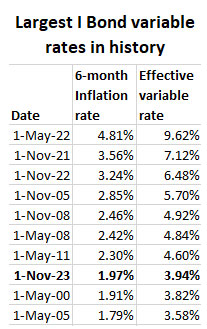

I Bond’s new composite rate could exceed 5% at the November reset.

By David Enna, Tipswatch.com

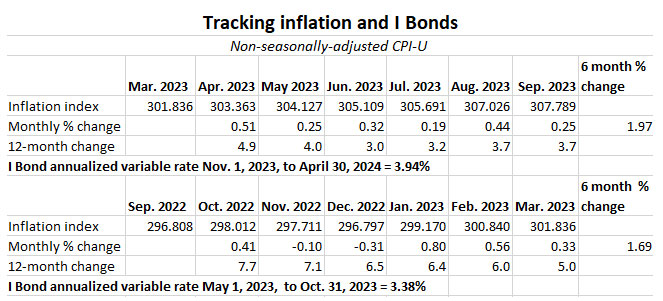

Investors in U.S. Series I Savings Bonds will see the investment’s annualized inflation-adjusted variable rate rise to 3.94% at the November 1 reset, up from the current rate of 3.38%, based on September inflation data released Thursday by the Bureau of Labor Statistics.

That variable rate, which is updated every six months, is applied to all I Bonds, no matter when they were purchased. The starting month of the change depends on the original month of purchase. The variable rate is combined with a permanent fixed rate to determine each I Bond’s composite interest rate.

At the November reset, the I Bond’s fixed rate should rise above the current 0.9%, if market conditions stay stable through the end of this month. That means the new composite rate — for I Bonds purchased from November 2023 to April 2024 — should be higher than 5%, maybe as high as 5.4%.

But investors holding I Bonds with a 0.0% fixed rate will be getting an annualized return of 3.94% for six months.

The new variable rate was set by non-seasonally adjusted CPI-U from April to September 2023. The BLS set the September inflation index at 307.789, an increase of 0.25% over the August number. Here are the data:

A variable rate of 3.94% sets up a quandary for investors holding I Bonds with a fixed rate of 0.0% — and there were a lot of those issued over the last decade. In effect, 3.94% will be their new composite rate — more than 100 basis points lower than investments in federal money market funds or short-term T-bills.

Redeem or keep holding? My opinion: Hold if you want the inflation protection. But if this is a short-term investment, redemption probably makes sense.

We don’t know what the new fixed rate will be for the I Bond at the November 1 reset. I have theorized that it could be the range of 1.4% to 1.7% (but this week’s real yield trends may indicate it will be lower). Any I Bond with a fixed rate above 1.0% will be attractive, in my opinion.

I will be writing more about this in coming days. But a quick thought: If the new I Bond fixed rate is 1.2% or higher at the reset, would I be a buyer in 2024? Absolutely, yes.

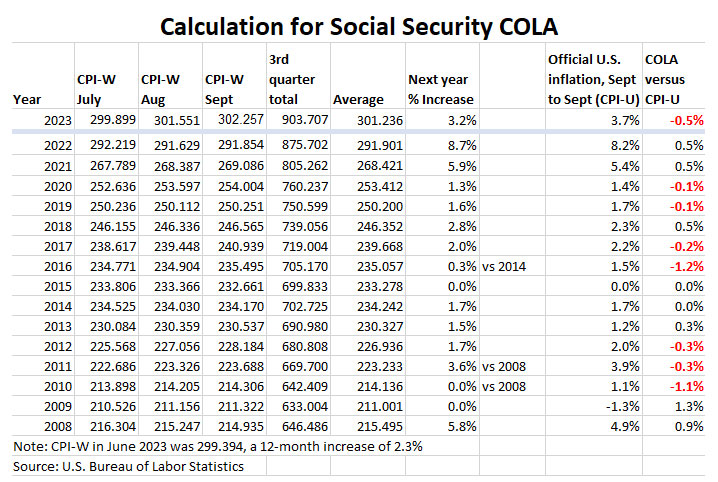

Social Security COLA

The September inflation report was the third of three — for July to September — that set the Social Security Administration’s cost of living adjustment for payments in 2024. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

