By David Enna, Tipswatch.com

Updated analysis … I Bond dilemma: Buy in April, in May, or not at all?

If you are a longer-term investor looking for ultimate safety and protection from inflation, you are going to want to buy U.S. Series I Savings Bonds in 2024, up to the $10,000 per person limit and possibly more.

That’s what I think. Not everyone agrees, such as this recent “Buy Side” article from the Wall Street Journal, which put forth the opposite opinion:

If you buy I bonds today, you could find yourself shackled to an investment with diminishing returns, says Aaron Brachman, a financial advisor in Washington: “I’ve never thought I bonds were a good place to park cash,” he says. … While I bonds will still keep you a step ahead of inflation, it’s obvious why their buzz has faded.

It’s no surprise to me that a financial adviser would criticize I Bonds. (No commissions, no fees, and they aren’t sexy.) But to understand why I Bonds remain attractive, even though the composite rate may slip lower, you have to understand how these investments work.

The basics

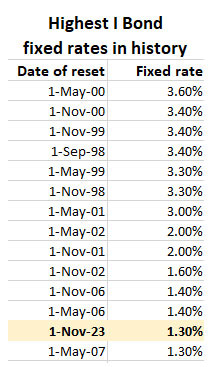

- The fixed rate of an I Bond will never change. Purchases through April 30, 2024, will have a fixed rate of 1.3%, which means the return will exceed official U.S. inflation by 1.3% until the I Bond is redeemed or matures in 30 years. That fixed rate is the highest in 16 years.

- The inflation-adjusted rate (often called the I Bond’s variable rate) changes each six months to reflect the running rate of inflation. That rate is currently set at 3.94%, annualized, for six months. It will adjust again on May 1, 2024, rolling into effect for all I Bonds, no matter when they were purchased.

- The current composite rate is 5.27% annualized for six months for purchases through April 2024.

For a longer-term investor (holding 5 years or more) the fixed rate should be the focus, because it is permanent. Getting a fixed rate of 1.3% above inflation is highly attractive, historically, especially when you factor in the benefits of I Bonds.

I Bonds are an extremely safe and conservative investment. Interest accrues monthly and principal can never decline, even in times of deflation. Investments are limited to $10,000 per person per calendar year for electronic I Bonds held at TreasuryDirect. There is also the option to get $5,000 a year in paper I Bonds in lieu of a federal tax refund. There is also a “gift box” strategy some investors use to stack purchases for future years.

I Bonds are a unique investment with many positives. For example, earnings are free of state income taxes and federal taxes can be deferred until the I Bond is redeemed or matures. Also, I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

But I can earn more elsewhere!

Yes, you can, and that is why short-term investors with a time horizon of 18 months or less should look elsewhere. Redeeming an I Bond held less than 5 years will trigger a penalty of the last three months of interest. That’s an obstacle for short-term investors, with the 13-week T-bill currently yielding 5.47% versus the I Bond’s 5.27%. Even the 1 year T-bill at 4.84% is attractive because it matures after one year with no penalty.

Also, the current 5.27% composite rate is likely to fall lower at the May 1 reset because inflation has been trending lower. The new composite rate could be closer to 3.0% to 4.0%, or even lower. Is that a disaster? Not really, but it’s not great for a short-term investor.

The long-term investor, however, should focus on earning 1.3% above inflation until redemption or maturity in 30 years. That is very attractive for an investment with ultimate safety and ease of ownership. Do you think in the next decade we could again see a period with safe interest rates close to zero? If that happens, I Bonds paying 1.3% above inflation will be performing well.

The buying strategy: Wait.

At this point of market trends, I think we will see both the I Bond’s fixed rate and variable rate fall at the May 1 reset. Mark this date on your calendar: April 10, 2024. At 8:30 a.m. ET on that day, the BLS will issue its March inflation report, setting in stone the I Bond’s new variable rate.

