By David Enna, Tipswatch.com

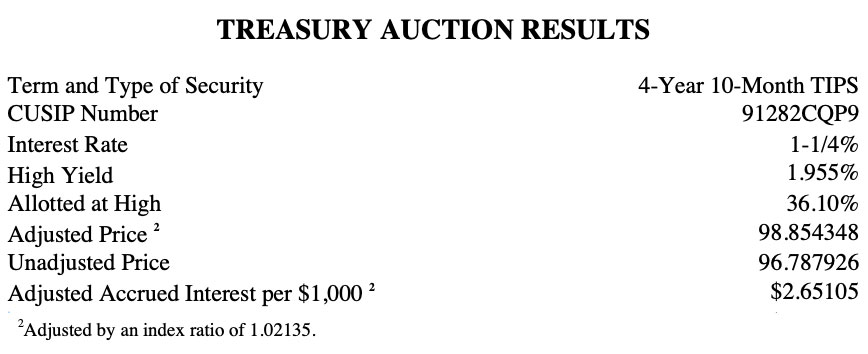

The Treasury’s reopening auction of a 5-year Treasury Inflation-Protected Security — CUSIP 91282CQP9 — generated a real yield to maturity of 1.955%, a good result for investors.

Real and nominal Treasury yields moved higher late Wednesday after the Federal Reserve held short-term interest rates in a range of 3.50% to 3.75%. But dot-plot projections from Fed members made it clear that rate increases could be coming later in the year if U.S. inflation does not begin cooling.

I watched Kevin Warsh’s news conference and I’d say he tried valiantly to make things look calm at the Fed, but there is a lot of apparent dissent. Other than that, I can’t say I know much more, since I am on holiday in southern France.

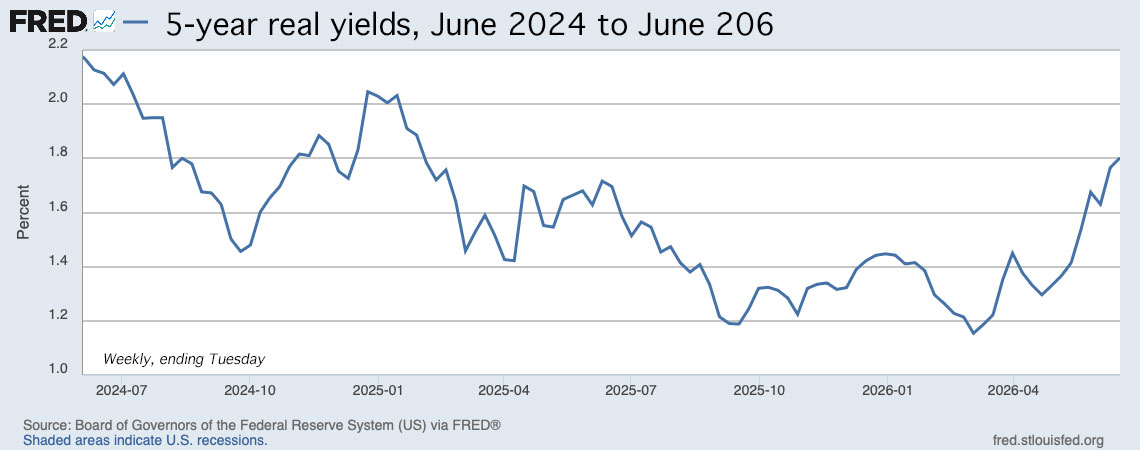

Before the Fed meeting, the 5-year real yield had been hovering in an already-elevated range of 1.78% to 1.82%. So today’s auctioned real yield of 1.955% was a sharp move higher. Plus, the auction drew solid demand. The “when-issued” prediction was 1.96% and the bid-to-cover ratio was 2.61, also a good number.

The statistics indicate we are entering a period of higher real yields. Maybe short term? Maybe not?

Consider this: Two months ago, this same TIPS generated a real yield to maturity of 1.367% at its originating auction on April 23. Today’s result was 57 basis points higher. That’s a big move.

Here is the trend in the 5-year real yield over the last two years, showing that today’s move higher is still off highs of late 2023, early 2024, and early 2025:

Pricing

Because the real yield of 1.955% was well above the coupon rate of 1.25%, this TIPS auctioned at a strong discount, with an unadjusted price of 96.787926. It also will carry an inflation index of 1.02135 on the settlement date of June 30. Here is the resulting cost of a $10,000 par value investment at this auction:

- Par value: $10,ooo.

