By David Enna, Tipswatch.com

The U.S. Treasury’s auction today of $16 billion in a new 10-year Treasury Inflation-Protected Security resulted in a real yield to maturity of -1.016%, the lowest in history for any TIPS auction with a 9- to 10-year term.

This is CUSIP 91282CCM1, and it was assigned a coupon rate of 0.125%, the lowest the Treasury will go for any TIPS.

A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or in this case, below) inflation.

In the case of CUSIP 91282CCM1, investors were willing to accept a real yield that will lag official U.S. inflation by 1.016% a year for 10 years. Why would they do that? Two reasons: 1) because a TIPS offers protection against unexpectedly high future inflation, and 2) the yield of a nominal 10-year Treasury — currently at 1.25% — is also highly likely to lag inflation, but with no upside potential. For many investors, a TIPS looks like the better option.

Investors at Thursday’s auction had to pay a steep premium price to collect that coupon rate of 0.125%, plus future inflation accruals. The adjusted price for this TIPS was about $112.42 for about $100.44 of value, after accrued inflation and interest are added in. This TIPS will have an inflation index of 1.00387 on the settlement date of July 30.

The auction appears to have gone off without a hitch. The real yield was a bit lower than the Treasury’s yield estimate of -0.98% at the market close Wednesday. But at 12:30 p.m., the most recent 10-year TIPS trading on the secondary market was yielding -1.03%. So -1.016% looks like a reasonable result. The auction’s bid-to-cover ratio was 2.5, a solid if not stellar number.

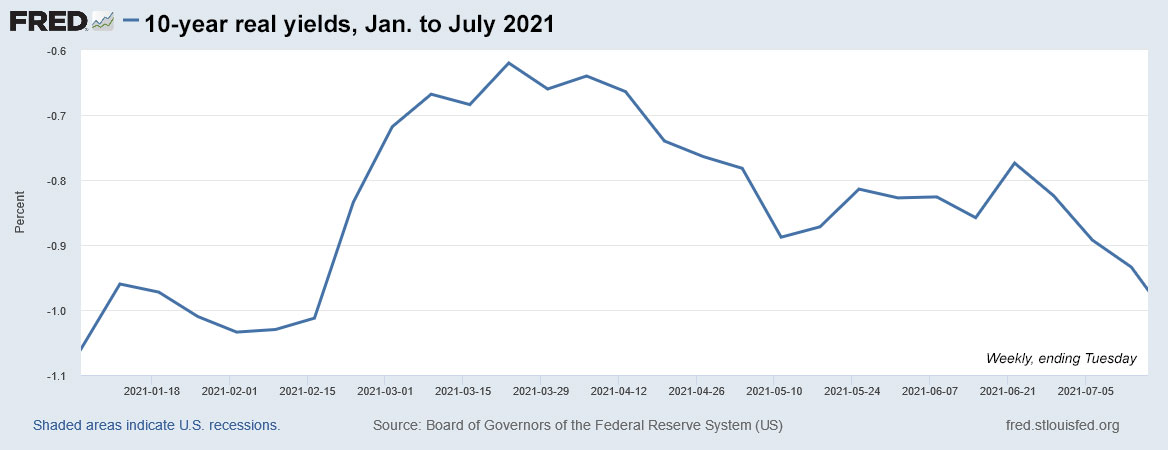

Here is the year-to-date trend in 10-year real yields, showing the recent dip in yields as the delta variant of COVID-19 raises fears of a future economic slowdown:

This recent dip, however, is remarkable because it has followed the Federal Reserve’s June 16 “talking about talking about” meeting that should be setting a course toward tapering of its aggressive bond-buying program. When that bond buying ends — if it ever ends — both nominal and real yields are almost certain to rise.

Inflation breakeven rate

The one oddity of this auction is a dip the 10-year inflation breakeven rate for this TIPS, which came in at 2.27%, a bit below recent auctions of this term. The breakeven rate is determined by subtracting the real yield of this TIPS (-1.016%) from the current nominal yield of a 10-year Treasury (1.25%). The result is 2.27%. It means that this TIPS will outperform its nominal counterpart if inflation averages more than 2.27% over the next 10 years.

While 2.27% is high by historical standards, it seems reasonable given recent trends, with official U.S. inflation running at an annual rate of 5.4% as of June. So it is interesting to see that inflation expectations are now beginning to ease.

Here is the trend in the 10-year inflation breakeven rate for 2021 year to date:

Reaction to the auction

The TIPS ETF — which holds the full range of TIPS maturities — had been trading slightly higher all morning, indicating slightly lower yields. After the auction’s close at 1 p.m., the ETF ticked up, slightly. Not much to see here. This auction went off as expected.

Investors at today’s auction probably had to hold their noses to accept a record-low real yield for auctions of this term. However, the slight decline in the inflation breakeven rate reinforces the advantage of a TIPS over a nominal Treasury of the same term. Who wants to accept 1.25% for 10 years?

This TIPS will be reopened at auctions in September and November. It will be interesting to watch the trend in real yields through the end of the year.

Here’s a history of recent auctions of the 9- to 10-year term, dating back to January 2020. Note that today’s auction was the 8th in a row to get a negative real yield:

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: 10-year TIPS reopens Thursday: How low can it go? | Treasury Inflation-Protected Securities

Great article, covering the reasons I held my nose and bought yesterday! Thank you for a fantastic blog.

Thank you, Clark. Now that you have posted your first comment, future comments will go up automatically. Feel free to share advice, ask questions.