I know most of my readers are experienced investors who already have a TreasuryDirect account. If you know a less-experienced investor who could use this information, please pass it along. Thanks …

By David Enna, Tipswatch.com

The news that U.S. Series I Savings Bonds are now paying 3.54%, annualized, for six months is drawing a lot of attention from new investors, people who a few months ago would have laughed off any talk of investing in savings bonds.

This is good. I love when people learn about I Bonds and EE Bonds and appreciate them as valuable and viable investments. Yes, they are “relics” from the past, but that relic status is what makes them so attractive: They have terms that create a flow of interest income much higher than you’d find with any other “modern” safe investment.

But then there is the obvious question: How do you invest in I Bonds? You could ask your broker, but don’t expect any help there. Your broker can’t sell you I Bonds, and can’t make money from advising you to buy them. You can’t buy them on the “open market.” There is only one place to purchase I Bonds, and that is the U.S. government’s site, TreasuryDirect.gov.

What do you need to open an account?

TreasuryDirect says you need these these things to open an individual account:

- A taxpayer identification number … in other words, a Social Security Number.

- A United States address of record. Do you need to be a U.S. citizen? No. Do you need to be living in the U.S.? No. But you need a U.S. address to register the account.

- Be at least 18 years old. A child cannot open a TreasuryDirect account. But a parent or other adult guardian can open an account for a child and link it to the adult’s account.

- A checking or savings account … this can be at a physical or online bank, or at brokerage, such as Fidelity or Vanguard. You will need to know your account and routing numbers.

- An email address.

- A web browser that supports 128-bit encryption. TreasuryDirect states that its site is “optimized for Internet Explorer,” which is classic government dumbness. IE has been replaced by Microsoft Edge and today has a market share of less than 1%. TreasuryDirect even provides “helpful” links to Windows XP service packs that have long-ago been discontinued. TreasuryDirect works fine with Firefox and Chrome browsers. I have tested it with Edge and Safari, too, and it seems to work fine.

When you get to the “Account Type” page, choose “Individual.” (You can also open an account in the name of a trust, but I have no idea how that works.)

A married couple must open two separate TreasuryDirect accounts if both spouses wish to purchase I Bonds. Each account is limited to purchasing $10,000 per person per calendar year, so if you want to purchase $20,000 in a year, you need two accounts.

(There are separate purchase caps for I Bonds and EE Bonds, so an individual can buy $10,000 of both, for a total of $20,000. EE Bonds, by the way, are also an excellent 20-year investment in today’s market. I wrote about that in September 2019.)

Once you get to TreasuryDirect’s “Individual Account Application” page, you’ll need to fill in a lot of personal information — see why you need that 128-bit encryption? — including your Social Security number, date of birth, state driver’s license number and expiration date, mailing address, email address, and bank information.

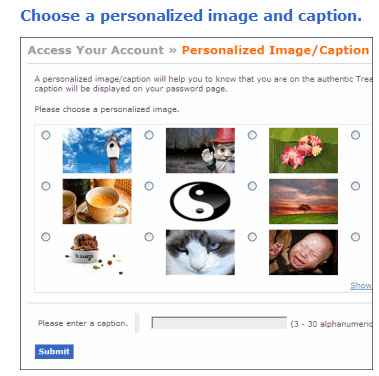

Then, TreasuryDirect will ask you to select a “personalized image and caption.” What’s this about? It is a safeguard against phishing attempts. If a scammer tries to get you to log into your TreasuryDirect account using a false address, you won’t see this image and caption. That’s a signal you are being scammed.

Next, you will choose your password. TreasuryDirect advises, “When selecting your password, avoid numbers, names and dates” that correspond to your personal information. I suggest creating a password that is UNIQUE to TreasuryDirect and not used elsewhere.

You’ll also be asked to answer three security questions, in case you forget your unique password. Favorite author? Favorite movie? And so on.

And that is it, on the last page of the account creation screens, you will be given your new account number (usually something like X-123-456-789). When you go to log later, you will be asked to provide your account number and password. As an additional security measure, you will be emailed a temporary security code to enter before you gain access to your account.

Registering your purchases

How you register a savings bond determines who owns the bond and who can cash it. The registration also determines what happens with the bond if the owner dies.

- One owner. Only one person is named as owner. Only that person can make transactions. If he or she dies, the bond becomes part of the estate.

- Owner and beneficiary. Only the owner can make transactions. If he or she dies, the beneficiary becomes the only owner. The beneficiary can’t be an entity. The registration says “PAYABLE ON DEATH,” or “POD.” Example of registration: JOHN DOE POD TO JANE DOE

- Two owners. For electronic bonds (the only option when buying through TreasuryDirect), the first-named owner is the primary owner; the second is secondary. The registration uses “WITH.” An example of this registration is JOHN DOE SSN 987-65-4321 WITH JANE DOE SSN 123-45-6789. If one owner dies, the other becomes sole owner. If one owner is a person, the other can’t be an entity like a trust.

These ownership rules throw a lot of investors for a loop, because they expect to see “Joint Ownership With Right of Survivorship” as an option. How is “with” ownership different from “joint ownership”? I don’t know, but for a married couple, I’d recommend using this “with” ownership, which should avoid issues after the primary owner’s death.

Using I Bonds for higher education

If you use interest from a Series I bond to pay for higher education, you may not have to pay federal tax on the interest. However:

- If you want to use the bond for your education, you must be the owner of the bond.

- If you want to use the bond for your child’s education, then you or your spouse, or both, must own the bond. Your child may be a beneficiary but not a co-owner.