- Adjusted principal on settlement date: $10,000 x 1.02135 =$10,213.50.

- Cost of investment: $10,213.50 x 0.96787926 = $9,885.43

- + accrued interest of $26.51.

In summary, an investor purchasing $10,000 par value at this auction paid $9,885.43 for $10,213.50 of principal on the June 30 settlement date. From then on, the investor will earn accruals matching official U.S. inflation, plus 1.25% annual interest on adjusted principal. The accrued interest will be returned at the next coupon payment on Oct. 15, 2026.

Inflation breakeven rate

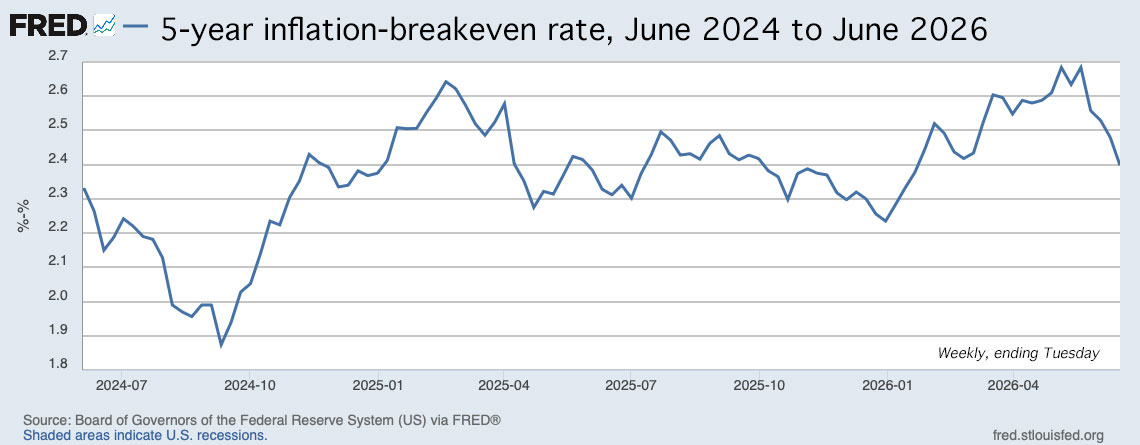

The 5-year Treasury note was trading with a nominal yield of 4.20% at the auction’s close, giving this TIPS an inflation breakeven rate of 2.25%, which seems low to me under current economic conditions. The originating auction in April got an inflation-breakeven rate of 2.58%. Inflation over the last 5 years, ending in May, has averaged 4.5%.

This week’s peace announcement, along with the potential for lower energy prices, is probably a big factor in easing inflation expectations.

Here is the trend in the 5-year inflation breakeven rate over the last two years, showing the strong move higher after the outbreak of war in the Middle East and the more recent move lower.

Thoughts

I spent the entire day in Aix-en-Provence, one of my favorite places on Earth, and really didn’t follow Treasury trends closely. I am assuming the Fed’s mixed messages created fears of rising short-term interest rates, and the 5-year TIPS maturity is the most sensitive, at auction, to those trends.

