Amid months of turmoil in the bond market, and a lot of scary talk about bonds from investment advisers, yields on Treasury Inflation-Protected Securities have actually declined slightly over the last three months.

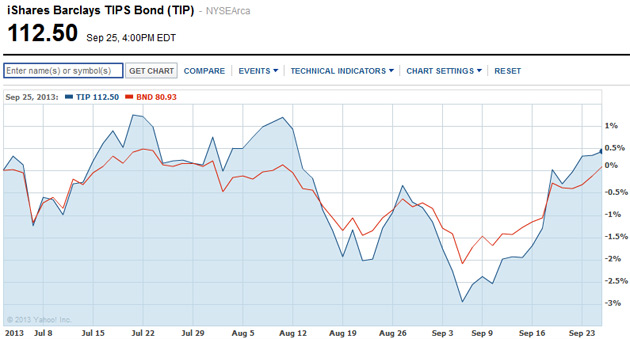

Hard to believe, isn’t it? Take a look at the chart for the TIP ETF, in blue, versus Vanguard’s BND ETF (total bond market) since July 1:

After a lot of volatility in the bond market, the price of the TIP ETF has actually increased almost 0.5% since July 1, outperforming the overall bond market. This means TIPS yields have declined over that time.

Here is a summary of how TIPS and Treasurys stand now, versus a year ago:

- 5-year TIPS: Today’s yield is about -0.38%, 44 basis points down from the early-September peak but a whopping 109 basis points higher than a year ago. Today’s inflation breakeven rate of 1.79% is much more attractive than 2.10% a year ago. It’s obvious the bond market is not anticipating near-term inflation.

- 10-year TIPS: Today’s yield is 0.45%, down 47 basis points from the peak but up 99 basis points from a year ago. The inflation breakeven point is 2.18%, down substantially from last year’s 2.42%

- 30-year TIPS: Today’s yield is 1.36%, down 28 basis points from the peak and up 90 basis points from a year ago. The breakeven point is down slightly from a year ago at 2.29%.

What these numbers mean. TIPS yields have declined sharply since the Sept. 18 Federal Reserve decision to back off from tapering its $1 trillion a year bond-buying stimulus program. The early-September peak in yields appeared to be pricing in tapering, and then the bond market was also hit by a weak jobs report (Sept. 13) and a very mild inflation report (Sept. 17).

Nevertheless, TIPS are a much more attractive investment today than they were a year ago, with yields across all maturities up about 100 basis points. At the same time, TIPS have gotten less expensive versus traditional Treasurys, shown by the lower inflation breakeven rates.

Are TIPS a screaming buy today? No. Are they a horrible investment today? No.

I personally believe Fed tapering is inevitable, and TIPS yields will again rise to more normal levels, in the range of 1% to 2% above inflation. We got very close to 1% above inflation in early September on the 10-year, before the Fed blinked.

A serious government shutdown, while unlikely, would change this equation. Read my April 25 blog: The TIPS earthquake: When did it happen, and why? It documents how the threat of a government shutdown in July 2011, plus a downgrade of US government debt, set off a massive reaction in the TIPS markets, with TIPS yields plummeting into negative territory for the first time in history.

A government shutdown would be ‘good’ for TIPS prices. Let’s hope that doesn’t happen.

>> I figured “What’s the hurry? Just buy these things in a slow and measured manner over time.”<<

Jimbo, I think that is a wise approach, especially if you are buying and holding to maturity. If you are buying 6- to 10-year TIPS, that should not be a problem. If you are planning on trading them for a profit, I have no opinion, that's a gamble. But holding to maturity means you get exactly the return you expected, x.xx% above inflation.

We had two years when TIPS were extremely undesirable as new purchases in this buy-and-hold approach. Now we are seeing the light, being tempted. Things are better certainly. They could get a lot better, as you note, with yields rising to the 'normal' 2% above inflation. A lot of things have to happen first, though, and that means a 150 basis point hit for the overall bond market. That would be ugly. It will happen, eventually.

It’s been quite an educational experience watching the TIPS market over the last few months. At first, I was overjoyed that I could finally purchase TIPS in the 6 to 10 year range with a positive yield to maturity. My original goal was to simply protect some retirement money from inflation that I had sitting in a cash account earning practically nothing. Not a large sum, but it was something that I felt comfortable with using as my initial foray into TIPS.

Once I burned-thru this cash, became a little more selective in my approach. I restricted my purchases to bonds available on the market that could be purchased below par. Finally, I established a rule to only purchase a particular issue if the new yield was higher than the last

purchase that I had made. Since Bernanke had basically said that the coolaid party was going to draw slowly to a close, I figured “What’s the hurry? Just buy these things in a slow and measured manner over time.”

The big reason that I started cooling my jets was the fear of the interest rate risk that I was assuming by purchasing 6 to 10 year TIPS at yields that were still below 1%. After all, the average coupon on 10 year TIPS since the beginning of time is around 2%. If you exclude the whacko data from 2010 and 2011, it’s more like 2.5%. That’s an opportunity cost of around 2% per annum on what are essentially mid-term bonds. Originally, I was just concerned with inflation – now I’m worried about future coupons.

Another way of looking at the coupons is what actually happened this year. In January, the coupon on the 10 year new issue was .125%. In July, it had risen to .375%. That’s a .250% increase over six months. At this pace, it would take 4 years to get the coupon rate back to 2.375%. During the same period, the yield on the January issue went from -.630% at the auction to +.415 on the secondary market on July 24th. That’s a spread of 1.045% in six months. If that kept-up, a 2.5% yield would take two years.

Of course, now that the Fed has seen the market reaction to possible tapering, they’ve pulled the plug on actually doing it. The 30 year mortgage rate went up 1% during the taper caper. That alone probably freaked them out pretty bad. I’ve learned a lot watching this circus.

That includes the clowns in the Congress who didn’t learn a thing from what they did back in 2011. Wasn’t it Einstein that said that the definition of insanity was doing the same thing over and over again and expecting a different result?