Thursday’s auction of a new 10-year TIPS will get a real yield nearly 50 basis points higher than a similar auction in November. But is that enough?

By David Enna, Tipswatch.com

The U.S. Treasury will offer a new 10-year Treasury Inflation-Protected Security at auction on Thursday, and the real yield to maturity will almost certainly be a negative number. A negative yield? Does that mean investors will earn less than zero on this investment? Of course not.

I bring this up because the New York Times ran an article this week implying that investors in TIPS are guaranteed to lose money on their investment. Utterly ridiculous, and the New York Times should know better. Here is what the Times reported:

“People assume ‘just because inflation goes up, you’ll do well’ with TIPS, said Lynn K. Opp, a financial adviser with Raymond James in Walnut Creek, Calif. But other factors, like rising interest rates, can sap TIPS’s returns, she said.

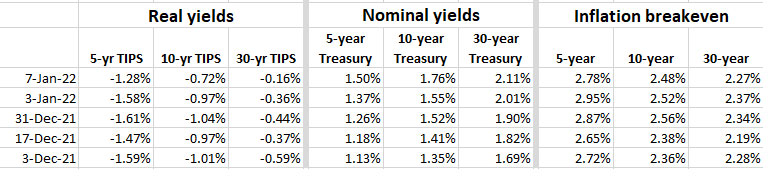

“Plus, TIPS are expensive when compared with standard Treasuries in that they pay less interest, Ms. Opp said. In the first week of January, a five-year TIPS was yielding minus 1.7 percent, while a five-year Treasury was yielding 1.4 percent. In effect, TIPS investors were paying the Treasury to hold their money.

No. No. No. I know that TIPS can be a complicated investment to understand, but any financial advisor should know that a real return of -1.7% means only that the investment will lag official U.S. inflation by 1.7% a year over its term. Inflation currently is running at 7.0%, which translates to a nominal return of 5.3% for that TIPS, much better than the nominal Treasury at 1.4%. If inflation falls to 4%, that TIPS would yield 2.3%, still much better than 1.4%.

A negative real return does not mean a negative nominal return. And a positive nominal return — as you can get on that 5-year Treasury paying 1.4% — does not mean a positive real return. Simple as that.

One more point on that Times article: A 5-year TIPS never had an estimated real yield of -1.70% in January. The lowest it got was -1.56% on Jan. 4, and that yield had increased to -1.24% on the date the article was published. This is sloppy reporting. TIPS have pluses and minuses, but paying the Treasury to hold your money is not an issue.

Rant over. On to the auction.

The Treasury on Thursday will offer $16 billion in a new 10-year TIPS — CUSIP 91282CDX6. The real yield to maturity and coupon rate will be set by the auction, but we can be sure the real yield will be negative and the coupon rate will be set to 0.125%, the lowest the Treasury will go on a TIPS.

The best source for estimating the real yield of a new TIPS is the U.S. Treasury’s Real Yields Curve page, which updates an estimate each day at the close of trading. As of Friday’s market close the Treasury was estimating that a full-term 10-year TIPS would yield -0.66%, which is up 31 basis points from the start of the year.

Real yields (and nominal yields, too) have been rising after the Federal Reserve signaled it is ready to end its aggressive bond buying by March, and also likely to begin raising short-term interest rates in that month. We could see as many as four increases in short-term rates in 2022, and eventually, the Fed should begin reducing its $8.8 trillion stockpile of Treasurys and mortgage-backed securities.

So we could see real yields continue to climb before Thursday’s auction, but both the bond and stock markets seem to be heading into a volatile phase.

If the auction does result in a real yield of -0.66%, that should result (roughly) in an unadjusted price for investors of about $107.85 for $100 of par value. This TIPS will carry an inflation index of 1.00253 on the settlement date of Jan. 31, which means the adjusted price should be around $108.12 for $100.25 of value, after accrued inflation is added in.

Reminder: that’s a rough estimate, and things change. But investors should be prepared for that higher cost, which is necessary because the real yield to maturity will be well below the coupon rate of 0.125%.

