By David Enna, Tipswatch.com

Many of us here are strongly committed to holding investments in Treasury Inflation-Protected Securities to maturity. That means trading is not an issue, despite the temptations. It also means the “current market value” of a TIPS becomes a bit irrelevant.

So this opens a topic for debate: Which TIPS value should you follow more closely — current adjusted principal or current market value? This is a dilemma I wrote about last year in this post: The unique serenity of holding TIPS at TreasuryDirect.

A reader brought this back to my mind last week with this question:

I have a challenging time putting a proper “current value” on my TIPS ladder holdings. … I hold all my bonds to maturity. There-in lies the problem, when I go to make my semi-annual spreadsheet. Fidelity shows a value that marks-to-market daily each holding. Since I’m a “hold to maturity” only investor, that valuation doesn’t represent the value to me of that holding.

I think a proper “hold to maturity” current valuation to me is the current inflation adjusted principal. Is this a good “current value” accounting for a “hold to maturity” investor?

That sums it up perfectly. TreasuryDirect shows only one valuation for TIPS: par value x inflation index as of the last coupon payment. This provides an update on the growing amount you will receive when the TIPS matures. It is a legitimate view of value. Key point: TreasuryDirect does not allow tax-deferred accounts and you can’t sell your TIPS on that platform.

Your brokerage account shows market value, which rises and falls with changes in real yields, along with daily inflation accruals. This is also a legitimate view of value, and is crucial for determining RMDs if you are holding TIPS in a tax-deferred account. Also, since you can sell a TIPS at a brokerage, market value shows the potential value for a sale.

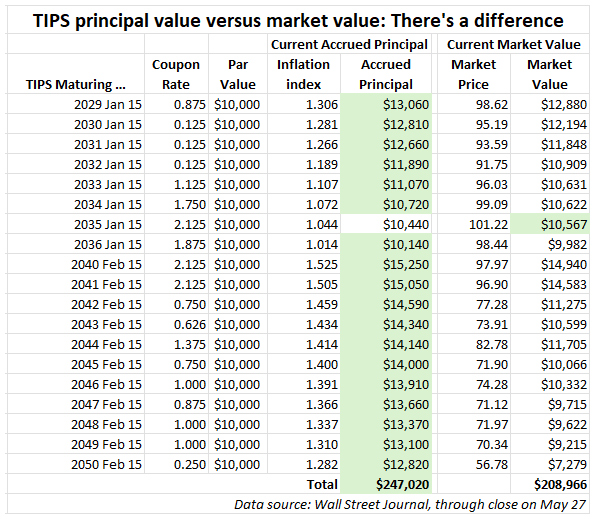

At this point, because longer-term TIPS real yields are at 15-year highs, market values for most TIPS are well below accrued principal. The difference is rather stunning for a multi-year ladder of TIPS, as shown in this example:

Keep in mind that as a TIPS nears maturity, market value becomes less and less relevant. It disappears at maturity and the final pay-out is: par value x inflation index, plus one last coupon payment.

The chart shows a simple way to calculate current principal using Excel. You just need to know par value and the current inflation index, which gets updated daily on this Wall Street Journal page, outside the paywall.

The chart also demonstrates why June 2026 is an excellent time to build a long-term ladder of TIPS. You can grab a lot of accrued principal at a discounted price. The negatives are: 1) the principal above par is not protected against deflation (a minor risk) and 2) the cash flow from coupon income won’t be stellar.

At Tipsladder.com, you can run through ladder scenarios. Right now, according to the site, you can build a 30-year ladder with a composite real yield of 2.50% and a safe withdrawal rate of 4.7%.

I Bonds? Not an issue

Series I Savings Bonds can never go down in value and cannot be traded on the secondary market. There is no “market value.” They have only one value to track: current adjusted principal, which changes on the first day of each month. TreasuryDirect will show you that current value, which you can also see using the Savings Bond Calculator or data from EyeBonds.info.

Correct answer?

As much as I would like to, I can’t ignore market value because most of my TIPS holdings are in a tax-deferred account subject to RMDs, which are based on market value at the end of the year. Also, your brokerage has to track market value because it changes daily, and some investors want to trade out of TIPS.

