By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will auction $22 billion in a new 5-year Treasury Inflation-Protected Security, and the results should be attractive for investors seeking protection from future inflation. It should generate the highest real yield to maturity for any auction of this term in 15 years.

This is CUSIP 91282CJH5, which will mature Oct. 15, 2028. The $22 billion auction size is the largest ever for this term, up from $21 billion for similar auctions in October 2022 and April 2023. The coupon rate and real yield to maturity will be set by the auction results.

Real yield: What to expect

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

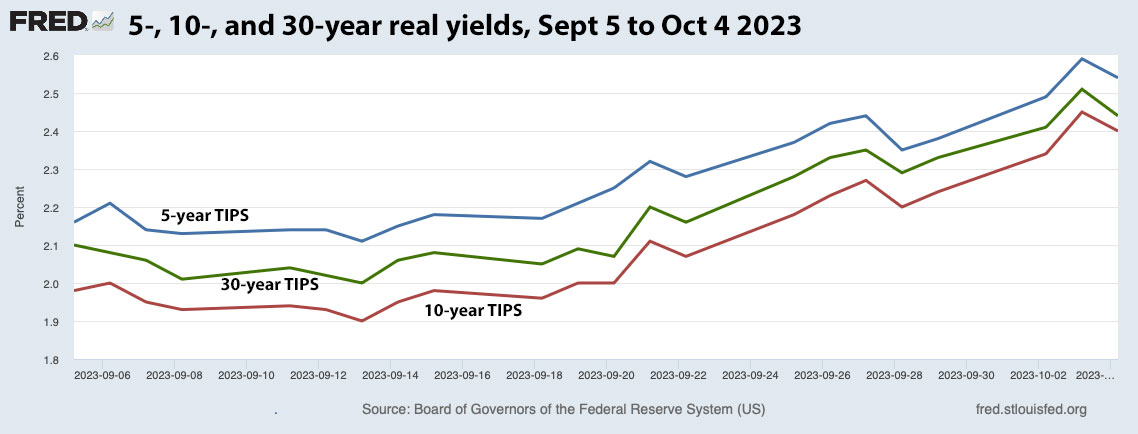

As of Friday’s market close, the Treasury was estimating the real yield of a 5-year TIPS at 2.39%, down 21 basis points from a week earlier. Treasury yields have been sliding lower based on a combination of more dovish comments by Federal Reserve officials, and a flight to safety in the wake of turmoil in the Mideast.

Nevertheless, a real yield of 2.39% is historically high. No 4- or 5-year TIPS has auctioned with a real yield above 2% since October 2008 (then at 3.270% in the depths of financial panic). The most recent auction of a new 5-year TIPS, in April, got a real yield of 1.32%, more than 100 basis points lower.

Another positive factor for this auction is that the coupon rate could end up at 2.375% if the real yield remains higher. That would be the highest coupon rate for any 5-year TIPS at auction since April 2006. That means this TIPS would pay out 2.375% annually on top of inflation-adjusted accruals to the principal balance.

Fun fact: As recently as March 2022, a 5-year Treasury note had a nominal yield of 2.33%, less than the likely yield of this TIPS above inflation. Just shows you the mighty move we have seen in bond yields, and why this new TIPS looks attractive.

Here is the 5-year real yield trend over the last 20 years, reinforcing that the current real yield is historically attractive:

Pricing

Because this is a new TIPS, the Treasury will set the coupon rate slightly below the auctioned real yield and investors will get a slightly discounted price. However, the inflation index on the Oct. 31 settlement date will be 1.00225, so the adjusted price will probably come in right around par.

Some investors like these new issues because they are buying very little accrued inflation, which is not protected against deflation. So this new TIPS should fit that profile. (I consider long-term deflation risk to be a minor factor in TIPS investing.)

Also, because this is a new TIPS, there won’t be a viable secondary market alternative for this October 2028 maturity for a few weeks, at least. But there is a TIPS maturing in April 2028 with a coupon rate of 1.25% and a secondary-market price around 95.18. Its real yield is currently 2.381%.