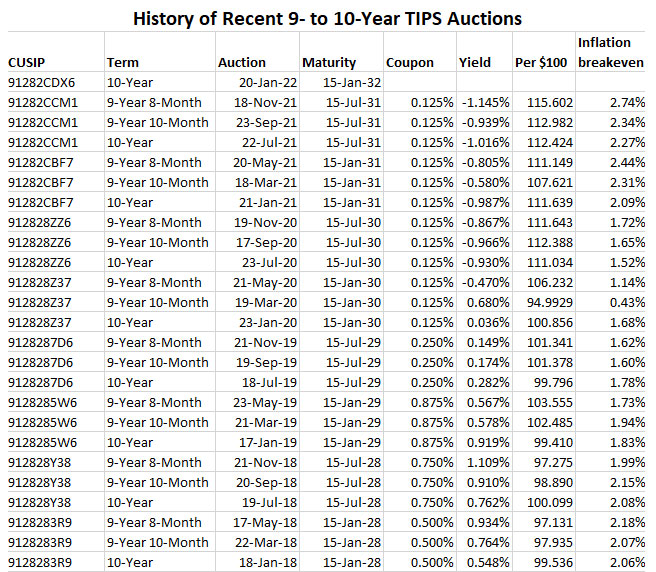

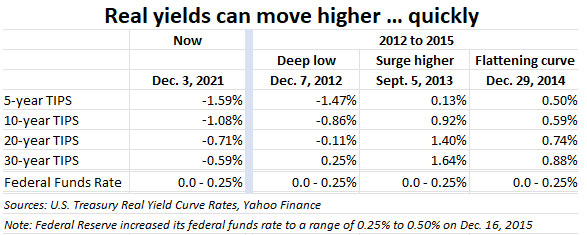

Is a real yield of -0.66% attractive? Hey, at least it is well above the record low of -1.145% set at a TIPS reopening auction in November. That TIPS carried a premium cost of 15%. So this TIPS should get a real yield about 48 basis points higher than investors accepted just two months ago.

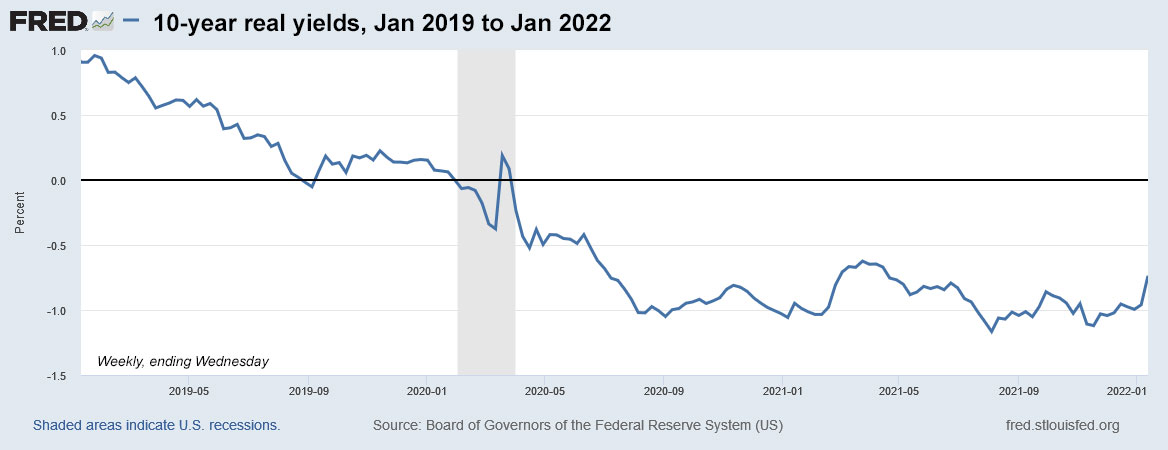

The key question is: Will this trend of rising real yields continue through 2022, making later auctions of this term more attractive? I’d say that is likely, but nothing is certain. Here is the trend in 10-year real yields over the last three years:

This chart is interesting because it shows that 10-year real yields were closing in on 1.0% in early 2019, following a period of Federal Reserve tightening. That could be the “new normal” for 2023 and beyond if the Fed stays on course to raise rates and reduce its balance sheet. However … the Fed does change course quickly. Back in 2019, it backed off and began reducing interest rates after the stock market had a volatile month in December 2018. More on that.