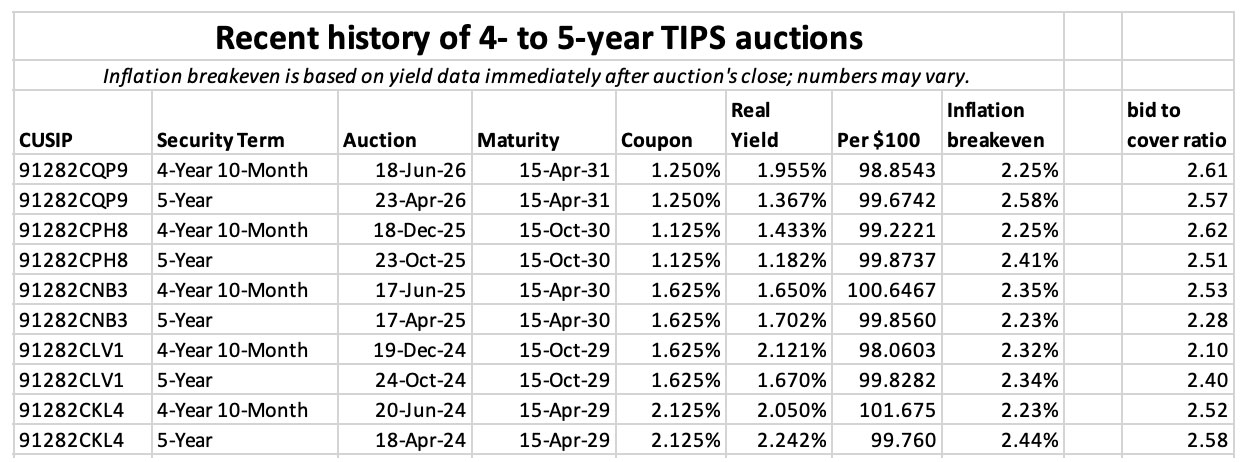

If you invested in this auction, or have other feedback or ideas, please start the discussion in the comments section. Without going into political rants, what did you think of Kevin Warsh’s performance? What should the Fed be doing? I will try to watch! Meanwhile, here is a history of 4- to 5-year TIPS auctions over the last two years.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I sent some paper bonds in for electronic conversion. The turn around time was about 3 months. 15 weeks.

There are about 163 million workers in the US with an average salary of about $70k. About 12 million or 7% are over the SS cap of 184,500. The average salary of these 12 million is around $300,000. $184,500 is already taxed so an average of an additional average of $115,500 could be taxed. Times 12 million that equals about $1.4 trillion. About $10 trillion of the total pot is already being taxed. So eliminating the cap should bring in approximately an addition 14% of revenues. Helpful, but I don’t know it solves the shortfall.

The SSA shows that eliminating the cap on social security taxes would eliminate 73% of the long range shortfall. https://www.ssa.gov/OACT/solvency/provisions_tr2024/charts/chart_run106.html

Fixing Social Security is really not hard at all, nor does fixing it result in terrible consequences, despite what thinktanks say. Failing to fix it, and the cut in benefits to the 75 million social security recipients, would be very damaging both to the economy and on a personal level for many, many people.

By the way, those who would advocate for deep cuts or eliminating social security do not advocate for eliminating the tax, which brings in $1.3 trillion in revenue to the govt.

Social Security’s problems are easily fixed and are not essentially financial. They’re political. Specifically, attitudes of a particular political philosophy toward concentrated wealth, the tax system, and the role of government.

The SS withholding rate could be raised a quarter of a percent and do even more to balance the books.

I’m new at this and bought this auction through my Schwab account. I’m trying to understand why the numbers Schwab is showing me for my purchase are different from what you’ve got listed in your piece above. I happened to stumble across this TIPS auction and placed the order, I believe it was around 7:45 AM Pacific on 6/18. Perhaps I missed the cutoff and got a different price as a result? The numbers Schwab is showing me for the purchase are as follows:

Lot Details: 91282CQP9 – UST INFL IDX 1.25%04/31INFL INDEX DUE 04/15/31

Open Date 06/18/2026

Quantity 10,000

Price $96.46875 (compared to the unadjusted price you list of 96.787926)

Cost/Share $99.00

Cost Basis $9,900.45 (compared to $9,885.43 in your analysis above)

Sometimes I hear from readers that the brokerage reported slightly different numbers. (The Treasury numbers are the exact result of the auction.) But in this case, it’s possible you simply bought CUSIP 91282CQP9 on the secondary market on the same day as the auction, so the prices should have been close.

I participated in this auction, and was pleased with the result, given the alternatives. The short term and low price make for a nice risk/return tradeoff. It’s not exciting, but a yield of nearly 2% is likely to cover most of the difference between the rate of increase in the CPI-U and the rate of increase in the cost of living. Whatever difference remains is the cost of hedging out most other risks.

My assumption is that the recent selloff in shorter-term TIPS is the market buying wholesale the idea that oil prices are going to drop dramatically and remain much lower for a long time, so the CPI-U will increase more slowly or perhaps even decrease in several months over the coming year. That would explain the relative lack of appetite for shorter-term paper: if the CPI-U were flat over the next year, a 2.25% breakeven on 4 year 10 month TIPS might make more sense (also, remember that this issue matures in April so it is likely that the last several months of 1 of the 5 years remaining will see the CPI-U decrease regardless). I am deeply sceptical of the thesis overall: inflationary forces are structural and preexisting, and oil is just one component of them. Also, the CPI-U does not depend on the price of oil futures on the CBOE but on the prices that are actually offered at retail, and the two are bizarrely disconnected. Moreover, the market seems to assume that Mr. Trump’s willingness to capitulate absolutely to Iran means that oil will be cheap. It seems to be forgetting that Mr. Trump’s behaviour is mostly irrelevant, the sole exception being the treatment of the SPR; what matters is Iran’s desire to obstruct and threaten shipping. Something that they are doing once again even as the ink dries on their MOU. It’s very clear that Iran has one and only one relevant economic asset and the mullahs intend to make the most of it. No amount of capitulation will make oil cheap again at retail, no matter what happens at the CBOE. So at a 2.25% breakeven this issue was cheap as you say.

