By David Enna, Tipswatch.com

I’ve been watching with fascination as market real yields of Treasury Inflation-Protected Securities have been steadily rising in recent weeks. We can look at several apparent causes:

- U.S. inflation has perked higher since the beginning of the year, with the annual rate of all-items CPI rising from 3.1% in January to 3.5% in March.

- The U.S. economy is showing few signs of stalling, with the job and housing markets remaining robust. The unemployment rate stands at 3.8%, still close to a 10-year low.

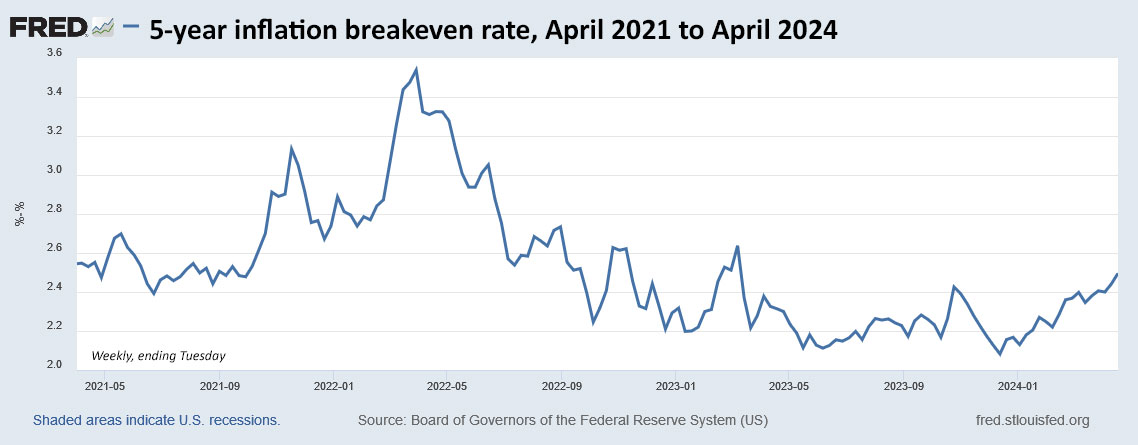

- The bond market’s inflation expectations have been steadily increasing, with the 10-year inflation breakeven rate rising from 2.21% on Jan. 2 to 2.42% on April 24.

- The Federal Reserve has backed off dovish talk and is now preaching a “higher for longer” message for U.S. short-term interest rates.

- The U.S. Treasury’s funding needs continue to rise with ever-growing federal deficits, causing longer-term yields to remain elevated.

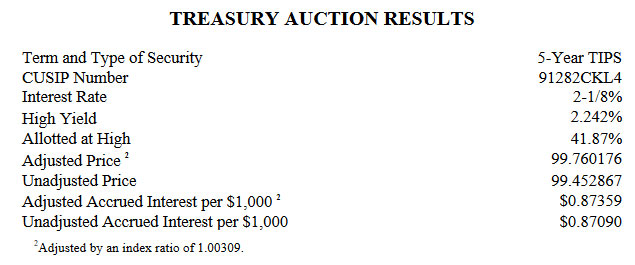

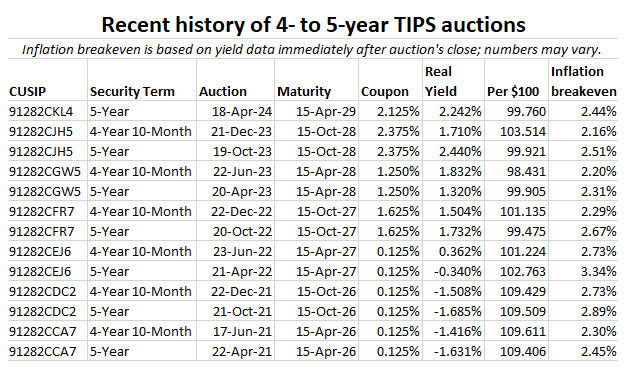

Definition: The real yield to maturity of a TIPS is its above-inflation annual return over the life of the investment. For example, on April 18 the Treasury auctioned a new 5-year TIPS with a real yield of 2.242%, which means that TIPS will out-perform official U.S. inflation by 2.242% over the 5-year term.