I am fine with seeing market value in the brokerage account. But I also keep an Excel spreadsheet showing the accrued principal for each TIPS, and I use that amount to balance out the years in my TIPS ladder. (I update the spreadsheet a few times a year.) The accrued principal will continue adjusting for inflation until maturity, so it does represent future inflation-adjusted cash flow.

Using the Excel method creates the illusion of a zero-duration bond with no interest-rate risk, similar to tracking an I Bond. Many Bogleheads freak out when I suggest this and yes, they are right. There is interest rate risk (or potential gain) if you want to trade out of TIPS.

Since I am not going to sell a TIPS before maturity, this is the multiverse reality I prefer.

Just to be clear, I am not a big fan of the multiverse trend in movies, especially Marvel movies, where it is way overused. But here is a multiverse treat, the closing credits theme from Loki season 1, episode 5, by the fantastic composer Natalie Holt. (She wrote different closing themes for every episode. Talk about multiverse!) This is one of my favorites of all time:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Great article, thank you for continuing to educate the public on TIPS!

I use Quicken to track every dollar and I have tried various strategies over the years on how to represent TIPS, especially since I have them in Schwab where transactions download straight into Quicken.

I agree using the market value is really odd for someone holding to maturity… who wants to see a logical market loss, or gain, on TIPS which is only hypothetical unless you are forced to sell?

Also, I didn’t want to show just the accrued principle, because you are showing the maturity-value of the bond, which could be 10-20 years out, and thus in Quicken it artificially inflates your overall assets as-of today. And the only “growth” you would see in Quicken is the inflation growth, plus you are missing the value of the interest payments.

I also want to show a price for every day in Quicken, so it charts properly over time.

The balanced approach and model I landed on is:

Sounds complex, but this is a one-time setup in a Google sheet. Then once a month, the Sheet auto-loads the current CPI data and I have one tab that I download as a CSV. The CSV contains all the Quicken TIPS prices, where every CUSIP has a price value for each day of the next month. Then I import this CSV into Quicken. Whola! Takes me <5 minutes a month.

Using this model lets me show real growth within Quicken each time I load the next month’s CUSIP data, extreme mental happiness! The growth is my real YTM plus the inflation growth. Best of both worlds.

I am happy to share the Google Sheet if others are interested.

Robert

I do all my financial tracking in QuickBooks and every month I make journal entries for all my stocks/bonds/etc. at the market rate to match my brokerage account statements. I started out valuing my TIPS at the inflation-adjusted amount, but after a while, I didn’t like that system at all. Since my totals didn’t match my brokerage statements, it was extra work to make sure the difference wasn’t a mistake I’d made in a journal entry. Since I track stocks/ETFs by market value, I decided to track my TIPS that way too. I show my stocks going up and down, but none of that matters until I sell. I decided to think of TIPS the same way. I plan to hold to maturity, but I book the market price so everything matches my statements.

For bonds bought in secondary market – what is the amount in cost basis on vanguard site? It certainly is not what I exactly paid when I bought the lot. Is it what I paid * the factor at the time?

The cost basis *should* be the investment cost, which would be (par value x inflation factor) x price.

In other words, it is not the par value you purchased, for example if you placed an order for $10,000 par value of the 10-year TIPS auctioned May 21. In that case the cost basis would be $9,893.85.

($10,000 x 1.01522) x 0.97455252 = $9,893.85

When you place an order at Vanguard, before you click submit you should see the investment cost listed. That should be the original cost basis. However, as inflation accruals are added as additional shares, the cost basis will rise since that is taxable.

I have never purchased a TIPS in a taxable brokerage account, so I have no experience in what you will actually see.

Should people buy TIPS if they have a general understanding of how they appreciate in value, i.e. through inflation, but have difficulty calculating the value at any particular point in time including at maturity? In other words, if there is a period of inflation the investor might understand that the security will grow based on that inflation, but will have to accept the valuation per the Treasury’s calculation.

Thanks for the explanation. That’s what I thought it should be (par value *factor * price). But I noticed it is much higher now (It’s been a couple of years since I bought the bond). The inflation accruals make sense.

For my tax situation I find I bonds a tax nuiscance (still own a few). Hence I waded into TIPS in taxable. And I couldn’t resist 5 year tip at 1.8% yesterday 🙂

Is there any interest in the SpaceX (SPCX) IPO?

You do realize that this is a website about inflation-indexed bonds?

