that move before the end of this month.

Opinion: A new variable rate of 1.90% combined with a fixed rate of 1.2% (if that happens) would mean I Bonds will remain an attractive investment into 2025. That is because a high fixed rate is the most important factor. However, older I Bonds with very low fixed rates (for example, 0.2% or lower) are going to have yields well below market rates, for six months at least.

Treasury Inflation-Protected Securities

Investors in TIPS are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances on these investments. The September inflation report means TIPS principal balances will increase 0.16% in November, after increasing just 0.08% in October. Here are the new November inflation indexes for all TIPS.

Social Security COLA

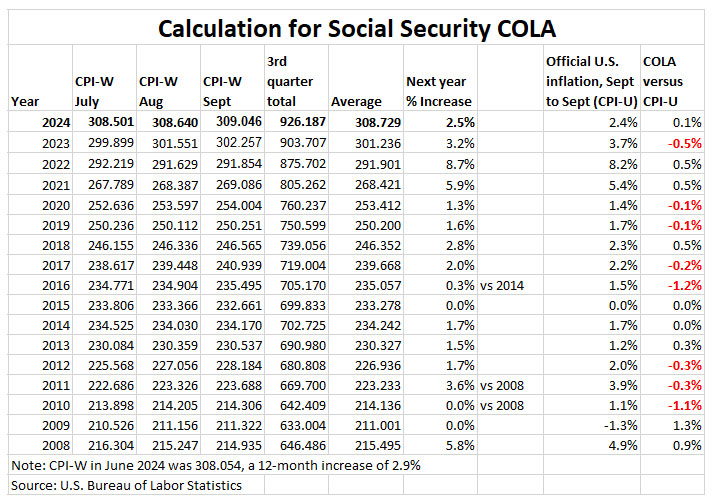

The September inflation report was the third of three — for July to September — that determine the Social Security Administration’s cost-of-living adjustment for payments in 2025. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For September, the BLS set CPI-W at 309.046, which produced a three-month average of 308.729, an increase of 2.5% over the same average for 2023. That means the Social Security COLA will be 2.5% for payments beginning in January. The numbers:

The increase of 2.5% will be the lowest since 2021, but it is slightly higher than the overall increase in U.S. inflation over the last year, 2.4%. The 2.5% increase will boost the average Social Security payment by about $50.

This year, the average monthly benefit payment for retirees is $1,927, according to the Social Security Administration. After the 2.5% increase, that will rise to $1,976 a month.

The inflation report

I’ll be honest: I was not expecting U.S. inflation to come in higher than expectations for September. Gasoline prices fell 4.1% in the month and are down 15.3% for the year. But other factors offset that decline:

- Food at home prices increased 0.4% in September after being pretty tame for most of this year. The BLS said five of the six major grocery store food group indexes increased over the month.

- For example, the index for meats, fish and eggs increased 0.8% in September. And costs for fruits and vegetables were up 0.9%.

- Shelter costs increased 0.2% in September, down from 0.5% from August. But these costs remain 4.9% higher year over year.

- Costs of medical care services increased 0.7% for the month after declining the previous two months.

- Apparel costs were up 1.1% for the month.

- Costs of motor vehicle insurance were up 1.2% for the month and a disturbing 16.3% year over year.

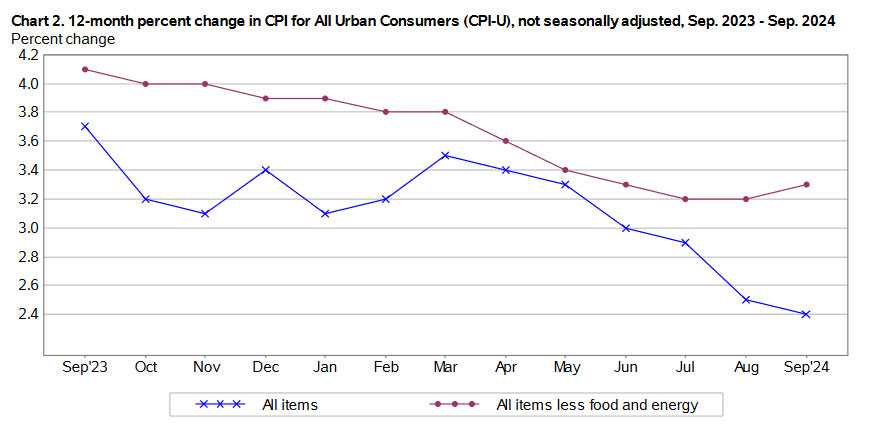

On the positive side, the overall annual inflation rate fell to 2.4%, the lowest level since February 2021. Here is the trend in annual all-items and core inflation over the last 12 months, showing that core inflation remains stubbornly high and in September actually trended higher:

The Federal Reserve

The combination of last week’s positive U.S. jobs report and this higher-than-expected inflation report should be giving the Fed jitters as it moves toward further cuts in short-term interest rates. I am pretty sure we won’t be seeing another 50 basis-point cut in 2024. From this morning’s Bloomberg report:

“Inflation is dying, but not dead,” said Olu Sonola, head of US economic research at Fitch Ratings. “Coming on the heels of the surprisingly strong September employment data, this report encourages the Fed to maintain a cautious stance with the pace of the easing cycle. The likely path is still a quarter point rate cut in November, but a December cut should not be taken for granted.”

I’d agree that a 25-basis-point cut is likely in November, and probably again in December. The Fed has room to move lower with annual inflation currently running at 2.4%. A neutral level for the federal funds rate could be around 3.5%, if inflation remains in this range.

The stock and bond markets seem to be taking today’s inflation news in stride, with the S&P 500 down only about 0.2% in early trading. Real yields have fallen slightly this morning, with the 5-year TIPS trading at 1.67%, down from 1.70% at yesterday’s close.

• Considering an I Bond rollover? Do it the right way.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Follow Tipswatch on X (Twitter) for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UrsaTaurus, I have been contemplating similarly, buying long without the expectation of holding to maturity (I will be dead). I…