While annual inflation dipped slightly, inflation continues to run hot — too hot for complacency by the Federal Reserve.

By David Enna, Tipswatch.com

When is a surprise not a surprise? When it comes to economists trying to predict U.S. inflation.

All-items U.S. inflation rose 0.3% in April, exceeding economist predictions of 0.2% for the month and continuing a string of monthly upside surprises. The year-over-year number was 8.3%, also exceeding expectations of 8.1%. Core inflation looked even worse, coming in at 0.6% for the month (beating expectations of 0.4%) and 6.2% for the year (versus 6.0%).

The stock market’s instant reaction was negative. Just minutes before the Bureau of Labor Statistics released the report at 8:30 a.m., S&P 500 stock market futures were trading at 3996. Minutes after the report, futures were down to 3969.

In April, U.S. inflation rose 0.3% even though the price of gasoline — a major factor in the monthly all-items report — actually declined 6.1%, but remained 43.6% higher year over year. Already, this trend has reversed, with gas prices rising to record highs in May.

The BLS noted that increases in the indexes for shelter, food, airline fares, and new vehicles were the largest contributors to the seasonally adjusted all-items increase. Some highlights:

- The food at home index rose 1.0% in April, the fourth month in a row with price increases higher than 1%. Year over year, food at home prices were up a painful 10.8%.

- Food prices have increased 17 months in a row. The BLS noted that the index for dairy and related products rose 2.5%, its largest monthly increase since July 2007. The index for eggs increased 10.3% in April.

- Shelter costs increased 0.5% for the month and are now up 5.1% year over year. Shelter costs are a lagging indicator and should be a factor in higher inflation in coming months.

- The cost of used cars and trucks fell 0.4% in April, but are still 22.7% higher year over year. The index for new vehicles was up 1.1% for the month.

- Apparel prices also fell 0.8% in the month.

- The index for airline fares increased a mammoth 18.6% in April, the largest one-month increase since the inception of the CPI-U series in 1963.

- Costs of medical care increased 0.5% in April and are up 3.5% year over year.

Here is the trend in all-items and core inflation over the last year, showing that annual inflation did peak in March, but remained at a very high level in April:

A side note: The separate inflation index — CPI-W — used to determine Social Security’s annual cost of living increase has increased 8.9% over the last 12 months, a bit higher than overall U.S. inflation. But the Social Security increase for 2023 will be determined by the average of inflation from July to September. It’s too early to draw any conclusions.

What this means for TIPS and I Bonds

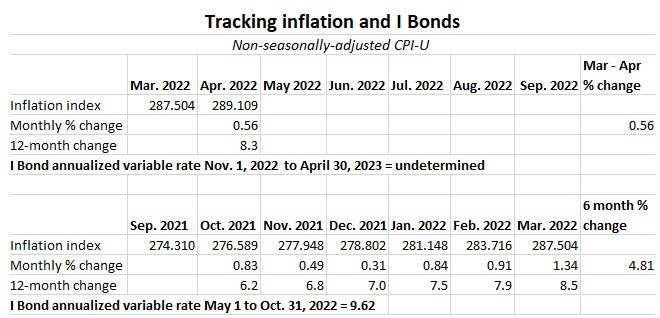

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For April, the BLS set the inflation index at 289.109, an increase of 0.56% over the March number.

Keep in mind that since non-seasonally adjusted inflation was running higher than the seasonally adjusted number in April, this will eventually reverse in coming months. The two numbers merge after 12 months.

For TIPS. The April inflation number means that principal balances for all TIPS will rise 0.56% in June, after rising 0.91% in April and 1.34% in May. Here are the new June Inflation Indexes for all TIPS.

For I Bonds. The April inflation index is the first of a six-months string — from April to September — that will determine the I Bond’s new inflation-adjusted variable rate, which will be reset on November 1. So far, that 0.56% number would translate to a variable rate of 1.12%, but it’s way too early to draw any conclusions from just one month. Inflation can be highly volatile in summer months.

Here are the data I’m tracking:

What this means for future interest rates

While annual inflation slipped slightly lower in April, the upside surprises for both all-items and core inflation indicate that the Federal Reserve has to stay the course with balance-sheet reductions and routine increases of 50 basis points in short-term interest rates.

I think the bond market has already priced in this trend, with the 5-year nominal Treasury rising above 3% earlier this week. The real yield of a 5-year TIPS is inching ever closer to zero and should quickly rise to positive, if the Fed stays the course and attempts to hold down inflation expectations.

I don’t expect annual U.S. inflation to continue above 8% for long. It should begin gradually slipping lower in coming months, possibly ending the year in the 4% to 5% range. This is what the market expects, but a lot will depend on if the U.S. economy can remain reasonably strong at a time of soaring energy prices and rising interest rates.

Next week’s reopening auction of a 10-year TIPS should be interesting. That TIPS is currently trading on the secondary market with a real yield of 0.32% and a price discounted to par. We haven’t seen that in a long time. I will be writing a preview article on that auction this weekend.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

UrsaTaurus, I have been contemplating similarly, buying long without the expectation of holding to maturity (I will be dead). I…