Just by coincidence, I have been listening to an audio book titled, “Ludicrous,” about Elon Musk and the creation of Tesla. It documents the many faults of the company, including quality control, and Musk’s frequent misleading statements, ethical missteps, hype, and even threats. Plus, of course, Musk’s drive for success and visionary drive.

The Savings Bond Calculator will calculate the value (principal plus accrued interest) for each month for all of your I-bonds for up to six months ahead. This means on May 1, you can know your I-bonds’ exact total value for each month up to November. It will also give you year-to-date interest which can be helpful for end of year tax planning, especially if you want to redeem an I-bond to avoid crossing an IRMAA threshold (IRMAA has the scourge of all tax structures, but that’s another story).

It is not a straightforward calculation because it depends on what month a bond was purchased along with its fixed rate and the new variable rate, so it is nice that the Savings Bond Calculator does this for you. This can be useful if you want to know exactly how much your I-bond is worth if you plan to redeem it on, say, Sept 1. Also you can calculate your estimated APY for all your bonds on May 1 for the next six months.

Random question: Have you ever looked into investing in inflation-adjusted government bonds of foreign governments? I’d be interested in reading about it.

I did look at the SPDR FTSE Intl Govt Inflation-Protected Bond ETF (WIP) a few years ago, but I shied away since I would rather own bonds in my own currency. I imagine WIP is going to get a lot of attention now because its total return over the last year was 11.5%, versus 4.9% for SCHP. But over the last 5 years, it was annualized at -0.39% and for 10 years, 1.84% Compare that to 1.21% and 2.80% for SCHP and 3.37% and 3.18% for VTIP.

RMDs are a reason to care about market prices in a traditional IRA, and there is a different tax-related reason to care in a taxable account: loss harvesting. If you find yourself having some unexpected (windfall) or unwanted (someone took over a corporation you held stock in) income to offset, you may be able to avoid taxes on it by harvesting a capital loss. It’s certainly possible and even likely these days as you point out to have some juicy paper losses in TIPS. Even if you still want the bonds, you can always sell one to take a loss and at the same time buy a different issue, perhaps one that matures 6 or 12 months away. Since bonds that differ in maturity date and/or coupon are not considered substantially identical securities unless convertible into one another, you can book the loss with little effect on your overall risk or income, and you can always reverse the trade 31 days later if you want, or in a year if you can benefit from the 0% rate on long-term gains or otherwise have a lower rate that year. Reducing tax liability without taking on additional risk is generally a good move, and if you hold TIPS in a taxable account they offer one of the lowest-risk ways to harvest a loss when you need one. Of course, straight Treasuries are also good candidates if you own them, for the same reasons. That’s not really all, though.

Personally I keep track of both these quantities. While I don’t generally expect to sell any of the bonds I own, it is always possible that the market will overvalue any particular asset to such an extent that I am no longer willing to own it. TIPS with substantially negative yields would be an example of that: gold’s yield of zero is preferable then, or I-bonds if you’re especially skittish and can get enough of them. Any Treasury security in 2020; remember that a few people managed to unload 30-year bonds yielding less than 1% at the very moment the Fed was creating a 30% jump in prices! And so on. I prefer to hold to maturity but failing to take advantage of an irrational market is devastating to long-term returns, especially if your investing years feature prolonged and severe financial repression which is true of most of Gen X and the later boomers also. When you’re getting 5%, holding to maturity is a strategy; when you’re getting 2%, it’s financial suicide. Buy cheap, yes. But sell dear too, when you can. One might ask how to be sure a TIPS yielding -2% is a bad investment. You have pointed out instances in which negative yielding bonds still outperformed straight Treasuries. True but irrelevant. A basement full of toilet paper outperformed Treasuries. Handily! In fact, a basement full of almost anything outperformed TIPS. The reality of it is that you are guaranteeing yourself a loss. You are better off buying whatever long-shelf-life items you expect to need in that future year and putting them aside to give you a 0% yield plus the phantom future price increases; think of it as a zero-coupon TIPS with nontaxable phantom gains. Ignoring the market is usually wise, but when people are lining up to give you free money, take it. To do that, you have to be aware.

Great thoughts, thanks. But still … I am holding onto TIPS to maturity. I Bonds? No, I will redeem those if I need the cash or want to avoid a future tax hit.

Great points! Thanks for taking the time to post that Fred. Plans should never be cast in stone and you did a great job explaining why.