I don’t have any new opinion on Mr. Warsh or the FOMC generally. The Fed exists to inflate. If the politicians did not want inflation, they would not need the Fed; gold served just fine as money for 8000 years when inflation was not desired. Mr. Warsh seems to be priming things to justify whatever he intended to do anyway, as politicians do. Prices will continue to rise, probably much faster than 2% per year, and the only open question is whether the CPI-U will be redefined yet again to deepen the extent to which it understates the rate of increase in the cost of living. Mr. Warsh and the Fed do not control the CPI-U so from the perspective of an investor in TIPS that’s not very interesting. If short rates do increase, there will be a tendency for the FOMC to declare victory prematurely, so if TIPS become cheaper as a result they will be a buy. We saw this repeatedly in the late 1960s and 1970s. We saw it again last year. Short rates are increased, the CPI-U rises more slowly, the FOMC declares victory and starts reducing rates even though the CPI-U is still rising far too fast, then it starts rising more rapidly again. I do not see today’s political and academic environment producing another Volcker to end that cycle, certainly not by the time Mr. Warsh’s term ends. TIPS out to 10 years remain a no-brainer on that basis, relative to other soft assets.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas… a rarity on the modern www. It seems to me that Chair Warsh will try to straddle the fence and show as few cards as possible (in hopes of minimizing criticism from the man who appointed him) while his masters attempt to figure out how to stack the FOMC with “pliable” members to achieve their desired political aims. My hope is that the independent system is strong enough to last another 2.5 years, and we can then return to the consensus that an independent Fed is a good thing, and we can leave in the rear view mirror any fears that the government will “substantially” cook the books to officially underestimate actual inflation. I stayed steadfast to my plan (based on said hopes) by filling out my 2036 TIPS ladder yesterday, at YTM 2.27. (I did not participate in the 5-year auction, only because my TIPS ladder is full in that time horizon.)

The biggest elephant is the Social Security payment trust/system or collapse thereof. With no noticeable/substantive discussion of the impact by the Fed is a sham(e)…all those recipients will be taking a big haircut to the gain of the party that wants to use those funds for other purposes, i.e. just like several agencies…cut the funding and they go south!

Eventually, we are going to see means testing based on AGI. Very unfortunate.

And very unnecessary.

Lifting the cap on the ceiling on the amount of wage/salary income subject to the tax which supports Social Security would solve its problems, as would (since the wealthy don’t derive most of their money from salaries) applying the tax to all income, regardless of type.

But, of course, that’s anathema to a certain political philosophy.

If we all resign ourselves to that outcome, we probably will. We can push for scrapping the cap instead, a cleaner and better approach to fully funding the trust fund for decades to come, but we will need to shed our the mass learned helplessness and push for that outcome.

Like most, most think there may be a legislative solution and what that may be…there could be no legislative solution! Get over it!

Dr, it’s not clear to whom your comment addressed, nor clear (at least to me, sorry) what it’s supposed to mean.

Social Secuity was created by legislation. Social Security, at its creation in the New Deal, was a “legistlative solution” to the precarity of old age in the “winner-take-all” economic system that existed before the New Deal. Social Security’s financial solvency has been shored up in the past by “legislative solutions,” and can be shored up by “legislative solution” again.

Get yourself a copy of U.S. Senate Report 111-187, “Social Security Modernization: Options to Address Solvency and Benefit Adequacy.” Then, among the many options considered, look at p. 46, which found that removing the cap on the amount of income subject to the Social Security tax would, by itself, without any other changes in the Social Security program, eliminate Social Security’s funding deficit for the following 75 years.

Unfortunately, that report was 16 years ago, and nothing was done, and so now Social Security is headed for another crisis. And the crisis itself gives a certain kind of politician a rhetorical window to disparage “entitlements” (a dog whistle word suggesting that tens of millions of shiftless people are acting like “entitled” parasites on the national budget) instead of raising taxes on the people and entities most able to pay taxes.

PS. Social Security is not a program for right now! Nor is foreign aid…on and on! The Q is really…what individual/party is advocating for an answer? None!

Excellent Book (2025) by Ray Madoff: The Second Estate. It reinforces the idea that just raising the cap won’t be enough since ultra wealthy don’t take an income and so don’t even contribute to FICA. ALL income should be taxed the same. Not holding my breath.

