May 2, 2022 update: Treasury holds I Bond’s fixed rate at 0.0%; composite rate soars to 9.62%.

By David Enna, Tipswatch.com

Based on the March inflation report, which concluded the six-month rate setting period for the U.S. Series I Savings Bond, the inflation-adjusted variable rate of the I Bond will rise from the current annualized 7.12% to 9.62% as of the May 1 reset.

This is for all I Bonds, no matter when you purchased them. All I Bonds will get six months of the 9.62% interest rate, but the starting month for the new rate will depend on the month the I Bond was originally issued.

Here are the official inflation numbers used in this calculation:

The 7.12% variable rate was already a record high for the I Bond, which was first issued in September 1998. So the new rate of 9.62% will crash through that record high. Possibly, we may never see a rate this high again. Economists have speculated that the March inflation report will set the peak and now we will begin a gradual slide lower. But … who knows?

For a much more detailed discussion of these savings bonds, read my Q&A on I Bonds.

For reasons to use I Bonds as part of your emergency fund, read the I Bond Manifesto.

Stick with the buying strategy!

While waiting for the May 1 reset might look tempting to launch directly into the 9.62% rate, I still strongly recommend buying I Bonds before April 30, which will lock in a 7.12% rate for a full six months, followed by 9.62% for six months. That’s an annual rate of about 8.4%, and there is no other very safe investment that can match that return.

I Bonds must be held for 12 months before you can redeem them. If you redeem them before five years, you will forfeit the last three months of interest. But if you buy near the end of April 2022, you will get full credit for April and can redeem 14 months and a few days later, avoiding taking the interest penalty on the 9.62% rate.

However, I always recommend buying I Bonds every year up to the purchase cap of $10,000 per person per year and holding them until you actually need the money. People who have been buying I Bonds for years — like many of my readers — are very happy right now, collecting an annual rate of 8.4%, plus any fixed rate attached to the original purchase.

Will the I Bonds’s fixed rate rise on May 1?

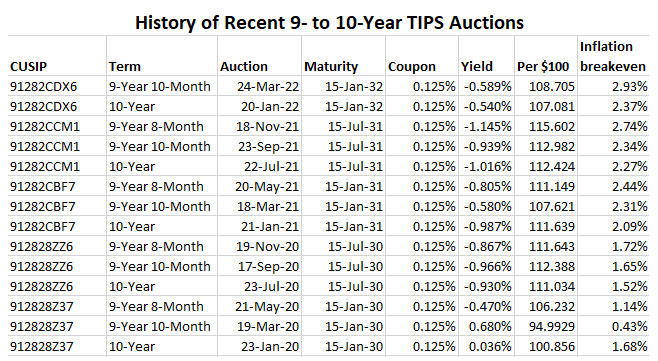

I still say “no,” but conditions are getting better for a fixed rate higher than the current 0.0%. The real yield of a 10-year TIPS has now “surged” to -0.12%, an impressive rise of 85 basis points since the beginning of the year. But until it gets to at least 0.25%, I think it’s unlikely the Treasury will increase the I Bond’s fixed rate. We might see the rate rise in November, which would be available to grab when the calendar resets in January.

My advice: Don’t be waiting for a higher fixed rate that might never come, and miss out on the chance to make $840 on a $10,000 investment in one year. Invest up to the cap before May 1.

The March inflation report

Once again, this was a stunner.