For September, the BLS set CPI-W at 302.257, which produced a three-month average of 301.236, an increase of 3.2% over the same average for 2022. That means the Social Security COLA will be 3.2% for payments beginning in January. The numbers:

Note that the 2024 COLA of 3.2% trails the official U.S. inflation number of 3.7% for the September-to-September period. That is often the case, because the SSA’s formula using a three-month average tends to smooth out sharp increases in inflation. Also, CPI-W tends to run lower than CPI-U. But the increases for 2022 and 2023 payments actually outstripped official U.S. inflation.

Starting in January, the average monthly Social Security retirement benefit will rise by $59, from approximately $1,848 to $1,907, according to the SSA.

What this means for TIPS

Principal balances for Treasury Inflation-Protected Securities are adjusted each month based on non-seasonally adjusted inflation two months earlier. The September inflation index of 307.789 means that TIPS balances will rise 0.25% in November, after rising 0.44% in October. Here are new November inflation indexes for all TIPS.

September inflation

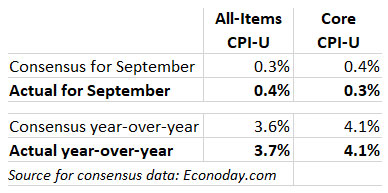

All-items U.S. inflation rose 0.4% in September and 3.7% year over year. Both of those numbers exceeded expectations. Core inflation, which omits food and energy, rose 0.3% for the month (less than the expected 0.4%) and 4.1% year over year (matching expectations).

So, nothing too surprising. The BLS noted that costs of shelter (up 0.6% for the month and 7.2% year over year) were a major factor in both all-items and core inflation. Gasoline prices were up 2.1% in September after rising 10.6% in August. Food at home costs rose a moderate 0.1% and are up only 2.4% over the year. Apparel costs were down 0.8% for the month.

Excluding housing and energy, services prices climbed 0.6% from August, the most in a year, according to Bloomberg calculations.

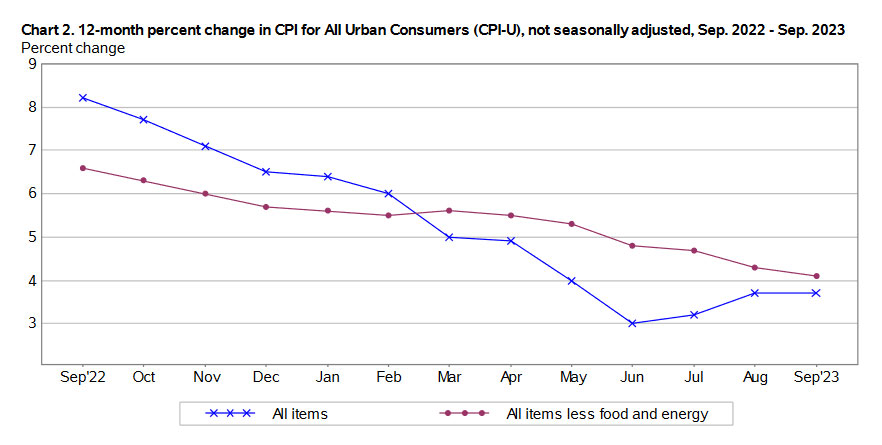

Here is the 12-month trend for all-items and core inflation, showing that all-items inflation has started climbing higher since June with increases in energy costs:

What this means for future interest rates

The Federal Reserve has been on a publicity campaign over the last 10 days to sell the idea that short-term interest rates “possibly” won’t need to go higher. Why? Because mid- and longer-term Treasury yields have been surging higher, causing the stock market to sell off. The bond market has been doing the Fed’s work.

But that interest-rate trend reversed a bit this week with turmoil in the Mideast and a flight to safety in U.S. Treasurys. Real yields have declined about 20 basis points this week. Still, I think the Fed will stick to the narrative that short-term rates have peaked but will remain elevated well into 2024.