Since you hold to maturity, you could also do a “value at maturity” calculation. You simply take today’s accrued value and then multiply that by your expected cumulative inflation from now until maturity.

Surprising things can happen.

For example, I bought a TIPS around a peak of yield to maturity in 2008. Because yields to maturity have been lower since then, meaning buyers paid a premium, the indexed value has consistently lagged market price. But at maturity, I expect that to turn around and for the value at maturity to exceed today’s market value, due to higher inflation over the next four years. Plus, I got a decent interest payment on the inflation-adjusted basis twice a year for the last 18 years.

David,

Though I don’t hold TIPS the point about the RMD calculation is a good one and brings front and center the fact that the market value is what it is and cannot be completely dismissed. We cannot predict the future and those that say “they will never sell,” are probably too young to realize that your “never” could actually end tomorrow and someone else will be stuck with your “market value,” or your finances could end up in such a position that the TIPS are the lessor of two evils in what you need to sell to generate the necessary cash to address an unforeseen circumstance.

Only because I enjoy it, my spreadsheet has everything – so I always have an estimate of what the next coupons/maturing TIPS dollar amount will be. But that’s mainly because I just enjoy doing it more than anything else.

Regarding RMDs, my plan is to Roth convert out all of my stock before RMDs begin at age 75. My own calculations show that it would require an unprecedented drop in yields for the RMD-based withdrawal calculation to exceed what the ladder will throw off on its own. And even if, somehow, that happened, it would likely be temporary since the effective percentage withdrawal from a TIPS ladder rises much faster over time than the effective percentage withdrawal from the RMD tables.

I do know that a lot of investors are either unable or unwilling to switch their mindset from holding an allocation of risky assets where returns and volatility are the primary focus to one where income is the focus. But once you make that transition, for all but some corner cases, you can safely ignore the value of your TIPS holdings.

I don’t know why anyone would build a TIPS ladder in Treasury Direct. You cannot sell them, transferring them can take a long time, and they don’t report market values. Brokerage accounts are not difficult to open and major brokerages charge no commissions and you can submit orders for auctions too.

Market value is always relevant. You may not act upon it, but you need to know it periodically as Hulu posted. Market value represents your ability to change course, for whatever reason. You can’t change course based on a value that cannot be realized.

Yes, you can buy principal at below 100%, which simply means those bonds were not a good buy at issuance given what has transpired since. Whether they are a good buy now depends upon the future!

I get that the intent of a TIPS ladder is to have inflation protection for an extended period and most people intend to hold them until maturity. But people die prematurely, heirs don’t have the same goals, etc etc.

Further, money is fungible! People commonly say how they setup a ladder to have maturities to provide cash for spending in the year of maturity. Unless you have no other assets, that is more a mental accommodation than reality. I have a ladder, intended to provide inflation protection for a spending amount – not to provide the actual cash for spending, which can come from other sources, or from the TIPS as I best judge at the time.

I bought TIPS at TreasuryDirect for nearly 15+ years (while working) and still have issues there maturing in 2027 to 2029 + 2041. While I much prefer the ease of buying TIPS in a tax-deferred brokerage account (at auction or otherwise), I also appreciate these taxable TIPS maturing in the next few years with near-zero taxes due. Building a true ladder at TreasuryDirect is nearly impossible because the investor only has access to 5- 10- and 30-year auctions.

Hey, we have all done things and then learned from them or might do them differently next time! If someone wanted taxable TIPS, they could still do that in a taxable brokerage account. I presume they would provide you with the tax reporting each year making it simple.

A ten year ladder would not be hard in Treasury Direct. You could build it in 5 years, buying the 5 and 10 each year. Then roll the maturity into a new 10. But everybody is in a rush to build the ladder in a short period.

I am biased against long bonds. Rolling a ten year ladder provides the same inflation protection as having a longer ladder. A lower real yield, but also less volatility and lower risk should you need to sell. If you invested poorly, reinvestment into new bonds is quicker. If you invested wisely, the good returns run off quicker. It is always a tradeoff.

In my spreadsheet, I have one cell with the current “REF CPI” for the current date, which is the same for all TIPS. Each TIPS CUSIP I own has its own row, with the quantity and the “REF CPI on Dated Date” for that CUSIP. That way, whenever I want to know the current value of all my TIPS, I only need to update the current REF CPI cell; I don’t need to change all of the rows for all of my TIPS.