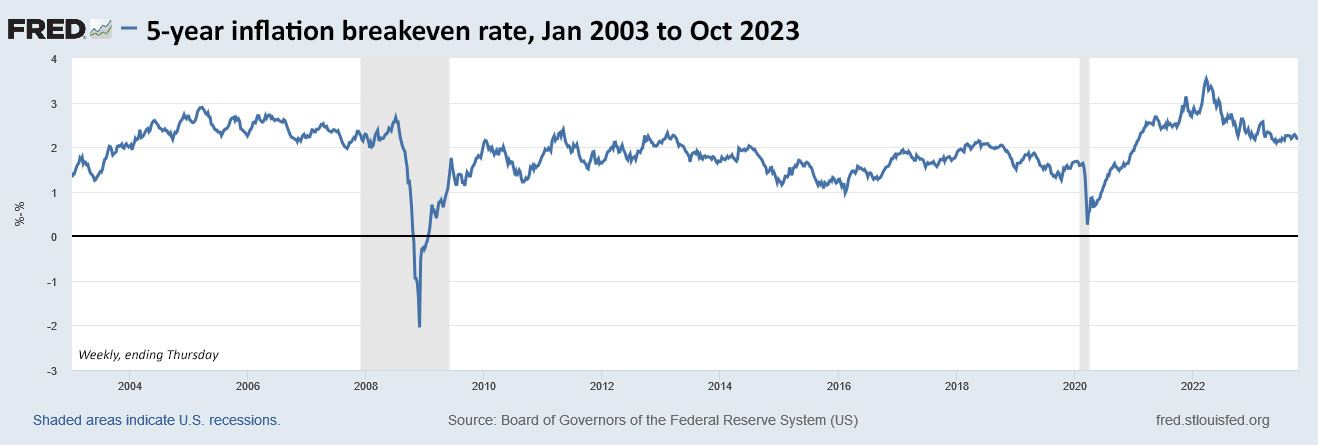

Inflation breakeven rate

With a 5-year nominal Treasury currently yielding 4.65%, this TIPS would have an inflation breakeven rate of 2.26%, a bit lower than recent auction results for this term. This is another factor making this an attractive investment. If you believe annual inflation will average more than 2.26% over five years, buy the TIPS and not the nominal Treasury.

Here is the trend in the 5-year inflation breakeven rate over the last 20 years, showing that the current rate of 2.26% fits into a “normal” range, meaning the TIPS is not expensive versus a nominal Treasury:

Other alternatives?

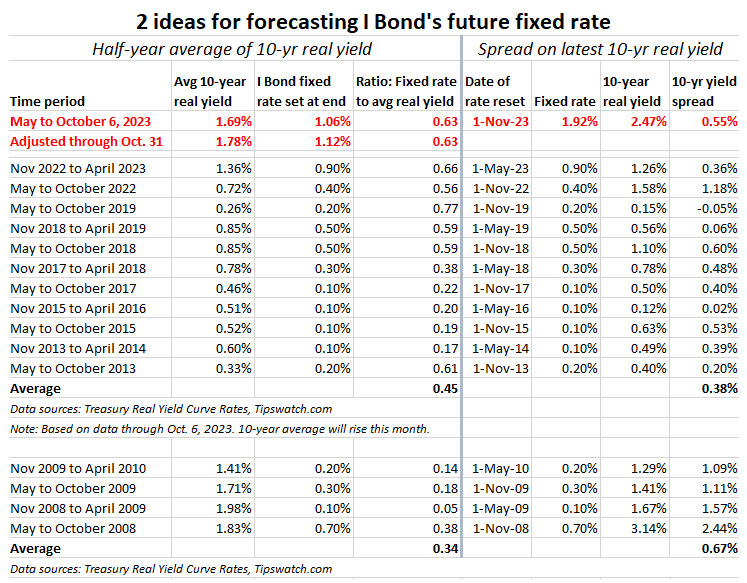

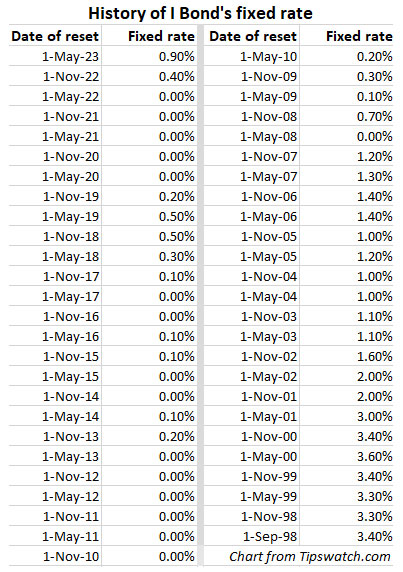

I Bonds. The U.S. Series I Savings Bond is a good comparable for a 5-year TIPS, since the I Bond can be redeemed after 5 years with no penalty. It currently has a fixed rate of 0.9% (which may go higher for I Bonds purchased after November 1). Still, that is a huge yield gap with a 5-year TIPS yielding 2.39%. For an investor who can handle the complexity, a 5-year TIPS is the superior investment.

Would I still buy I Bonds with a fixed rate of 0.9%, or higher? Yes, in combination with TIPS. For me, I Bonds are a super-safe, inflation-adjusted, tax-deferred savings account.

Bank CDs. Best-in-nation 5-year CDs are currently yielding about 4.85%, according to DepositAccounts.com. That’s a bit better than the nominal 5-year Treasury, but interest would be subject to state income taxes. I’d still prefer the TIPS.

Final thoughts

For anyone looking to fill a 2028 spot in a TIPS ladder or other investment plan, this auction looks like a no-brainer. The result should be attractive, although recent TIPS auctions have not produced stellar yield “surprises.” There’s no way to know what yield a non-competitive bid will get until you see the auction results, which will be announced at 1 p.m. ET Thursday.

I won’t be a buyer. Why? My TIPS ladder is loaded with issues maturing in 2028, so I have been looking to fill other needs, even though this TIPS is more attractive than all my current holdings. Oh, well.

If you are pondering an investment at Thursday’s auction, keep an eye on the Treasury’s Real Yield Curve page, which updates at the market’s close each day. This is an estimate, but can give you a good idea of how yields are trending.

The auction closes at 1 pm EDT. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I hope to post the results soon after the close.

Here is the history of recent TIPS auctions of the 4- to 5-year term:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I don't know anything about TIAA Traditional, but I see it appears to be an annuity. TIAA is a good…