I Bonds remain the preferred inflation-protected investment. But a 5-year TIPS could be an addition to your inflation-fighting arsenal.

By David Enna, Tipswatch.com

The U.S. Treasury will offer $20 billion in a new 5-year Treasury Inflation Protected Security at auction on Thursday. This is CUSIP 91282CEJ6, and the coupon rate and real yield to maturity will be set by the auction results.

As of Thursday’s market close (no data for Good Friday), the Treasury estimated the real yield of a 5-year TIPS at -0.54%, a remarkable 104 basis points higher than where we started this year. Real yields — especially for shorter- and medium-term TIPS — have been surging in response to the Federal Reserve’s commitment to raise short-term nominal rates and also begin reducing its huge balance sheet of U.S. Treasurys.

The Fed stopped buying TIPS and other Treasurys in mid March and also “generally agreed” that it is prepared to reduce its balance sheet of Treasury issues by up to $60 billion a month. This could possibly begin in May. The result “should” be higher interest rates across all maturities.

Consider this: In Thursday’s auction, the Treasury will be offering $20 billion in a new 5-year TIPS, the highest auction amount in history for this term, and up 10% from the same offering a year ago. But at the same time, the Treasury won’t be adding TIPS to its balance sheet, and is preparing to let its balance sheet decline, meaning no reinvestment. Again, this “should” result in higher interest rates.

If the history of the last tightening cycle repeats itself, we should see 5-year TIPS real yields rise at least another 100 basis points. But that forecast is highly uncertain, because if inflation continues surging then demand for TIPS will be very strong, which will support yields at this level. On the other hand, if the U.S. economy sinks into recession, the Fed will likely launch another era of stimulus, and 5-year real yields could sink deeply negative.

Got it? The future is uncertain.

For that reason, I am not opposed to nibbling into this auction, if 5-year real yields hold in the -0.50% range this week. The one great thing about a 5-year TIPS is that the term is only 5 years. Even though you’ll pay a premium price, you probably won’t lose money and could do decently if inflation continues at a moderately high pace.

But wait, how can you lose money on a TIPS, an investment that guarantees return of your original par value? That’s true in “normal” times, when TIPS have real yields positive to inflation. In the current market, with negative real yields, buyers pay a premium price over par to invest in TIPS, and the premium is not guaranteed to be returned at maturity. I don’t think this has ever happened in TIPS history, but it is “possible.”

Here is a history of the 5-year real yield over the last five years, showing how the yield surged to an attractive level (around 1.0%) during the closing days of tightening in late 2018 and then plummeted in response to the Fed’s quantitative easing following the pandemic surge of March 2020:

What to expect

Definition: The “real yield” of a TIPS is its yield above or below official U.S. inflation, over the term of the TIPS. So a real yield of -0.54% means this TIPS will trail U.S. inflation by 0.54% for 5 years. A negative real yield isn’t necessarily a bad investment; the quality of the investment will depend on whether inflation rises above expectations in future years.

If the real yield holds at around -0.54% at Thursday’s auction, the coupon rate will be set at 0.125%, the lowest the Treasury will go for any TIPS. That means investors will be paying a premium price, because the real yield to maturity will be much lower than the coupon rate. The price should be roughly about $103.70 for $100.42 of value, after accrued inflation is added in. The inflation index will be 1.00424 on the settlement date of April 29.

Key point: Investors also know that in May, principal balances for this TIPS will get an immediate boost in value of 1.34%, the rate of non-seasonally adjusted inflation in March. That’s pretty appealing. I’m expecting demand to be reasonably strong, but recent TIPS auctions have received lukewarm investor interest.

Inflation breakeven rate

With a 5-year nominal Treasury closing last week at 2.79%, this TIPS has a current estimated 5-year inflation breakeven rate of 3.33%, a rather lofty number. That means that for this TIPS to outperform a nominal Treasury of the same term, inflation would have to average 3.33% over the next 5 years. I think investors are front-loading a lot of inflation in 2022, but then see it dropping to a rate of 4% to 5% by the end of the year. After that …. er … the future is uncertain.