Inflation is nowhere near the Fed’s target of 2.0%, with core inflation currently running at 4.1%. We’ve got a long way to go. From this morning’s Bloomberg report:

“While inflation is slowly edging lower, the strong labor market means that the threat of inflation resurgence cannot be ignored, keeping the Fed on its toes,” said Seema Shah, chief global strategist at Principal Asset Management. “The question around whether or not there will be one more interest rate hike is yet to be answered.” …

Anna Wong of Bloomberg Economics: “The September CPI report won’t convince most Fed officials that interest rates are sufficiently restrictive… Our baseline is for the Fed to hold rates steady for the rest of the year, but we see non-negligible risks of another rate hike, something the market is probably under-pricing.”

In other words, we face more uncertainty. And it is times like this that make investments with inflation protection highly desirable.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————-

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: October inflation brings positive news: Flat for the month, sliding lower for the year | Treasury Inflation-Protected Securities

Pingback: Medicare costs for 2024 are rising faster than U.S. inflation | Treasury Inflation-Protected Securities

Since we know the variable rate on I-bonds for the next six months, is there any program around that will allow me to calculate my I-bond interest for each month for the next six months? I have a lot of I-bonds. It would provide the same information as Savings Bond Calculator. I could wait until Nov 1 or 2 to use the updated Savings Bond Calculator, but I would like the calculation now rather than have to wait a couple of weeks. Eyebonds.info does not seem to do it (it stops in Oct 2023).

The eyebonds.info site could provide that information, one I Bond at a time, but it hasn’t yet updated with the new variable rate. That probably won’t happen until the November announcement.

eyebonds.info DOES provide a method in the form of their downloadable IBond Portfolio Calculator Excel Workbook found on the download page. You just need to load up the information on your IBonds portfolio and plug in the values for your projection of the next variable and fixed rates. Note that the variable rate you put in is the 6-month rate rather than annualized.

Hello, David, thank you so much for all of the information and analysis you provide! You have greatly expanded my knowledge, and I really appreciate your consistent, rational approach.

I’m trying to decide how to use my I-bond purchase limit for 2024. Should I roll 0% fixed rate I-bonds into the new rate or hold them and purchase additional I-bonds? The answer seems to depend on what I would buy with the proceeds of those old bonds.

I think we have a lot of good alternatives right now for low-risk investments – treasuries, municipals, TIPS are all giving better after-tax returns than those old I-bonds. So I think that doing the roll is a good idea and I should be putting my new money someplace else, instead of effectively, “buying” I-Bonds with a 0% fixed rate. Am I missing something?

If you haven’t made your 2024 purchase yet, congratulations! If the November I Bond does get a fixed rate of 1.2% (or higher) waiting will have turned out to be wise. You can buy this year and again after January. Now, should you roll over the 0.0% I Bonds? I probably will do that next year, but I have large holdings in TIPS and I Bonds. I consider the I Bonds my tax-deferred, inflation-protected savings account. And I don’t plan on holding the I Bonds forever. I will be spending that money in future years. …. But your circumstances could be different, especially if you don’t have a large allocation in inflation-protected investments.

There is one thing that I BONDS are GREAT about vs. TIPS – and each have their own place in one’s investment plan……I BONDS principal does not fluctuate and redemption is much easier on the nerves in case of an emergency withdrawal – whereas TIPS, the principal is subject to interest rate risk, duration risk, etc. which won’t serve well in an emergency as the principal may take a hit especially in a rising rate environment we have now.

And since one can buy only a set amount of I Bonds in a given year, best to park it and forget about it just as one would for TIPS.

Reaching for yield, buy/selling etc. may be a good short term preoccupation for I Bonds and TIPS but is an unhealthy approach to fixed income investing for long term!

Excellent point of view. Thanks.

I have 0% I bonds that I purchased in 2022. Considering redeeming in January 2024. I realize I will lose 3 months interest. I assume the accumulated interest will be reportable as 2024 income. Or will the interest be reported at earned through October 2023 because of the penalty and reported as 2023 income?