Variable rate. So far, the trend is not looking good for even a moderate variable rate, but things can change in the next few months, as shown in this comparison of non-seasonally adjusted inflation for this rate-setting period in 2022-2023:

I don’t think it’s likely we will see inflation ramp up this year the way it did in early 2023, but after a low number in December, non-seasonally adjusted inflation should perk higher from January to March. However, the end result of six-month inflation could be as low as 1.0%, creating a composite rate of 3.3%. That’s just a guess.

My contention is that for a long-term investor, the variable rate isn’t a crucial factor. It creates a six-month composite rate for a 30-year investment. The fixed rate of 1.3% is crucial. It is permanent.

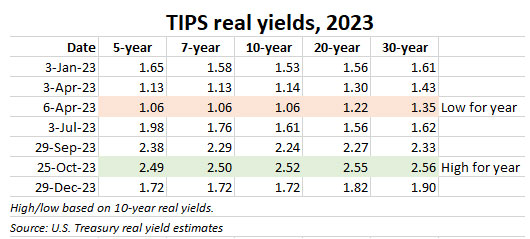

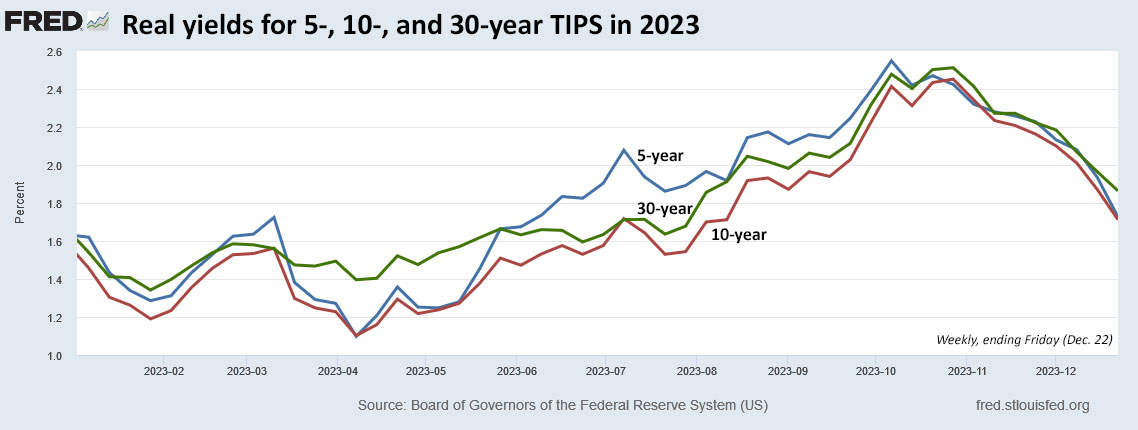

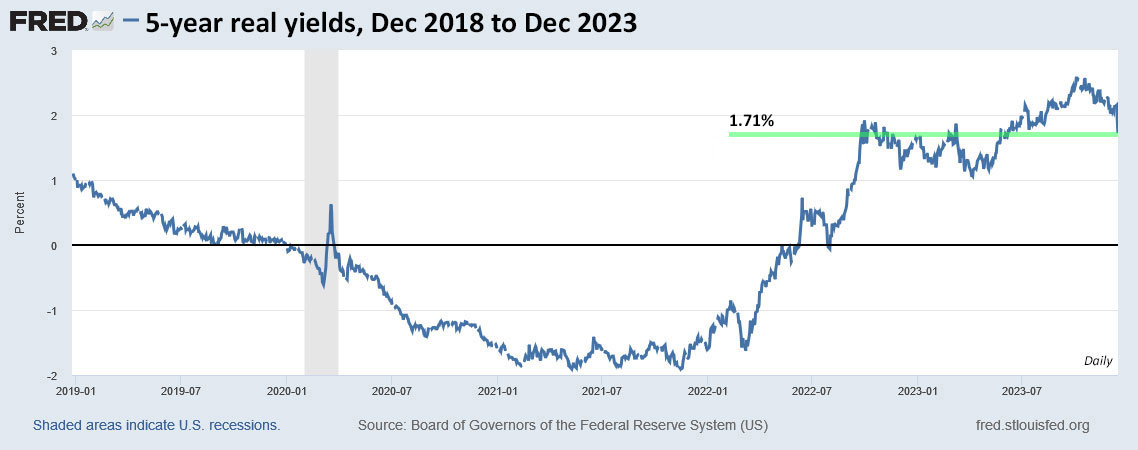

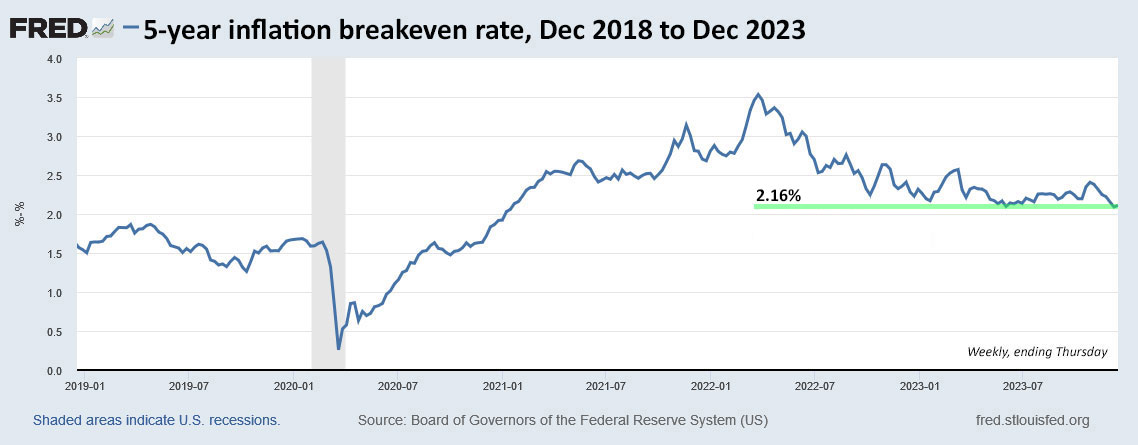

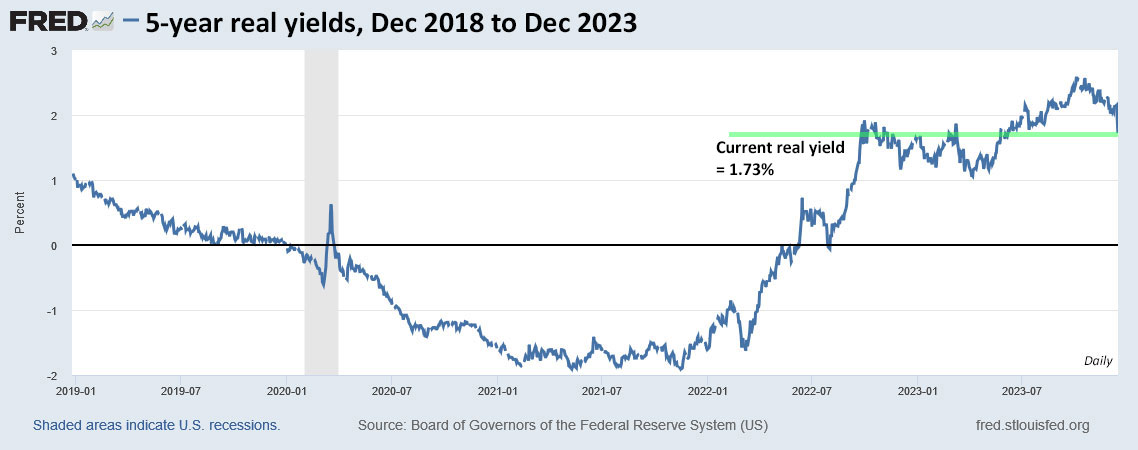

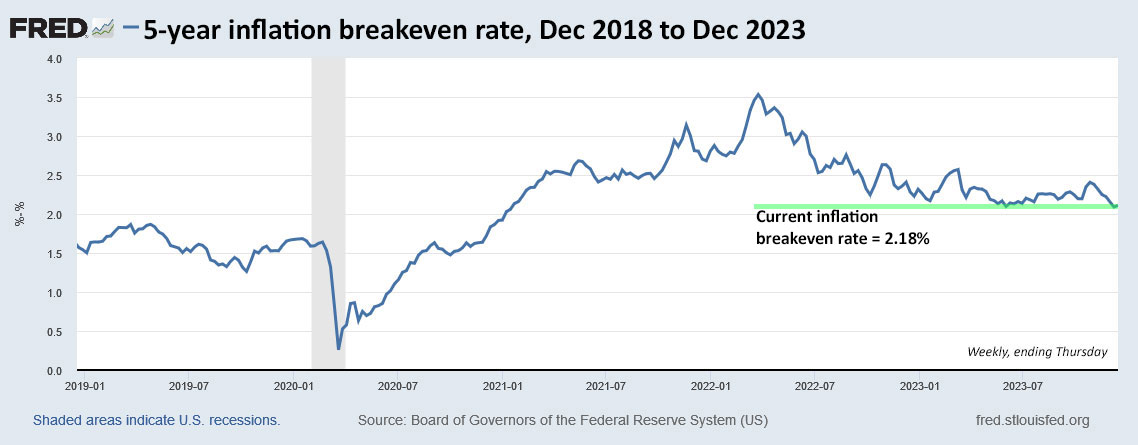

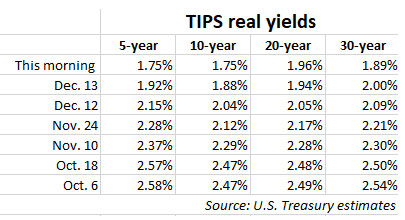

Fixed rate. The Treasury tracks trends in real yields (specifically yields on Treasury Inflation-Protected Securities) to help determine each reset of the I Bond’s fixed rate. Real yields are down dramatically from the November 1 reset, with the 10-year real yield falling from 2.46% on Oct. 31 to 1.83% at Friday’s close, a drop of 63 basis points.

So, at this point, it doesn’t look likely that the I Bond’s fixed rate will rise on May 1. If 10-year real yields managed to hold around 1.8% through April, the fixed rate would probably fall to about 1.2%, still attractive. But the Treasury market is highly volatile right now. Nothing is certain as the market awaits actions by the Federal Reserve. It’s possible real yields could fall another 50 basis points by the end of April. Or rise? Who knows.

What this all means

I think it is highly likely that the best decision will be to buy your full allocation of I Bonds before the end of April, to lock in both the 1.3% fixed rate and 5.27% composite rate for a full six months. But there is no reason to rush that decision. An I Bond purchased in April gets exactly the same return as one purchased in January.

So there is time. Here’s what we will want to watch:

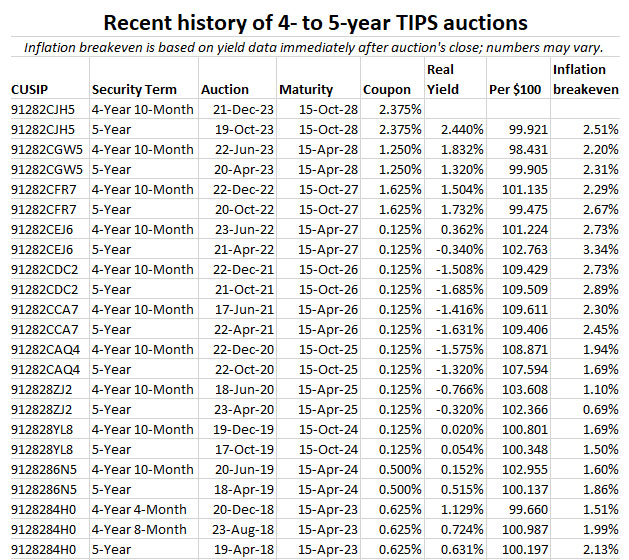

- Are real yields declining? In April, if you see 5- and 10-year TIPS yields falling to 1.5% or lower, you would definitely want to lock in the 1.3% fixed rate by buying in April. In fact, might want to use the gift box strategy to buy more, if you have a trusted partner for that transaction. My opinion: The gift box should only be used to lock in a high fixed rate, like the 1.3% currently in effect.

- Are real yields rising? Despite the Fed’s intention to begin cutting short-term interest rates this year, I’ve seen speculation from market “experts” that longer-term nominal rates could still rise, possibly to 6% on the 10-year Treasury note. Other experts, like bond king Jeffery Gundlach, see 3% as more likely. If 5- and 10-year real yields actually do rise by May to levels above 2.0%, it’s possible that we will see a higher fixed rate at the May 1 reset. I think that is unlikely, but by postponing your I Bond purchase to April you can get a better idea of what’s ahead.

- Is inflation declining? Lower inflation will cut the I Bond’s variable and composite rates, but that should not be a huge factor in this long-term investment decision.

The rollover strategy

If you are holding I Bonds with 0.0% fixed rates, you are currently earning a composite rate of 3.94%. You could redeem some of those now, park the cash in a money market account paying close to 5%, and then in April use that cash to buy I Bonds with a 1.3% fixed rate.

I generally encourage people to continue holding I Bonds “until you need the cash.” It’s great to have these savings bonds growing tax-deferred with zero risk. But this strategy of rolling over 0.0% I Bonds for a 1.3% fixed rate makes sense.

You will owe federal income taxes on the interest earned, and if your withdrawal is more than $10,000 (because of earned interest) you’ll only be able to buy $10,000 in new I Bonds in April. And if you held the I Bond less than 5 years, you will get hit with the three-month interest penalty, either at 3.38% or 3.94% or a combination, depending on your month of purchase.

The rollover strategy especially makes sense for people who are retired and have no way to raise cash for an I Bond purchase without selling an asset or withdrawing IRA money, both creating tax hits.

Reminder: When you redeem an I Bond, you earn zero interest for the month of that transaction. So the best idea is to redeem early in the month, like Jan. 2 or Feb. 2.

The TIPS alternative

For a savvy investor able to handle the complexity of investments in Treasury Inflation-Protected Securities, TIPS at this point are a “superior” investment to I Bonds because real yields are about 50 basis points higher. Plus, there is no purchase cap on TIPS or penalty for selling out early.

But TIPS are subject to market forces, rising and falling in value by the hour. In my opinion, they work best when held to maturity in a structured ladder providing inflation-protected cash for future needs. I Bonds have a flexible maturity so they can be considered more of a “cash equivalent” savings account and work well side-by-side with TIPS. And I Bonds aren’t subject to any market-price swings.

For some investors, TIPS are the preferred choice. For others, it is I Bonds. Or for people like me, a combination.

Conclusion

A lot of shorter-term, yield-hungry investors won’t see the appeal of I Bonds in 2024. That’s fine; there are great short-term options available right now. But longer-term investors interested in building a sizable reserve of inflation-protected cash will want to buy I Bonds in 2024, up to the limit.

But there is no hurry. Just mark your calendars for that April 10 inflation report.

What are your thoughts? Post your ideas and strategies in the comments section below. If you will bypass I Bonds this year, what alternatives are you considering?

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

https://www.wsj.com/finance/investing/the-investment-that-can-shield-you-in-uncertain-times-36c1d850 Mr. Enna in the WSJ today :-)