An earthquake has hit the Treasury market. The result is that TIPS are becoming much more attractive.

By David Enna, Tipswatch.com

The investment world — from Suze Orman to your Uncle Bob — has been fascinated by U.S. Series I Savings Bonds for the last 12 months, and rightly so. These inflation-tracking savings bonds are ultra-safe and are currently offering a gaudy yield of 9.62% annualized, for six months.

I’m a huge fan of I Bonds, and I highly encourage people to invest in them. But today, rather suddenly, there is a true alternative to I Bonds: Treasury Inflation-Protected Securities. Over the last 2 1/2 years, TIPS have been a mediocre investment, with real yields lagging behind the official U.S. inflation rate. But all that has changed — dramatically — in June 2022.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match current U.S. inflation. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

In the last two weeks — and especially after Friday’s high-side shocker of an inflation report — both nominal and real yields have surged higher, transforming a “meh” TIPS market into something very interesting: Real yields positive to inflation at a time of dangerously high inflation.

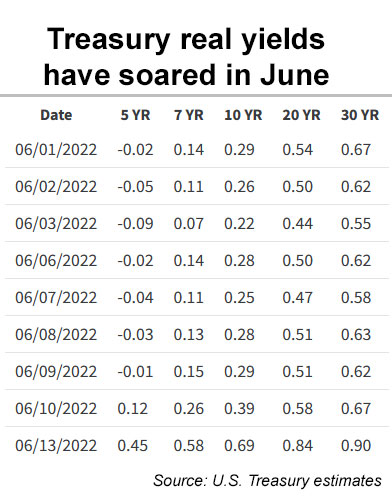

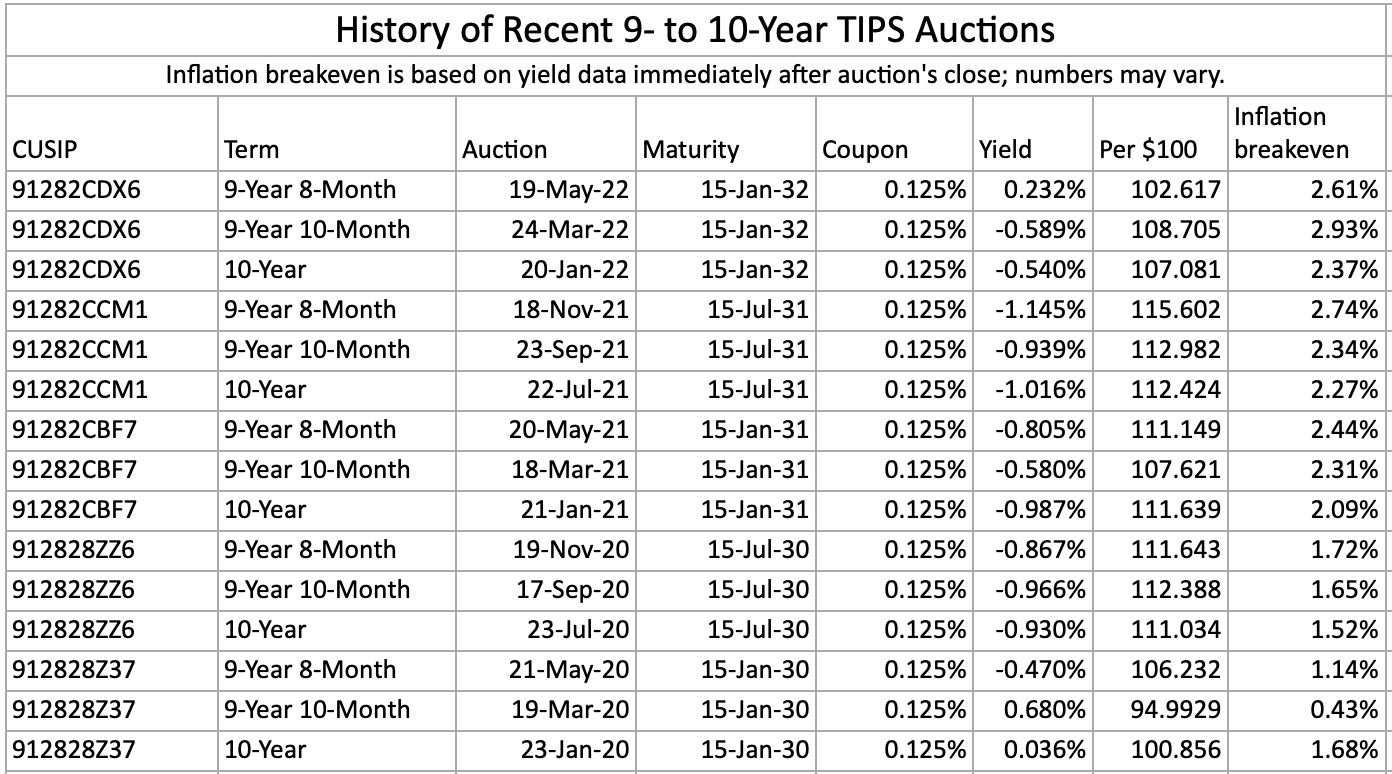

Here are the real yield numbers since June 1, based on the Treasury’s daily yield curve estimates:

These are some crazy numbers. The 5-year real yield surged 46 basis points in two days. The 10-year TIPS real yield was up 40 basis points. For those of you who invest in TIPS mutual funds, that’s pretty much “half a duration,” meaning those funds have been hit with a half a duration event in just a couple days. For example, the broad-based TIP ETF has a duration of 7.12 years. Last Thursday, it closed at $117.51 a share. Now it is trading at $113.72, a loss of 3.2% in a few days.

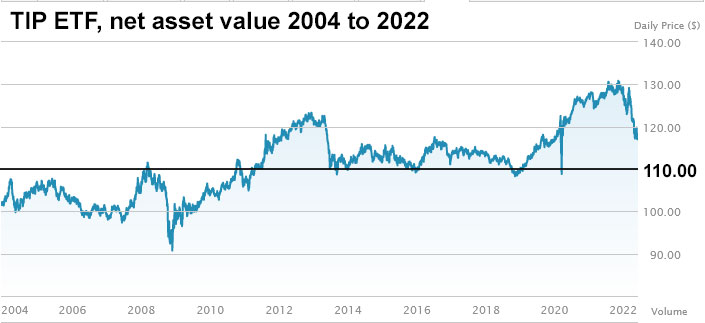

Many times in the 2015 era of Fed tightening (seems like a lifetime ago) I pointed to a price of $110 for the TIP ETF as a “buy signal.” I’ve thought about discussing that target again, but honestly I thought it would be too alarming and even embarrassing to point to a possible price decline of about 12% from where the TIP ETF was trading as recently as March 8, when it closed at $129.16.

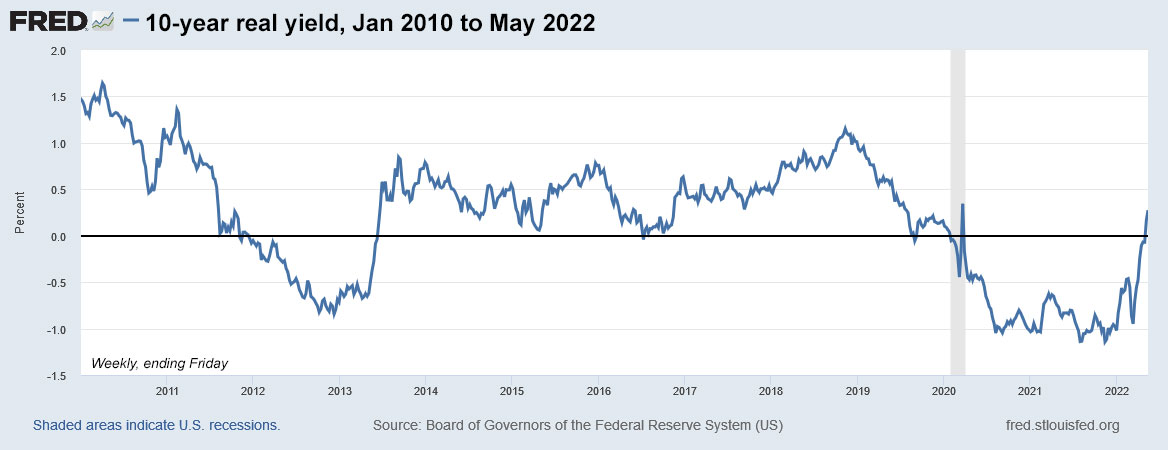

Here is a historical chart, showing how $110 was a resistance level through nearly a decade of trading, right up to the pandemic-triggered market chaos of March 2020:

Although I prefer to buy TIPS at auction and hold them to maturity, I do have investments in Vanguard’s Short-Term TIPS ETF (VTIP) and Schwab’s Total TIPS ETF (SCHP). Because of very high inflation adjustments over the last year, VTIP hasn’t performed horribly. It has a total return of -0.71% year to date. But SCHP’s total turn has been -8.08% year to date because of its much higher duration. That is similar to its return in 2013, the year of the bond market’s “taper tantrum.”