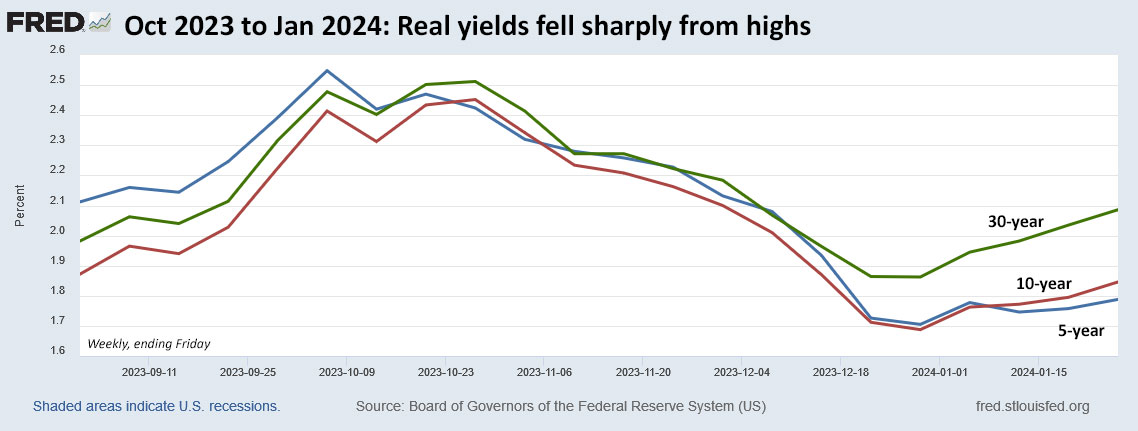

Here is the trend in 5-, 10- and 30-year real yields since July 2023:

As you can see, real yields peaked in October 2023 at a higher level than today’s market. The real yield curve at the time was essentially flat, with the entire maturity spectrum yielding in a range from 2.47% to 2.58%. That trend continued for about a month, before real yields began falling, fairly dramatically.

What’s interesting is that the September 2023 annual inflation rate (which was announced Oct. 12, 2023) came in at 3.7%, not much higher than today’s 3.5%.

Also at the time, the Federal Reserve was pushing the idea that short-term interest rates might not need to go any higher. And in fact, the Fed has held its federal funds rate in the range of 5.25% to 5.50% since July 2023. No cuts, no increases.

It was the Fed’s “no higher” message that helped cause interest rates to begin a steady decline into January 2024. In addition, the U.S. entered a mildly disinflationary trend through the end of 2023. As a result, real yields fell sharply through the end of the year:

But now, inflation is seemingly again a rising threat, and the Fed is hinting that it might need to increase interest rates if the trend continues. I think an increase is unlikely, but once-likely rate cuts might be out of the picture for the rest of 2024. Stock investors seem to be taking that news with a yawn, but the bond market is in turmoil, with the total bond market producing a total return of -3.0% year to date.

Here are how real yields stand today compared with their highs of October 2023:

As you can see, the 2023 yields were about 30 basis points higher than today’s elevated levels. October 2023 was a great month for building a ladder of TIPS investments, with all maturities yielding close to 2.5% above inflation. April 2024, in fact, is also an opportune time for making new TIPS investments.

But as this chart shows, real yields could go higher. Or, as happened in the months after October 2023, they could move sharply lower. A lot will depend on inflation trends and what actions the Fed decides to take through the end of the year … an election year.

What this means

I am always looking for a “new investing era” and I am certain we are well into an era of normalized interest rates, after a decade-plus of Federal Reserve actions to hold rates at ultra-low levels.

By historical standards, a 10-year Treasury note with a nominal yield of 4.67% and a 10-year TIPS with a real yield of 2.24% aren’t outliers. These were fairly normal in the past. In fact, the 10-year Treasury note had a nominal yield above 5% for nearly three decades from 1970 to 2000, as shown in this chart:

So are interest rates peaking in April 2024? My guess is: Probably. But it will depend on actions and direction from the Federal Reserve, which right now seems fairly happy with higher yields keeping the U.S. economy (and potentially inflation) under control.

Any change for I Bonds?

The Treasury will be resetting the fixed rate of the U.S. Series I Bond on Wednesday, May 1. The current fixed rate is 1.3%. That rate, which was the highest in 16 years, was set on Nov. 1, 2023, just after the October surge in real yields. The same thing is happening now, with a surge in April 2024.

My guess is that the Treasury will hold the I Bond’s fixed rate at 1.3%, and when combined with a new variable rate of 2.96%, I Bonds issued from May to October will be getting a composite rate of 4.27%, down from the current 5.27%.

Could the fixed rate rise, maybe to 1.4%? It could, if the Treasury attempts to factor in higher future real yields. Seems iffy to me.

The I Bond rate announcement could be coming on the morning of Tuesday, April 30, or more likely on the morning of Wednesday, May 1. TreasuryDirect has this message posted on a link from its homepage:

The current rate of 5.27 percent is available until 11:59 p.m. Eastern Time on Tuesday, April 30. The new rate becomes available at midnight.

That would seem to indicate TreasuryDirect will still be accepting orders for April I Bonds on Tuesday. But I would not risk that. If you are buying and want the higher April rate, buy Monday at the latest.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

In his first term, Trump constantly battled the Federal Reserve over interest rates, which he wanted lower. That would likely…