Composite rate for I Bonds rises to 5.27%. Fixed rate for EE Bonds rises to 2.70%; doubling factor holds at 20 years.

By David Enna, Tipswatch.com

The Treasury announced today it is raising the permanent fixed rate on the U.S. Series I Savings Bond to 1.3%, the highest fixed rate since a reset in May 2007.

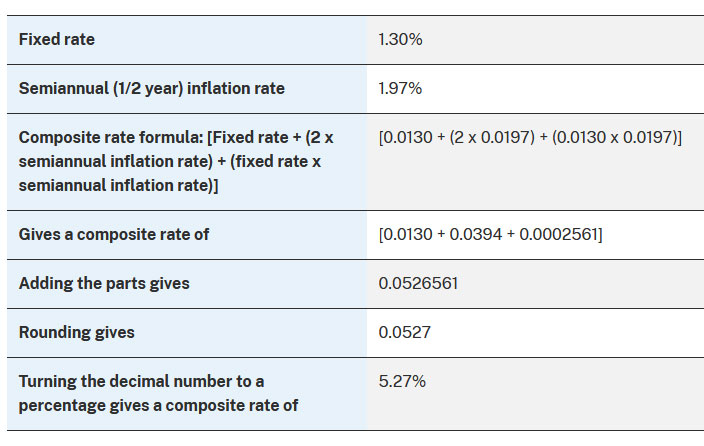

Combined with a six-month inflation-adjusted variable rate of 3.94%, I Bonds sold from November 2023 to April 2024 will get a composite rate of 5.27%, Treasury said.

The I Bond’s fixed rate is important for investors. It is permanent and stays with an I Bond until redemption or maturity in 30 years. This new fixed rate only applies to I Bonds purchased from November 2023 to April 2024.

The variable rate applies to all I Bonds, no matter when they were issued. It changes every six months and the starting date of the change depends on the month you bought the I Bond. This new 3.94% variable rate is based on non-seasonally adjusted inflation from April to September 2023.

Here is how the Treasury calculated the new composite rate:

Note that the new composite rate of 5.27% applies only to I Bonds purchased from November 2023 to April 2024. If you are holding an older I Bond with a fixed rate of 0.0%, your new composite rate will be 3.94% for six months. If you bought an I Bond from May to October 2023, it has a fixed rate of 0.9% and the new composite rate will be 4.86% for six months.

Reaction

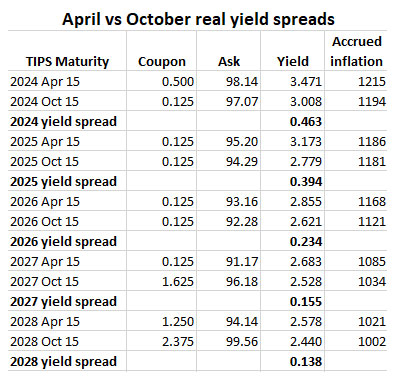

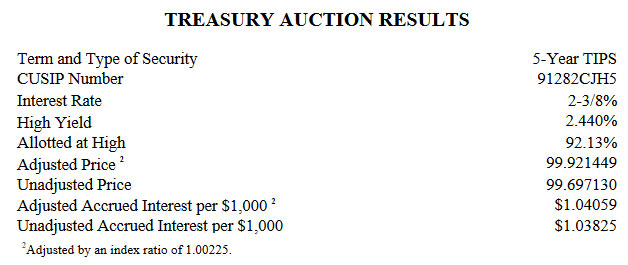

I my most recent projection I estimated that the I Bond’s fixed rate would be set in a range of 1.1% to 1.4%, so a fixed rate of 1.3% fits into expectations. It is not spectacular, especially when a comparable investment — the 5-year Treasury Inflation Protected Security — has a real yield of 2.40%, an advantage of 110 basis points.

Not spectacular, but satisfactory and hits a 16-year high. I Bonds are a simple investment to track, earn tax-deferred interest, and can never lose a cent of accumulated value. An I Bond with a fixed rate of 1.3% remains attractive and a worthy investment.

But how worthy? I already bought my $10,000 I Bond allocation this year, back in April when the composite rate was impressive (6.89%) but the fixed rate was what we know see as mediocre (0.4%). That I Bond will soon transition to a composite rate of 4.35%. Oh well. I will still hold that one.

I am not sure a fixed rate of 1.3% is attractive enough to do a “gift-box swap” in 2023, but I will consider it. More likely I will simply wait until mid-April 2024 to decide if the 1.3% fixed rate remains highly attractive. There is no penalty for waiting to buy this 1.3% I Bond. You can purchase any time from November to April and get the same return.