Interesting question. I believe the tax will be owed in the year you receive the proceeds, so taxes will be owed in 2024.

Thanks David for your great blog! I found you after reading Harry Sit’s blog. For anyone selling your 0% fixed rate bonds, who may be worried about the tax owed and if an underpayment penalty might apply, Harry has some great step-by-step instructions on how to withhold taxes when you redeem your bonds. If you want to overpay your taxes, so you can buy more I Bonds with your refund, this is also a handy way to pay extra. Just thought I’d pass it along.

https://thefinancebuff.com/tax-withholding-sell-i-bonds.html

I am thinking of cashing out the 2021 & 2022 I-Bonds by paying 3-month penalties. Buy 6 month T-Bills. Then buy new I-Bonds in April via the giftbox options to be delivered in multiple years in future.

i bought an i bond in january 2023. i didn’t know there was a fixed rate. is the fixed rate added to the 3.38 percent rate? could you tell me what the fixed rate was in january 2023?

If you bought in Jan 2023, your fixed rate is 0.40%. Your current composite rate is 3.79%.

Did CPI-W actually outpace CPI-U during the 3Q SS COLA calc? When I look at the CPI-U chart for the I-Bond rate, it looks like July, Aug and Sept ran 3.2%, 3.7%, 3.7%. Is it too crude a calculation to average those together and get a CPI-U 3Q of 3.5%?

I’ll take your word for that (didn’t check it) but the thing to realize is that annual CPI-W as of June 2023 was up only 2.3%, versus 3.0% for CPI-U. So it needed to catch up for the lag.

That would make sense as a (more or less) equalizer.

We know that the next I Bond inflation rate will be 3.94%, which is .056% above the current one.

We think we know with some degree of certainty that the next I bond fixed rate will be above the current 0.9% one.

So there’s really no reason for anyone to buy the current I Bond. The I Bond section of Treasury Direct should be a ghost town for buying for the next 2 1/2 weeks (but may be busy for selling as it has been since the current 3.38% has been applied to existing I Bonds for 3 months or more).

And on April 12, 2024, we will know the NEXT I Bond inflation rate and know what interest rates have done during the next 6 months including T-Bill and T-Note alternatives. As it usually is, THAT seems to be the Goldilocks time to make the most informed decision about whether to buy the upcoming I bond offering.

As for right now, I’m a buyer of a 26-week T-Bill to prepare for that decision-point.

In the past, when cash was paying 0.001%, I often said, “When you’ve got the $10,000 sitting around, make the purchase.” But now you can do well with cash, so no need to rush. Your strategy looks good.

Well, if the fixed rate is 1% and the variable rate is 3.94%, then the combined rate is 4.94% tax deferred for thirty years for the I-bond, if the variable rate stays on average to be 3.94% (The average annual CPI from 1971 to 2022 is 4.01%, which is about what the variable rate is now). The current 6 month T-bill pays 5.58% but it is federally taxed on your next tax return. Say you are in the 20% tax bracket, that reduces the T-bill interest rate to 4.46% (after taxes, as they say). So much depends on what your tax bracket will be when you cash out your I-bond. Also if you assume the average annual CPI will be around 4% while you hold the I-bond, I-bonds do not look too bad. I have always viewed a 5% annual return over the long run to be pretty good for me, especially it it is tax-deferred.

A final consideration: Medicare will increase your monthly premiums fairly dramatically if you are a single person and earn over $97,000. I am pretty sure the tax-deferred income on I-bonds is not part of that calculation (until you cash out), but Mr Enna knows for sure and can correct me on this.

1) I’d prefer to look at the 30-year average inflation rate, which was 2.5% for the 30 years ending in September. But it could be higher over the next 30 years. Or not. 2) You are right that I Bond interest that is deferred has no effect on Medicare surplus charges until you actually redeem the I Bond, or it matures. (No I Bond has ever matured, as of yet. The first one will be in September 2028, I think.