I can track 5-year inflation breakeven rates back to 2003, and at no time — until the last several months — has the 5-year inflation expectation ever exceeded 3%. We have entered a new era.

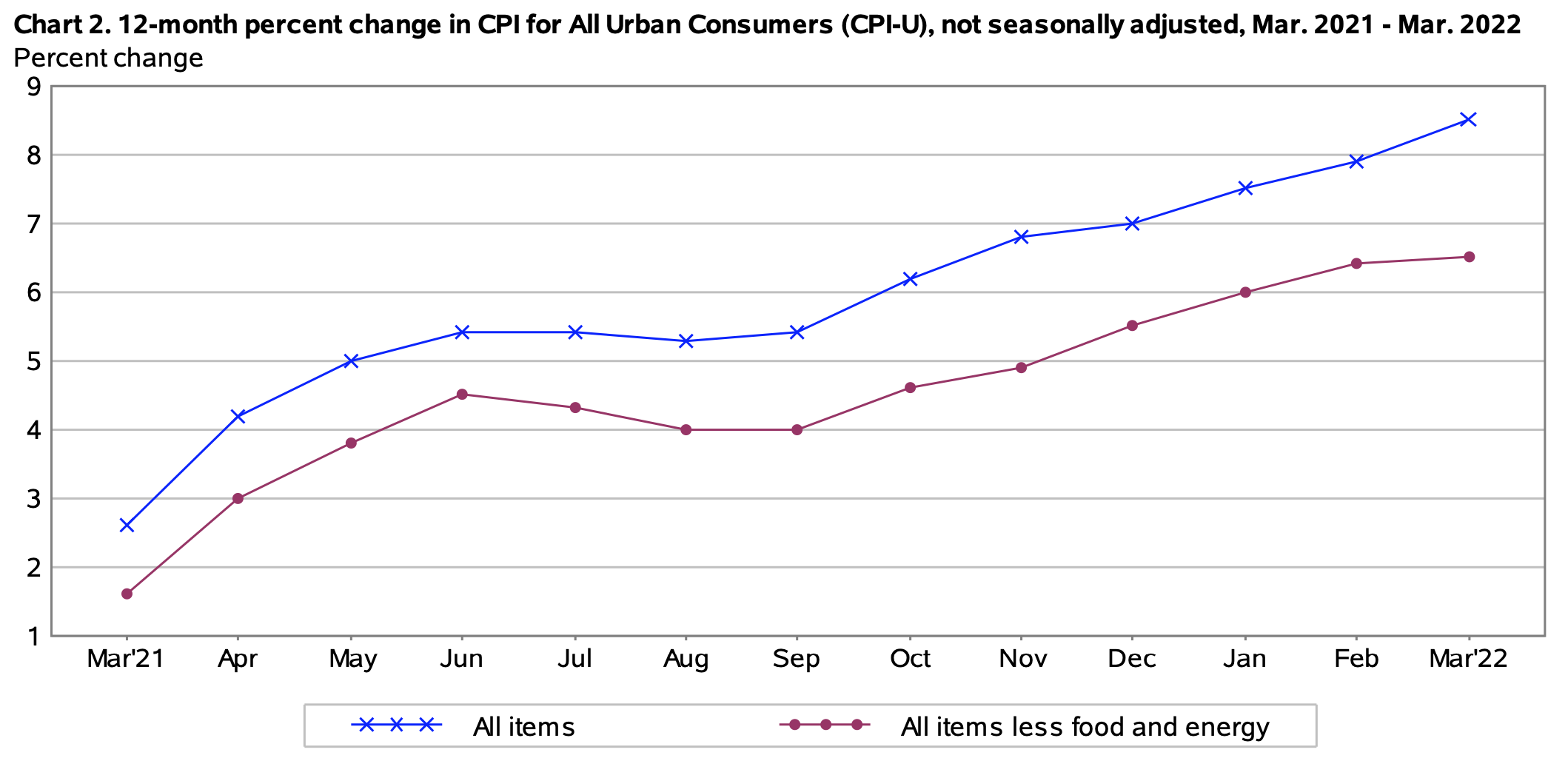

The inflation breakeven number is important because it tells you the relative cost of a TIPS investment. A high inflation breakeven rate — anything above 2.75% — means a TIPS is “expensive” versus a nominal Treasury of the same term. We are well above “expensive” at this point, but rightly so with U.S. inflation currently running at a annual rate of 8.5%.