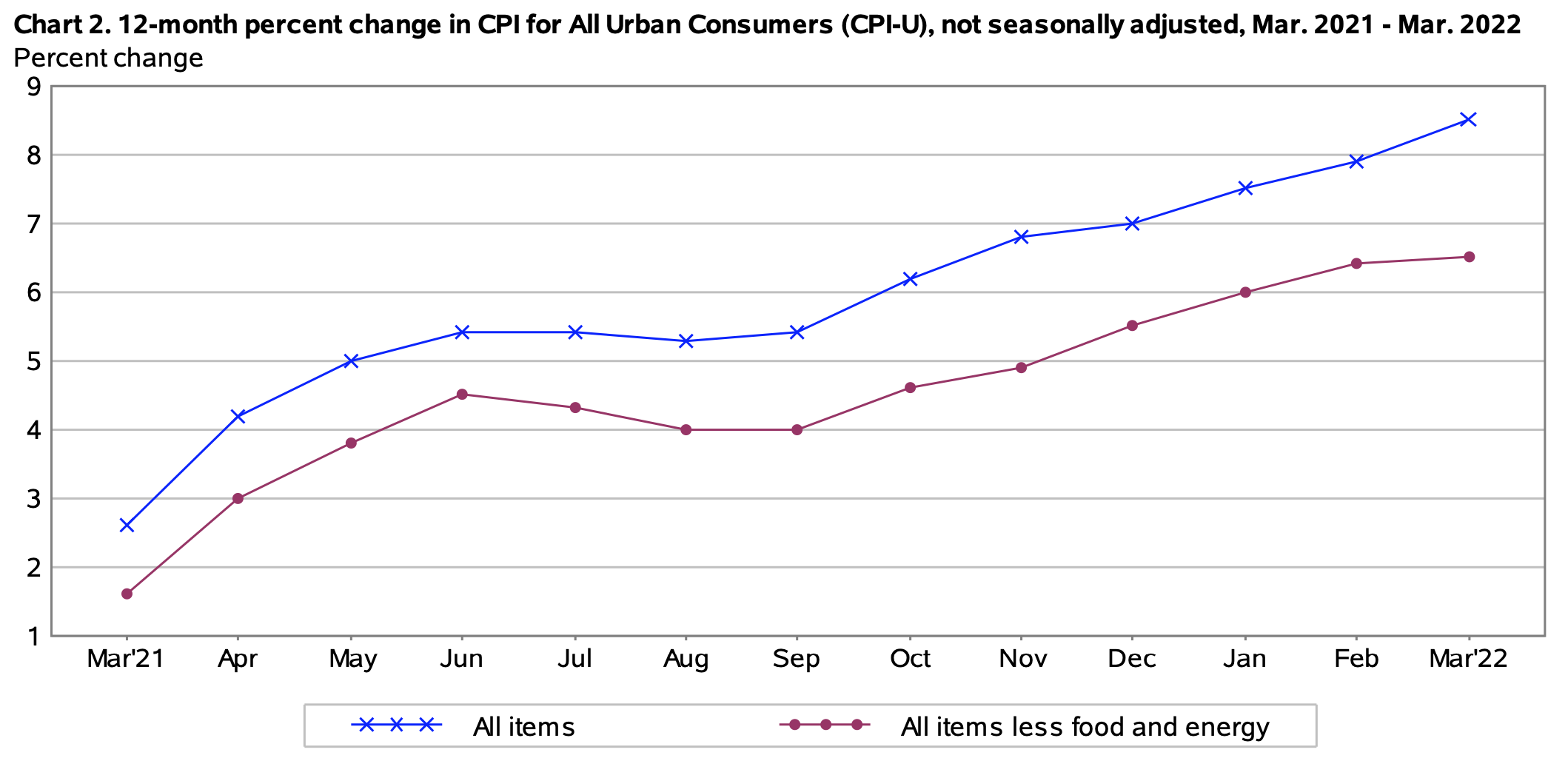

The Consumer Price Index for All Urban Consumers increased 1.2% in March on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all-items index increased 8.5%.

Both the March and year-over-year number were higher than the consensus forecast, which has happened repeated for the last six months. However, core inflation — which removes food and energy — came in lower than expectations for the month (at 0.3%) and year-over-year (at 6.5%, the highest level for core inflation since August 1982.)

So economists might view this report as a “mixed bag,” but American consumers are seeing nothing positive about it. The year-over-year number of 8.5% was the largest 12-month increase since the period ending December 1981. Inflation is surging across almost all areas of the U.S. economy:

- Gasoline prices rose 18.3% in March and accounted for over half of the all items monthly increase, the BLS said.

- Food prices rose 1% for the second month in a row and are now 8.8% higher over the last year. That’s the highest annual level since December 1981.

- Especially painful: the costs of food-at-home increased 2.0% in March.

- The costs of shelter rose 0.5% for the month and are up 5.0% over the year. It seems likely that we will continue to see higher costs in this area as rents are adjusted higher.

- The index for airline fares rose 10.7% in March.

- One area with declining prices was used cars and trucks, down 3.8% but still up 35.3% over the last year.

Here is the overall trend for annual all-items and core inflation over the last year, showing the steady rise higher since September 2021. Many inflation-watchers believe inflation now will begin gradually declining, possibly to a rate of 4% to 5% by the end of the year. But the war in Ukraine has created huge volatility in fuel and food prices:

What this means for TIPS

Investors in Treasury Inflation-Protected Securities are also interested in non-seasonally adjusted inflation, which is used to adjust the principal balances of all TIPS. The March inflation report means that TIPS principal balances will rise 1.34% in May, after rising 0.91% in April. Here are the new May Inflation Indexes for all TIPS.

This year’s incredible surge in inflation demonstrates the value of placing (and keeping) a portion of your investment portfolio into inflation protection, provided by TIPS and I Bonds. When inflation surges unexpectedly, these investment become valuable insurance against losses.

For a more detailed look at TIPS, read my Q&A on TIPS.

What this means for future interest rates

As many of you know, I am writing this in the mid-afternoon in Catania, Sicily, near the end of a three-week holiday. I haven’t been tracking the Federal Reserve’s pronouncements, but obviously the Fed seems highly motivated to get interest rates higher to slow the pace of inflation. This report should add fire to the motivation.

On the positive side for the Fed, core inflation was slightly lower than expectations. But that could be caused simply by consumer spending shifting to higher food and fuel costs, leaving less disposable income. There is no evidence that inflation will suddenly plummet, so the Fed needs to stay on this course. It could take years, unless the economy slips into a deep recession.

At some point, the real yields provided by TIPS should become competitive with I Bonds and eventually surpass the I Bond’s fixed rate, even if the fixed rate rises later this year. It will be good to see TIPS back as an attractive inflation-fighting investment.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I'm already familiar with the product and was curious if Tipswatch had ever done any rate predictions for it, like…