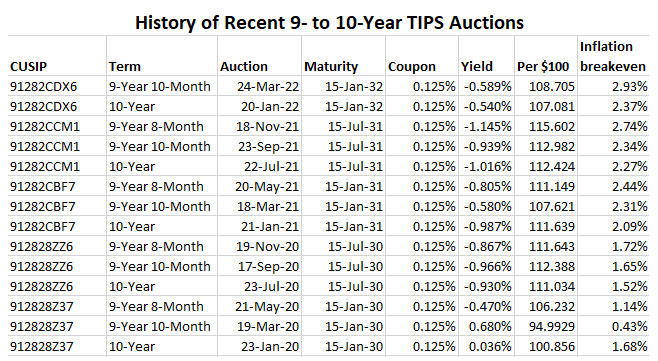

The inflation breakeven rate hit 2.93%, the highest in history at auction for this term.

By David Enna, Tipswatch.com

Even with U.S. inflation raging, it appears the U.S. Treasury is finding difficulty in drawing strong demand for Treasury Inflation-Protected Securities. Thursday’s reopening auction of $14 billion in CUSIP 91282CDX6 generated a real yield to maturity of -0.589%, a bit higher than looked likely just minutes before the auction closed at 1 p.m.

This TIPS, which can be purchased on the secondary market, had been trading all morning with a real yield in the range of -0.63% to -0.64%. The auction result came in 5 basis points higher — not a huge difference but an indication of lukewarm demand.

CUSIP 91282CDX6 carries a coupon rate of 0.125%, which was set at the originating auction on January 20. That auction also was met with weak demand. It’s likely that big-money TIPS investors are sitting back and waiting for rising real yields in future offerings, which seems likely as the Federal Reserve begins raising short-term rates and unwinding its huge balance sheet of U.S. Treasurys.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or in this case, below) inflation.

Investors in today’s auction had to pay a sizeable premium above par value for this 9-year, 10-month TIPS. The adjusted price was about $108.70 for about $101.40 of principal, after accrued inflation is added in. This TIPS will carry an inflation index of 1.01396 on the settlement date of March 31.

The real yield of -0.589% means that this investment will trail official U.S. inflation by 0.589% over the next 9 years, 10 months. Does that make it unattractive? Not necessarily, with U.S. inflation currently running at 7.9%. And this TIPS will get an immediate inflation boost of 0.91% in April, reflecting non-seasonally adjusted inflation in February. An equally high number looks very likely in May.

Here is the trend in 10-year real yields over the last two years, showing how real yields sank below zero as fear of the pandemic erupted in March 2020:

Inflation breakeven rate

With a 10-year nominal Treasury trading today with a yield of 2.34%, this TIPS gets an inflation breakeven rate of 2.93%, the highest in history for any 9- to 10-year TIPS auction. This breakeven rate is 56 basis points higher than the 2.37% recorded at the originating auction, just two months ago. That shows how dramatically inflation expectations have increased in 2022.

Will inflation average 2.93% over the next 10 years? I would tend to think it will be lower, but in the near term inflation is likely to continue at a high rate, probably at least 4% to 5% over the next year. Key question: Will the Federal Reserve act aggressively enough to clamp down on inflation, which is becoming an international phenomenon?

Here is the trend in the 10-year inflation breakeven rate over the last two years, showing the steady surge higher since the pandemic outbreak, which was followed by aggressive stimulus measures by the Federal Reserve and Congress:

Reaction to the auction

This is a hard one to judge. Clearly, the auction brought a higher-than-market real yield, which indicates lukewarm demand. But the bid-to-cover ratio was a decent 2.43, better than the 2.30 recorded at the January auction.

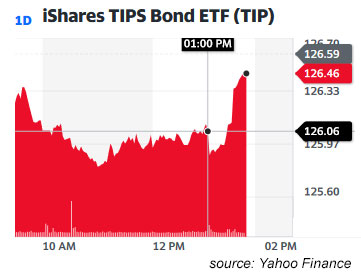

The TIP ETF, which holds the full range of TIPS maturities, had been trading slightly lower all morning, indicating slightly higher yields. After the auction closed at 1 p.m. EDT, the ETF took a slight dip and then began climbing higher. So it looks like the auction got an acceptable result.

Even more bizarre: At 1:45 p.m., this same TIPS was trading on the secondary market with a real yield of -0.67%, a pretty big swing lower after the auction set the market at -0.589%. So it goes in the always confusing TIPS market.

After the auction closed, I got this reaction from an institutional market-marker with expertise in TIPS:

“What was interesting to me was that the stats had turned to stronger demand – only 10.6% primary dealer takedown and 2.43 bid to cover, both much better than last couple auctions. What that indicates to me is there is still elevated demand for inflation protection, just at the right price. I don’t expect this demand to ebb until we start to actually see some weakness in realized CPI.”

Anyway, for investors, the higher-than-market yield was a positive result. Disclosure: I made a small purchase of this TIPS in a brokerage account, mainly to test how prices are reported.

This TIPS will be reopened again at auction on May 19. Here is a history of recent TIPS auctions of this term:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I appreciate your timely articles. Just bought my first TIPS today in my IRA account. I’m glad to see the yield is a little better than it looked earlier today. I wonder what the next reopening of this TIPS will bring.

Reflects the sentiment of retail investors? They think dollar-cost averaging into the S & P 500 index guarantees all will be well. ( The index just completed the best two year run since 1937.) Or is it they believe the Federal Reserve will easily tame inflation? This time?

Thank you David. Is it correct that were are now clearly in the period of the Fed tapering its TIPS purchases? If so, how might this affect things? I would expect yields to increase with tapering (price drops), following your post of 6/20/2021. As I recall, the Fed has a very large balance sheet of TIPS. Or perhaps not much will happen in terms of yields as people wait for rates to broadly increase more. Interesting guesses.

This is a great point. March 2022 is the last month of Fed purchases of Treasurys and so tapering ends this month. The Fed still holds about $8.9 trillion of assets on its balance sheet, and will continue rolling those over until it begins reductions. FYI, it looks like the Fed’s last purchase of TIPS was on March 1. (It doesn’t buy new holdings at auction) https://www.newyorkfed.org/markets/domestic-market-operations/monetary-policy-implementation/treasury-securities/treasury-securities-operational-details

Thank you for your update. I was glad to see the order trigger at a higher yield.