Here is the trend in the five-year inflation breakeven rate over the last five years, showing the surge higher in the aftermath of aggressive economic stimulus by both the Fed and Congress in the wake of the pandemic surge two years ago:

Obvious alternative: I Bonds

Over the last two years, I have recommended putting your first $10,000 inflation-protected investment (per person) into I Bonds, which have an effective real yield of 0.0%, currently 54 basis points higher than a 5-year TIPS. In essence, I Bonds would be about 3.3% more valuable than a 5-year TIPS, if I Bonds could be traded on an open market (they can’t be).

I Bonds remain the superior investment, across pretty much the entire TIPS maturity spectrum, since I Bonds can be redeemed after five years with no penalty, or held for 30 years if that is what you desire. Plus, taxes on the interest is tax-deferred, and I Bonds provide better deflation protection.

However … there is always a however … things will change when and if real yields on TIPS rise well above zero. At that point, the equation shifts toward individual TIPS, because there is no annual purchase limit. I’d still buy I Bonds, though. I always buy I Bonds, just in case we hit a bizarre scenario like we are seeing in April 2022: high inflation and very low nominal rates.

Another investment to consider for the future is 5-year insured bank CDs, which even at the best-in-nation banks are now paying a pathetic 2.0%, well below the 5-year Treasury note at 2.79%. In my opinion, this is a scandal, but the National Enquirer won’t be doing any front page stories on it. If you are thinking about a bank CD, it’s probably still better to look at 1-year CDs and try to get more than 1% in a time of 8.5% inflation. Or, even better, the 2-year nominal Treasury is paying 2.47% right now; it is the “sweet spot” of the nominal Treasury curve.

Conclusion

This 5-year TIPS auction, viewed outside of the current Fed hiking trend, is ugly but attractive enough. I might chip in with a small (very small) purchase to keep my TIPS ladder interesting. Higher real yields seem highly likely in the future, but as I seem to say often … the future is uncertain.

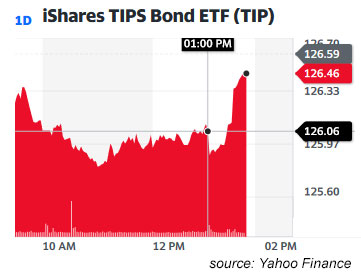

This auction closes for non-competitive bids at TreasuryDirect at noon EDT on Thursday. If you are buying through a brokerage account, you should make your purchase either Wednesday evening or early Thursday, because auction orders close early at brokerages. I will be posing the auction results soon after it closes at 1 p.m. EDT Thursday.

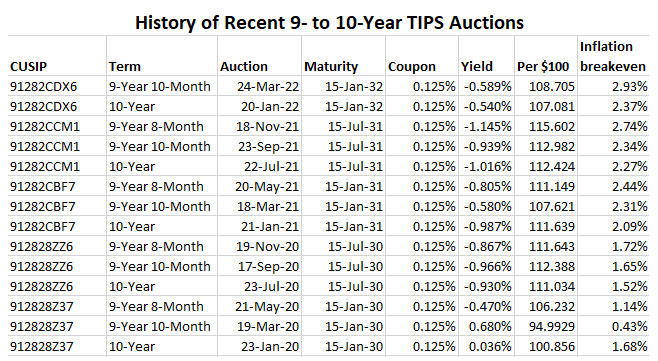

Here is a history of 4- to 5-year TIPS auctions over recent years. Notice that at the tail-end of the last Fed tightening cycle a 5-year TIPS reopening on December 20, 2018, generated a real yield of 1.129%. Eventually, we could be heading there?

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…