For example, CUSIP 912828Z37 (maturing 1/15/30) shows the REF CPI as 329.66010 for May 27 and 257.28368 for the Dated Date:

https://www.treasurydirect.gov/auctions/announcements-data-results/tips-cpi-data/tips-cpi-detail/?cusip=912828Z37

If the current REF CPI is in cell A1, the row for this TIPS would have a “price” cell that looks like this: A$1/257.28368*1000, which shows the “price” as $1,281. A quantity of 10 would have a current value of $12,810 (which is the same number as in David’s table).

For a more extreme multiverse consider a whole life insurance policy where you can evaluate (I) the death benefit, (ii) the cash surrender (or loan) value, and (III) what Coventry Direct would pay for it.

Another option would be the Present Value today of all future coupons and the final payment? You would need to project future inflationary growth and discount back at an appropriate discount rate. This is what I do for determining my Net Worth.

Market Value is meaningless if you will 100% hold to maturity. Valuing as the future payment at maturity doesn’t take into account the future coupons or the time value of money.

If you are just looking at projected cash flows that’s a different animal than the Value of the TIPS.

This is something I deal with as well. When I do my semi-regular updates of my spreadsheet, I have one column with the market value of each TIPs and another with the value based on each bonds inflation index, assuming it is held to maturity. If I could figure out how to export the info from WSJ (I believe that’s outlined on the Bogleheads forum), it would be much easier.

You can explain these issues better than 99% of financial writers. I particularly like you pointing out the silver lining that now might not be a bad time to fill in any ladder gaps from the secondary market.

“You can grab a lot of accrued principal at a discounted price.”

At first, that sounded almost as if the accrued principal were cash sitting in a box that can be purchased below face value. But of course not, or every hedge fund would buy it quickly. So I figure that what it really means is: “You can buy claims on large inflation-adjusted principal balances when the bond matures at market prices that are below those balances.”

Your translation is perfectly fine. Except maybe the order of wording: When a TIPS matures it is at full accrued principal value, not market value. I know you understand that.

True enough, although “every hedge fund” having an interest in TIPS is a bit of an overstatement. They’ll be ~$28 trillion of gross Treasury issuance this year and <$200 billion of TIPS issuance. So interest in this type of security is small in scheme of things.

Said another way, my experience with TIPS is that it’s fairly easy for individual investors to time ladder purchases to achieve higher than average yield to maturity. I have a full 10-year ladder, all with yield to maturity >= 2%. I just don’t buy if it’s less than that.

I think the observation in the blog is just saying now is a time where individual investors can get that type of return above inflation pretty easily in today’s secondary market.

I must have started buying TIPS long before you, as close to a decade went by from the GFC when there were few (if any) TIPS with a real yield above 2%. I wasn’t thrilled to be buying at <2%, but they achieved what I wished to achieve in terms of my ladder. I agree that 2% makes this a great time to start a TIPS ladder! I’d be happy with 2% even if they should go even higher– it’s good enough for me.

Not marking to market is pure mental accounting. That’s how investors get into trouble.

At TreasuryDirect, you will never see “market value,” so you’d have to calculate it yourself. I suppose that could come into play if you were preparing a net-worth statement? One important thing, however: If you are building a ladder of TIPS investments over 20 to 30 years and you want equal amounts of inflation-protected cash maturing each year, you should balance the amounts of accrued principal, not the market values. The accrued principal will be the future pay-out, adjusted for inflation.

I’ve never sold a TIPS, an IBond or a CD before maturity . . . and I never will. So “marking to market” is totally the wrong accounting for me for knowing where I currently stand vs. my financial goals. And I will never get in trouble by not doing it.

I don’t worry about the current marketable value of my individual TIP bonds since they will be held to maturity and the returns are guaranteed.

But if I had a bond fund I believe I wouldn’t like watching my invested principle be up or down so much since there is no maturity date. Those bond funds seem to me more like a variable rate savings account like a MMF or something akin.

You don’t have to “worry about” it. You do have to be aware of it to consider ones self to be a rational investor.

I continue to learn. Thanks for the insight!

The other multiverse is that the dollar will always be king. Some cracks are starting to show IMHO. I gonna hold stable coin in diversified currency backing when this gets going big next year.