By David Enna, Tipswatch.com

Also: See my update on why this real yield was actually logical (to bond traders).

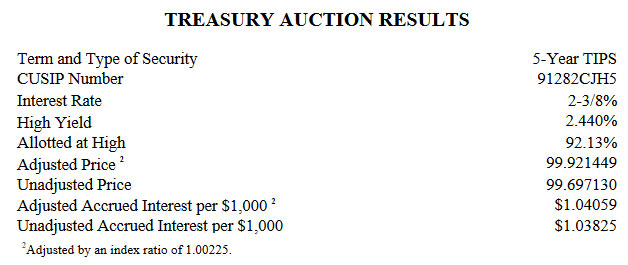

Today’s Treasury auction of $22 billion in a new 5-year Treasury Inflation-Protected Security generated a real yield to maturity of 2.440%, continuing a recent trend of mildly disappointing results for TIPS at auction.

This is CUSIP 91282CJH5, which will mature Oct. 15, 2028. At yesterday’s market close, the U.S. Treasury estimated the real yield of a full-term 5-year TIPS at 2.57%, and a TIPS with a similar term was trading all morning with a real yield in the range of 2.54% to 2.61%. So the result of 2.440% was a downside surprise, indicating fairly strong demand for this new issue.

I was expecting a real yield and coupon rate topping 2.5%. Nevertheless, this TIPS broke through some historic milestones:

- The real yield of 2.440% was the highest for any TIPS auction of this term going back to October 2008, during the heart of the U.S. financial crisis.

- The coupon rate was set at 2.375%, the highest for any 5-year TIPS since the very first TIPS auction of this term in history, which generated a coupon rate of 3.625% on July 9, 1997.

- The auction size was $22 billion, the largest for this term in history.

While the real yield came in a bit lower than expected, CUSIP 91282CJH5 measures up as a stellar investment, with a real yield 112 basis points higher than a similar auction just six months ago, on April 20.

Investment cost

Because this was an auction of a new TIPS, the coupon rate (2.375%) was set below the auctioned real yield (2.440%) and investors got CUSIP 91282CJH5 at a slight discount. The unadjusted price was 99.697130. Here is how that works out for a $10,000 investment:

- Par value: $10,000

- Inflation index on settlement date: 1.00225

- Adjusted principal: $10,022.50

- Unadjusted price: 0.99697130

- Investment cost (adjusted principal x unadjusted price): $9,992.15

- Plus, accrued interest: $10.41 (will be returned at first coupon payment)

- Total cost: $10,002.56

Inflation breakeven rate

At the auction’s close, a 5-year Treasury note was trading with a nominal yield of 4.95%, creating an inflation breakeven rate of 2.51% for this TIPS. That is about 30 basis points higher than the breakeven for recent auctions of this term. Hard to explain, but the 5-year nominal yield actually rose today a few basis points, while this TIPS auction came in 10+ basis points lower than expected.

And the bid-to-cover ratio was 2.36, indicating just average demand. But the pre-auction “when issued” measurement of expected yield was 2.42%, below the actual result. So, the when-issued number most likely indicates strong advance orders for this TIPS from big-money investors, orders that are too big for the secondary market. And therefore those buyers were willing to accept a lower real yield.

Anyone have other theories?

Final thoughts

Today’s auction adds another notch to the view that buying TIPS on the secondary market is a wise move, since you know exactly the real yield and price you will be getting. We’ve had a slew of “slightly” disappointing TIPS auctions this year.

I wasn’t a buyer because my TIPS ladder is loaded with maturities in 2028. But honestly, this real yield of 2.440% was highly desirable, even if a little disappointing. Since it is a new issue, there was no direct comparison on the secondary market.

CUSIP 91282CJH5 will be reopened at auction on Dec. 21, 2023. It will be interesting to watch yield trends over the next two months.

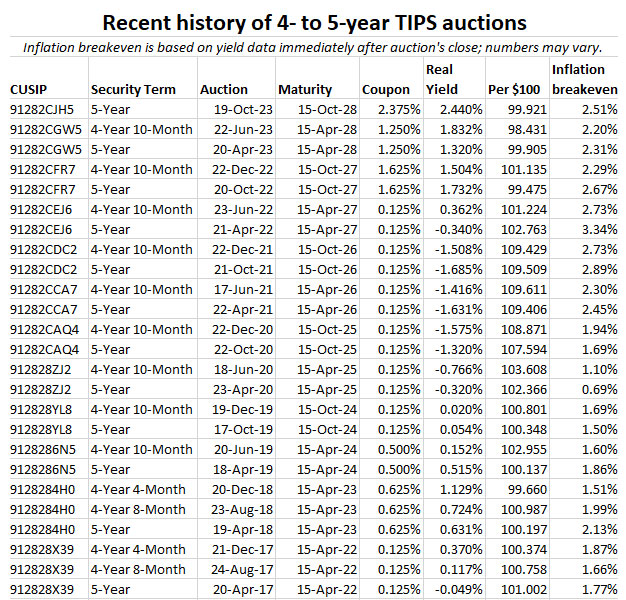

Here is the history of 4- to 5-year TIPS auctions going back to 2017. Note there is nothing on the list that even comes close to a real yield of 2.440%.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dongchen, I always say that the inflation breakeven rate reflects sentiment but is a fairly lousy predictor of future inflation.…