From an article today on Money.com:

What’s notable about the new I bonds rate is not the overall 5.27% yield but the fixed rate. The fixed rate hasn’t exceeded 1% since before the Great Recession ….

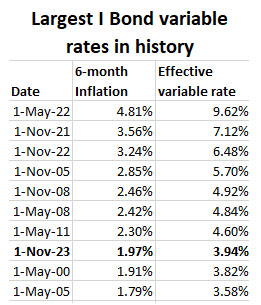

As an example of how critical the fixed rate is, look no further than the folks who bought lots of I bonds when the rate was an eye-popping 9.62% last May. The Treasury Department says it sold billions worth in the first week alone; in the last week the rate was applicable, the website had so many visitors it crashed.

While the inflation-based rate was extremely high, the fixed rate was 0%. Without a fixed rate boosting the yield, those same I bonds purchased in 2022 are now earning only 3.94% (the inflation-portion only) — versus the 5.27% rate for I bonds purchased starting in November.

Then the next question: Is a six-month composite rate of 5.27% attractive enough for short-term investors in I Bonds, looking to redeem in 12 to 18 months? I’d guess most short-term investors (I am not in the category) will pass and look to invest in shorter-term T-bills, with the 1-year currently yielding 5.41% and no penalty for redemption after one year.

Conclusion. For longer-term investors, I’d say this new I Bond with a 1.3% fixed rate is a solid investment, considering the benefits of tax-deferral, deflation protection and exemption from state income taxes. We’ve had a long wait for a super-safe return this attractive.

Rolling over 0.0% fixed rates?

If you are holding I Bonds with 0.0% fixed rate — especially those held for five years or more — you can consider redeeming those older I Bonds for new ones with the 1.3% fixed rate. When you redeem, you will owe federal taxes on the interest earned.

If you are planning to redeem I Bonds held for less than five years, read this first: “The I Bond exit ramp is now open; proceed with caution“.

I think this is a sound strategy, especially if you don’t want to raise another $20,000 to buy I Bonds this year or next in two separate accounts.

EE Bonds

And now for the disappointing news: The Treasury raised the permanent fixed rate of EE Savings Bonds to 2.7%, up only 20 basis points from the past rate of 2.5%. It is retaining the policy that EE Bonds will double in value if held for 20 years, guaranteeing a compounded return of about 3.53%.

I’m baffled. Back in May 2023, when the EE’s fixed rate was set at 2.5%, a 10-year Treasury note was yielding 3.44%. The current yield is 4.88%, 144 basis points higher. Raising the EE’s fixed rate to 2.7% is a weak move, and guaranteeing a return of 3.53% for holding 20 years is also inadequate. You can invest in a 20-year Treasury bond and get a return of 5.21%.

The doubling period should have been shortened to 16 years, at least, which would guarantee a return of about 4.5% if held for 16 years. Even that falls short of attractive. EE Bonds can now be placed on a shelf to collect dust. They aren’t a meaningful investment in November 2023.

What’s your reaction?

Investors are going to be sorting through a lot of issues when considering this new I Bond with a fixed rate of 1.3%. Is it a better investment than a 5- or 10-year TIPS held to maturity? Or is it an acceptable tax-deferred alternative? Is the 1.3% fixed rate attractive enough to trigger gift-box purchases for future distribution? Will you invest in January 2024 or hold off until mid-April when the next variable rate will be set?

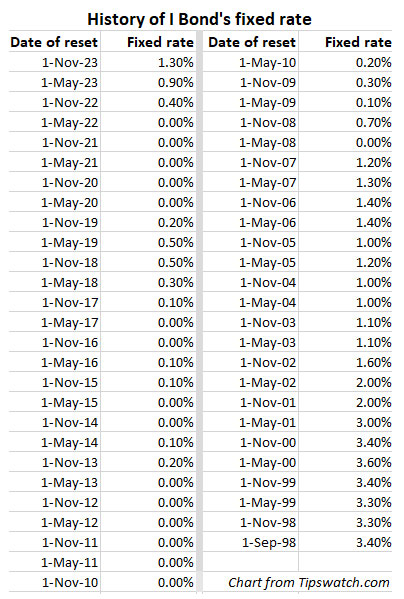

Lots of things to consider. Post your ideas in the comments section below. To close, here is the history of all fixed rates for I Bonds back to their inception in September 1998:

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I don't know anything about TIAA Traditional, but I see it appears to be an annuity. TIAA is a good…