1) Well, I like 50 years, but you like 30 years. Big difference in averages. But note the CPI in 2021 was 4.7%, in 2022 8.6%, and in the 12 months ending in Sept 2023 it was 3.7%, all of which are a lot closer to the 50 year average of 4.0% than the 30 year average of 2.5%. I seriously doubt we will see ZIRP again (which dominates the 30 year average) now that the Fed has seen how much trouble it has caused.

2)Thanks, that is becoming important now that I am getting 5.5% on Tbills. As for I-bonds maturing, I have a lot of I-bonds maturing in 2031. I am not looking forward to it.

Just another comment related to Eric‘s comment above. I am currently selling my i-bonds that are yielding below 4% and will roll them into new i bonds in November yielding over 5% with a higher fixed rate. You seem to recommend in your column that if the new rate is 3.94% that you should hold. It is hard for me to understand under what circumstances it would be better to hold, than to roll them to new ibonds With a higher fixed rate. Can you clarify?

The reason to hold is viewing I Bonds as a long-term, inflation-adjusted savings account. Do you think there could be a time in the future that the Fed again pushes real yields below zero and safe investments are again yielding close to 0.0%? If that happens, you want to be holding I Bonds, which will at least match inflation. That said, I will probably roll over 0.0% I Bonds next year to buy at the new rate.

I do view I-bonds as a long-term inflation protected savings account. However, if I simply sell my older Bonds that have a 0% guaranteed rate and replace them with new issue bonds at a higher rate then I am better off. The real problem is the $10,000 annual purchase limitation. So if I want to maintain the same amount of inflation protected investments, I will actually be forced to roll some of my Bond sales into Tips or something similar.

I keep hearing about rolling over I Bonds into new I Bonds. How does rolling over I Bonds to get better rates with new I Bonds work? I thought the limit was $10,000 per year with some exceptions such as the gift box. So if you have say $30,000 in 0% I bonds, and assume that none of the exceptions are available to you, how would you roll over the entire $30,000? To me roll over is a misnomer, you are just selling I Bonds and buying new ones up to the $10,000 limit.

You can only buy $10,000 per person in new I Bonds, so you redeem about $10,000 of I Bonds with 0.0% fixed rate. You will get some extra cash, but you will also owe taxes on the interest. The gift-box strategy is available if you want to do more, and I think that strategy is best used when the fixed rate is high, not when the temporary variable rate is high.

Thank you. Will you be writing about the 5 year TIPS auction coming up?

The preview article will be posted Sunday morning.

You should consider methods to purchase more than $10k such as spouse purchases and trust purchases.

Great idea. I already do have my account, my wife’s account and an LLC so that gets me to $30,000 per year I think that’s enough allocation to I-bonds, at least for me.

If I’m going to redeem a set of 0%-fixed I-Bonds to purchase new 1%+-fixed rate I-Bonds, should I redeem my oldest or newest 0% I-Bonds?

The answer might depend if you are OK with paying taxes on the higher earnings of the older I Bonds. Any I Bond older than 5 years can be redeemed without any penalty, so that is a plus (3 months interest). The newer I Bonds will face the penalty but the tax bill will be lower since they haven’t been earning interest as long.

Thank you David. This sort of information all in one place is unavailable elsewhere so far as I know. I am leaning towards ‘ sticky ‘ inflation myself and it seems the Fed is reluctant to continue being aggressive. Because of upcoming election?

I have been thinking for awhile that a short-term rate of around 5.5% should be adequate, if longer-term rates started rising. Now that has happened. But it is amazing to see the job market remain so strong.

Thanks for the analysis as always!

With HYSA close to 5% and maybe going higher with another predicted rate hike, I’ll be selling my I-Bonds with a <4% rate and 0% fixed rate. I’ll be buying back into the higher fixed rate. Only question is to do that in October (better variable rates) or wait until November (for the better fixed rate). Looking forward to your analysis on this!

November will have better fixed and variable rates

The fact that inflation went up YoY after being so high (ie 7-9+ percent), would you say this is the “sticky” inflation that was previously talked about? Above 2% is still bad, but it went back up to almost 4%. Wow.