I will continue to hold these funds, but I have been moving some money out of SCHP and into individual TIPS throughout this year.

What this means …

Yes, all of this is bad news for investors in TIPS mutual funds and ETFs, but it is good news for investors seeking to increase their holdings in inflation-protected investments. Real yields are now solidly positive across 5 to 30 years, giving TIPS a strong yield advantage over I Bonds, which if bought today will have a 0.0% real yield going into the future. So as of Monday’s market close:

- The 5-year TIPS has a yield advantage of 45 basis points over an I Bond purchased today.

- The 10-year TIPS, 69 basis points

- The 30-year TIPS., 90 basis points

Historically, I Bonds had have a real yield lower than a typical TIPS, and that is OK because I Bonds have several advantages: 1) a flexible maturity of 1 year to 30 years, 2) tax-deferred interest, and 3) much better protection against deflation.

But purchases of I Bonds are limited in electronic form to $10,000 per person per calendar year, plus $5,000 in paper I Bonds in lieu of a federal tax refund. I love I Bonds as an investment, but after you hit the $10,000 cap where do you go for inflation protection?

There are no limits on TIPS purchases. You can buy them on the secondary market, even in an IRA account if you choose, or participate in monthly auctions. See my Q&A on TIPS.

I want to state clearly that TIPS are for preserving wealth, not building wealth. If you are in the early stages of investing and far from your long-term needs for buying a house or for paying for college or especially for retirement, TIPS aren’t going to be a great investment. That’s especially true when yields are less than 1% over inflation. You probably won’t build enough wealth to meet your goals.

However, if you are nearing retirement, or in retirement, and have an adequate nest egg, then TIPS make sense as part of your investment portfolio – especially if you buy and hold them to maturity. That strategy is risk-free, and you can protect a part of your savings from the dangers of unexpected inflation.

The downside to TIPS

TIPS are a complicated investment. I’ve had long discussions with finance-savvy reporters at the Wall Street Journal and other media who simply “didn’t get” the idea of a return based on future inflation, or a “real yield to maturity,” or a “discount” or “premium” price at TIPS auctions.

Complicated, yes, but investors can simplify TIPS investing by buying them and then holding them to maturity. That strips away almost all the risk of market fluctuations, as we have seen with TIPS mutual funds. You can simply track par value x the current inflation index and ignore market value.

If you buy a 10-year TIPS that yields 0.69% above inflation, you are going to get a return that is close to 0.69% over inflation for a decade. (The actual return could be affected by a long deflationary period, which could reduce accrued principal. This is one advantage I Bonds have over a TIPS.)

Also, the inflation accruals earned by TIPS are federally taxed as income in the year they are earned, even though they aren’t paid out until maturity or redemption. This creates a “phantom tax” issue, and is the reason most financial advisers recommend buying TIPS in a tax-deferred account. (You can purchase TIPS at auction through most major brokerages with no commissions or fees.)

Where are real yields heading?

Of course, I can’t predict the future. But I have examined several Fed easing and tightening cycles of the past and it seems clear to me that we haven’t reached the top for real yields, especially for shorter-term issues, which will be more sensitive to Fed rate increases. A 10-year real yield rising above 1% seems like a certainty, unless the Fed loses its nerve. (And at that point, we should also see the I Bond’s fixed rate rise above 0.0% in the November 2022 or May 2023 rate resets.)

