By David Enna, Tipswatch.com

U.S. Series I Savings Bonds are a unique investment because all interest is rolled into principal until redemption, and in most cases, all the compounded earnings are tax deferred until the I Bond is redeemed or matures.

This is good.

And no I Bond has ever matured. I Bonds were first issued in September 1998, so history’s first I Bond maturity will come in September 2028. These early-issue I Bonds from years 1998 to 2001 had incredible fixed rates of 3.0%+, meaning they have generated fantastic returns over the years, in the range of 6.0% to 6.25% annual interest, compounded.

This is good.

What isn’t good?

A rather large tax bill is coming for investors in these early-year I Bonds. When the I Bonds are redeemed or mature, the entire amount of interest will be subject to federal income taxes in that year. (I Bond interest is not taxed at the state level.) Some people might say, “Nice problem to have,” but break-through amounts of income can trigger a series of harsh tax consequences: higher marginal brackets, Medicare surcharges, phase-out of some deductions, and the 3.8% Net Investment Income Tax.

The amounts can be seriously hefty: When I Bonds were first created in the fall of 1998, the purchase limit was $30,000 per person per year, and the Treasury even allowed credit cards to be used for purchases with no fees. (Air miles!) This means couples could buy $60,000 in I Bonds each year in those early years.

This chart shows how a $10,000 investment has grown for each of these early I Bond issues, from September 1998 to November 2002. Investors who purchased $20,000 in a year would need to double these amounts; if the purchase was $60,000 for a couple, multiply the amounts by 6.

Couples who bought $60,000 in I Bonds in November 1999 have already earned $193,896 in interest and that amount could easily grow by another 30% at maturity in November 2029, figuring annual interest of around 6%. That brings the total interest to $252,065 in 2029. Ouch.

This is an extreme example, but I have heard from many readers who did indeed buy $60,000 a year of I Bonds in the early years. That has been a great investment, but the coming tax bill causes worries.

My own example: 2031 is a problem

Many readers have been encouraging me to write on this tax issue, but I’ll admit I have been ignoring it. I figured the problem was years away, and my wife and I could handle the influx of taxable interest by adjusting other income sources in the years of maturity. I had no intention of redeeming my high-fixed-rate I Bonds … until maturity.

But then I took a closer look.

I knew we had $40,000 in early-year I Bonds with high fixed rates, but I didn’t realize that all of our purchases were in the single year of 2001, meaning they would all mature in 2031. Hmmm … problem.

Let’s look ahead to 2031. Both my wife and I will be collecting Social Security, a pension, possibly an annuity, and drawing RMDs from traditional IRA accounts. This $144,700 of extra income would very probably push us into a higher tax bracket, high Medicare surcharges and trigger the 3.5% Net Investment Income Tax. Plus, it is possible that tax rates will be higher in 2031.

What’s the plan?

Reluctantly, I am going to give up the idea of holding these high-fixed-rate I Bonds until maturity. Now my plan is to redeem one-fifth of the total each year from 2027 to 2031, bringing the interest income to maybe $28,000 a year, an amount we can deal with by adjusting other sources of income (such as IRA withdrawals).

In our case, these are still paper I Bonds, stored in a bank’s safety deposit box. I looked into the box recently and double-checked. There are 40 $1,000 I Bonds, all issued in 2001. Because the denominations are each $1,000 original value, it will be simple to redeem eight a year for five years, 2027 to 2031.

The denomination is important because paper I Bonds have to be redeemed in whole, unlike electronic I Bonds, which can be redeemed in $25 increments. TreasuryDirect says: “You cannot cash part of a paper savings bond. A paper savings bond must be cashed for its entire value.”

My bank (Wells Fargo in Charlotte) still redeems paper savings bonds, but some banks no longer offer that service. TreasuryDirect says, “Banks vary in how much they will cash at one time – or if they cash savings bonds at all.” From a recent New York Times article:

Hoping to cash in a paper savings bond that’s been lying around for a few decades? Set aside a lot of time for disappointment. …

The process is only getting harder. In May, the nation’s largest bank, JPMorgan Chase, began imposing a $500 limit on each savings bond cashed for longtime depositors — that’s total redemption value, so including any interest owed. Wells Fargo and Citi place a $1,000 limit on new customers. U.S. Bank has a five-year waiting period before it will cash a bond for a new customer.

Converting paper to electronic

Because banks are balking at redeeming savings bonds, especially in large dollar amounts, another option would be to act now to convert these paper I Bonds into electronic form. This isn’t simple, of course. My wife recently converted a batch for her mother, and the process was tedious and time-consuming. But it worked.

To do this, you must have a TreasuryDirect account (if you are reading this I am sure you do), and then you will have to create a Conversion Linked Account where the converted I Bonds will reside. This page on TreasuryDirect has answers to a lot of questions on this procedure.

Harry Sit of TheFinanceBuff.com wrote an excellent guide to conversions, which you can read here. He notes:

In the usual government fashion, they don’t make it easy. Treat it as a test for how well you’re able to follow instructions.

Once converted, you can go into TreasuryDirect and adjust the ownership registration, if needed.

You can find another guide to the conversion process in this May 2022 article on the my site: “Ready to convert paper I Bonds into electronic form? Here’s a step-by-step guide.”

It is not a fun process and that is why I am hoping my wife will do it for us: She has experience!

Do TIPS face this same tax problem?

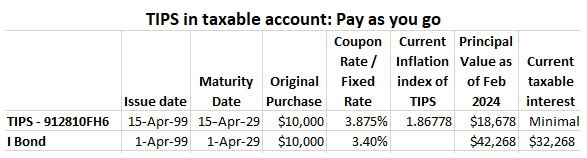

Absolutely not. For example, in April 1999 I bought $10,000 par of a 30-year Treasury Inflation-Protected Security in a taxable account at TreasuryDirect. Let’s look at how it now compares with an I Bond purchased in the same month:

This one chart dramatically shows the difference between investing in a TIPS, which pays out the coupon rate biannually, versus the I Bond, which continuously rolls interest payments into principal all they way to maturity. So even though the TIPS has a higher fixed rate of 3.875%, its current value reflects only inflation of 86.7% over the last 25 years. All the earlier coupon payments — the real yield over inflation — have already been paid out.

Plus, because of the way TIPS are taxed, with inflation accruals getting taxed in the current year, when this TIPS matures on April 15, 2029, there will be only a small amount of tax due — on 3 1/2 months of inflation accruals and the final coupon payment of 1.9375%.

A TIPS held in a taxable account does not create a “tax time bomb.” You pay the taxes as you go. At maturity, taxes are pretty much a non-event.

One more point: The chart demonstrates the benefits of compounded, tax-deferred interest when an I Bond has a very high fixed rate. That April 1999 I Bond is still earning 3.4% above inflation on compounded principal of $42,268. There is no way a TIPS investor could have earned that yield by reinvesting coupon payments in an equally safe investment from 1999 to 2024. For most of that period, real yields have been below 2.25%.

Final thoughts

If you were one of the fortunate investors to have invested in I Bonds in the early era of 1998 to 2001, congratulations. Now you should take a careful look at your investments and the potential tax consequences of holding to maturity. You will be paying taxes, of course, but you may be able to manage the redemptions to minimize effects on your tax bracket, potential Medicare surcharges and the looming Net Investment Income Tax.

You have time to create a plan because the first-ever I Bond maturity won’t occur until September 2028.

• I Bond buying guide for 2024: Be patient

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I found another work around. I had saved a December 2024 inventory. Opened it and 'return to savings bond calculator'…