Inflation breakeven rate

With a nominal 10-year Treasury note yielding 1.78%, a 10-year TIPS would currently have an inflation breakeven rate of 2.44%, which seems reasonable (and actually attractive). I can visualize inflation running at a rate of 3% or higher over the next decade, but that would be a dramatic break from the last decade of lower-than-expected inflation.

Simply put, a lower inflation breakeven rate indicates that a TIPS is getting more attractive versus a nominal Treasury of the same term. Would I want to invest in a 10-year Treasury yielding 1.78%? No. Would I want to invest in a TIPS that would lag official inflation by 0.66% over 10 years? Maybe, because the TIPS offers protection against unexpectedly high inflation. We could be entering an era of unexpectedly high inflation.

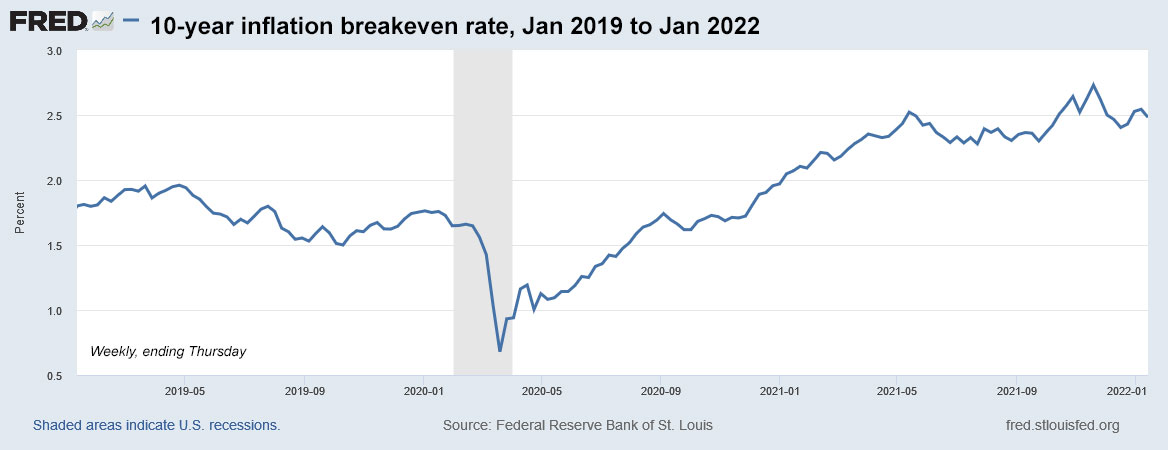

Here is the trend in the 10-year inflation breakeven rate over the last three years, showing the massive surge higher after the pandemic mania of March 2020, and the less dramatic dip lower in recent weeks, in reaction to the Federal Reserve’s potential actions to tamp down inflation:

Conclusion

I can see the appeal of this auction, with real yields rising nearly 50 basis points since the last auction of this term in November. But will we see higher real yields later this year? The Treasury schedules opening and reopening auctions of this term every other month, so there will be a lot of opportunities. I’ll probably pass.

Also, remember that the first $10,000 you invest in inflation production in 2022 should go to U.S. Series I Savings Bonds, which in effect have a real yield of 0.0%, 66 basis points higher than a 10-year TIPS. In reality, that means an I Bond is about 7.5% more valuable than a 10-year TIPS, plus it offers better deflation protection, a flexible term and tax-deferred interest.

Thursday’s auction result closes at 1 p.m. EST for non-competitive bids, like the ones made at TreasuryDirect or a brokerage. I’ll be reporting on the auction results soon after the close. In the meantime, here is the recent history of TIPS auctions of this term. Note that Thursday’s result will be the 11th consecutive auction with a negative real return:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I meant regarding 'wait it out' on I-bonds... but to me, TIP bonds right now are a horse of a…