- Your modified adjusted gross income has to be less than the cut-off amount set by the Internal Revenue Service. This amount typically changes every year. I believe the current caps are $84,950 for single taxpayers and $134,900 for married filing jointly, but a gradual phaseout of the benefit begins at lower income levels. See IRS Publication 970 “Tax Benefits for Education.”

Logging in for the first time

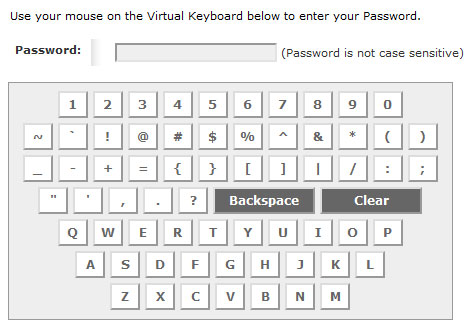

When you first log in, you will enter your account number (it looks something like X-123-456-789) and then you will get a notice that you must go to your connected email account for a one-time security code. Copy and paste that code into the box, submit, and you will come to the password entry page.

This is another security step. You enter your password using a virtual keyboard (it ignores upper and lower case). This security measure will keep keystroke-tracking viruses from learning your password. But you can see why you don’t want a 23-letter-long password. Keep it unique, and reasonable.

Here are the Treasury’s official password rules:

- Length. Use at least eight characters without spaces.

- Characters. Use at least one letter, one number, and one special character such as $ or %, but excluding “\”.

- Content. Avoid numbers, names, or dates that are significant to you. For example, your phone number, first name or date of birth. Try to choose a password based on a memory aid.

On this page, above the keyboard, you will also see the image and caption you selected in the registration pages.

Making your first purchase

After you complete the login process, you will see your account summary page, which should be pretty empty if this is your first purchase. Up in the top row of links, click on “BuyDirect” and you will go to the purchasing menu.

- Select Series I

- On the next page, your preferred registration should be filled in, such “Person1” or “Spouse1 WITH Spouse 2”

- Enter the purchase amount, up to $10,000 per account per calendar year.

- Select the source of funds, which should already be filled in once your link to your bank or brokerage is completed.

- If you select a single purchase, you can select the date for the purchase to be completed. I recommend setting a date near the end of the month, but on a weekday. For example, for this month, I’d probably select May 27, a Thursday. (An I Bond purchased late in a month earns a full’s month’s interest.)

- Submit.

At this point you should see a confirmation of your purchase, but since I’ve already purchased my 2021 allocation, I can’t complete the process to test it.

How do I track/sell my holdings?

TreasuryDirect isn’t really like a brokerage account where you can check the current value of your holdings on a simple “balances” page. When you go to the account summaries page, you will see a value listed, but it is actually the original value of the I Bonds you purchased. If you click on “Savings Bonds” on that list, you go to another page, where you can select “Series I Savings Bonds” and hit submit.

On the next page — titled “Current Holdings > Summary” — you can see a list of your holdings and the “issue date,” “interest rate” and “current value,” which reflects interest paid up to that point. If you click on an individual issue and “select,” you will see at the bottom a link to redeem that savings bond.

When you redeem, you can sell the full amount (including interest accrued), or a partial amount, and you designate the bank account that will receive the funds. TreasuryDirect says you should receive the money in two business days.

(Keep in mind that you must hold an I Bond for 12 months before redeeming, and if you redeem before 5 years you will forfeit the last three months of interest.)

The Treasury also provides a web-based Savings Bond Calculator that it says are for paper bonds only, but in actuality can be used to track and list the electronic version, too. Back in January 2018 I wrote a step-by-step guide to using this calculator. Hint: It’s clunky.

How secure is TreasuryDirect?

This is source of rather heated debates on the Bogleheads forums, because the Treasury makes no “stated” commitment to guarantee your account against hacking or theft. For that reason, some investors will not purchase any holdings in TreasuryDirect. And this debate has been going on for more than a decade.

While the Treasury seems to dodge the “security guarantee” question, I feel strongly that it would take responsibility for any errors/hacking that it caused. But if you fall for a clever phishing attack or have an evil relative, you could face losses. The system does send you email alerts for any account changes, such as in registrations or linked bank accounts, or even if the email address was changed.

The Treasury expects you to monitor your account and provide timely notice of any irregularities. I think the risk is extremely small, and I have not heard of anyone ever losing money through hacking or theft. The complex login system that TreasuryDirect uses, including the two-factor verification and virtual keyboard, add up to strong security.

As an added security feature, TreasuryDirect allows you to place a hold on your account. If you believe someone else has learned your account access information and you want to prevent unauthorized access, you can edit your Account Info in your primary account to place a Customer Hold. This action will prohibit all transactions associated with your primary and linked accounts. After you place your Customer Hold, you will not have access to your account until the hold is removed.

What happens at tax time?

Not much. TreasuryDirect doesn’t have a “user-friendly” attitude when it comes to tax documents. It may (or may not) send you an email reminder to log in and check your current documents. It will not physically mail you anything. When you locate your tax documents, you’ll find the format to be confusing and not-printer friendly.

Of course, with I Bonds, you won’t owe any federal taxes until you redeem a bond, and I Bond interest is exempt from state income taxes. So this isn’t a big deal for an I Bond investor. But if you redeem some bonds, you will have a tax obligation that year and you’ll need to track down the forms.

Conclusion

No one is going to extol TreasuryDirect for being “user friendly,” and some of the complexities arise because of the extra security steps it places in the way of logins. Can you open an account in 5 minutes? I’d bet against that. And there could be some time needed to verify your bank account before you can make a purchase.

If you have more questions, post them below. I might not be able to answer some of the more complex or legal issues, but possibly other readers have some experience in those areas.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It definitely caused at least a small reduction in six-month inflation. What's amazing is if the United States didn't attack…