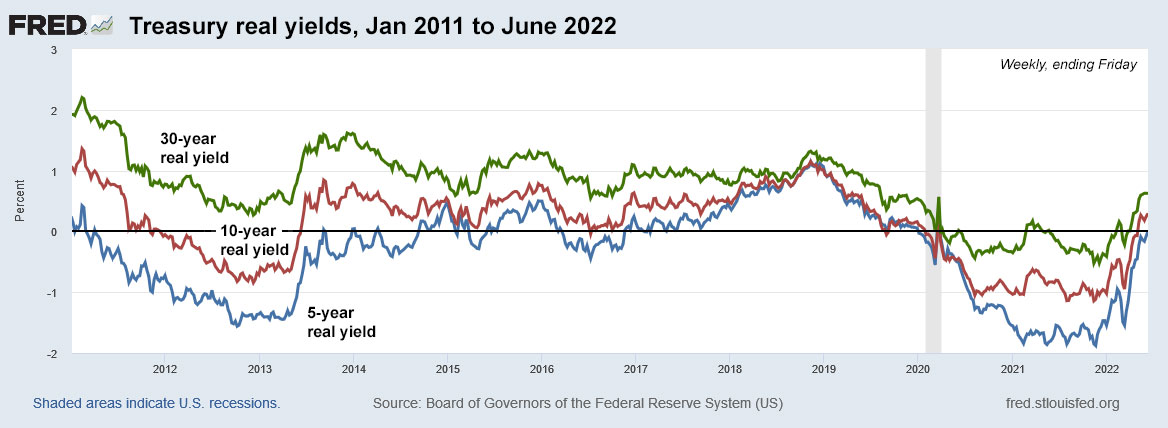

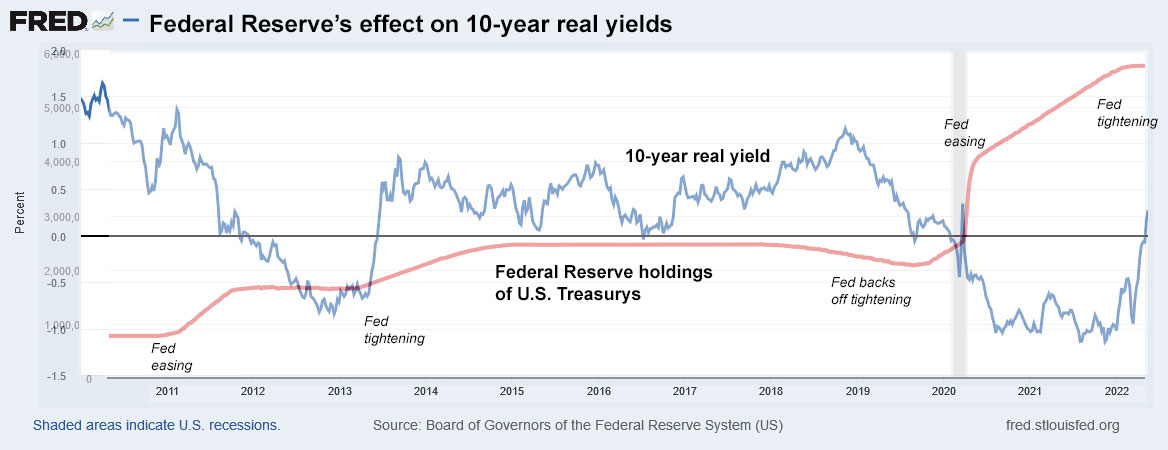

Here is a long-term view of 5-, 10- and 30-year real yields through several Fed easing and tightening cycles:

It’s been an “incredible” (too nice a word?) 11 years for TIPS, with real yields falling deeply negative under the weight of Federal Reserve quantitative easing, first in the 2011 to 2013 era, and then again after the pandemic outbreak in 2020. The period of 2015 to early 2019 was a time of “implied tightening” by the Fed. It was raising interest rates, but not dramatically reducing its balance sheet of Treasurys.

Notice how the yield curve flattened in early 2019, after several years of the Fed’s moderate actions. Now, in June 2022, the Fed is acting much more aggressively, with a 0.75-basis-point increase in short-term interest rates looking likely this week, plus sizable monthly efforts to reduce its balance sheet. The Fed knows it has to act as inflation is surging globally.

So, I do expect real yields to continue to rise, and the yield curve to flatten as fear grows of an economic slowdown. But even with higher yields “possible” in the future, I’d be a buyer of individual TIPS in this current market of reasonable yields and very high inflation. We can’t be sure of the Fed’s future actions.

Next week … A 5-year TIPS auction

The Treasury will be holding a reopening auction June 23 for CUSIP 91282CEJ6, creating a 4-year, 10-month TIPS. That TIPS is currently trading on the secondary market with a real yield of 0.66% and an unadjusted price of $97.45 for $100 of value. It’s looking attractive, in my opinion. But a lot can change, as the last two weeks have shown.

I’ll be posting a preview article on that auction on Sunday.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

As a courtesy to the TipsWatch community, you are welcome to use a webpage I wrote for my personal use,…