I see there is a discussion about possible solutions for Social Security insolvency. Here is a very good visualization of different proposals if anyone interested. https://www.crfb.org/socialsecurityreformer/

I made a small purchase for my IRA.

We will still have a fair amount more cash to reinvest (or spend) when these TIP bonds mature in 5 years.

I did the same thing as you.

I needed this issue for my ladder, and I was happy with the result. I’m optimistic about Warsh as well. I listened to the presser, and he came across as decisive vs. Powell’s more “we’ll just wait and see” approach. That bit him in the butt a few times during his tenure, but he still did a decent job with the hand he was dealt. I think Warsh is hyper-focused on the balance sheet, and will try to restore the Fed’s more independent and indirect approach to inserting themselves in markets. Contrary to consensus, I think he’ll be pragmatic too, and not overtly political either. He knows that Trump is only around for another couple of years, so just as Jeffrey Gundlach said, he’s “buying time” right now. He also understands the need to modernize the data flow. Using surveys via phone inquiries and constantly revising the data weeks and months later is slow, stale, and not reflective of the new information economy we are all living in now.

what is the difference in profit between this reopening and the original auction?

In terms of the security you receive, nothing at all. Same coupon, maturity date, accrual, CPI-U adjustment mechanism, etc. In terms of the price, they are separate auctions so each has a different price at settlement, as well as a different “inflation factor” and accrued interest you have to pay (which you receive later on with the next coupon).

I just built my first TIPs ladder this past week. Small to start, as I’m still learning the mechanics. I’ve bought 15 issues so far in modest amounts with an aggregate real yield of 1.85% which I’m happy with. Targeted the 7 year period from 2029 through 2035 as I believe somewhere in there the debt crisis will hit very hard and I’m not sure where money will be safe.

I also do believe that a point will come where the USA (i.e., the Federal Reserve Banks and their creditors messaging the Government) will have to at least slowly, yet seriously, deal with the national debt to satisfy their creditors…. if they want lower interest rates.

Inflation is one historically used option to reduce the relative debt (but not interest rates).

Perhaps if there were ever a realization of a debt crisis, our leaders could decide they must use one of the other options, to ether raise taxes to match expenses, or embark on a true effort of austerity (cut programs and services – doubtful option).

I made a small addition to my TIPS at auction, and the real yield works for me.

I didn’t watch the Fed / Warsh comments. Inflation information is provided by the federal government and confirmed by citizens feeling the impact of higher prices. Trying to say there is better information is ridiculous. Where is it? The Fed’s job is to take actions to reduce inflation and manage employment, not decide what inflation is. If inflation remains high, especially gas and food, in the short term, then doing nothing just to get past November is a complete failure to carry out the job for political purposes. Let’s hope that doesn’t happen, that inflation is “transitory”, and the deal with Iran actually stabilizes the oil supply. If not, I will buy more TIPS and get a good return.

Warsh is both accomplished and capable. I did not find him cryptic or cagey.

His repeated statements that inflation is a choice and this Fed will absolutely deliver 2% inflation is bothersome. Either he thinks Fed monetary policy is more capable of getting specific results than it is, or he plans to deliver 2% inflation and declare victory whether it is really 2% inflation or not.

His task forces may be needed; I do not know. They could also be laying the groundwork to say that inflation is 2% and we can cut rates, never mind that pesky CPI or PCE over there. He said he is very open to new and real time data sources.

While he did not demean the agencies producing the statistics and the Fed, he essentially said their methods and results are out of date or ineffective. That is a backhanded way of saying they are idiots, and I hardly think they are.

Personally, I like the idea of less communication and guidance. Warsh says markets will now react to real time data rather than to how the Fed will react to the data. Warsh seems to forget that before Greenspan began communicating in his cryptic manner, there was a cottage industry of Fed watchers and markets did react to anticipated Fed reactions. I suspect less communication will increase the (nebulous) risk premium, which is not a bad thing in my opinion.

I came away with lots of questions. Will hitting 2% (price stability) mean interest rate increases? Or changing the data? Can he get the votes to lower rates? That is probably a function of the task force outcomes, administration pressures and perhaps a SCOTUS ruling on Lisa Cook, who has incurred $1.3 million in legal fees to defend herself. When will changes come about? Not immediately but some likely in 3 months, as he indicated some things are urgent, with more change when the task forces are done by December. Are the task forces legitimate and balanced or composed of specific experts to justify a preordained conclusion? No idea, but Warsh is smart enough to not be too overt here.

Will this impact TIPS? Probably not the CPI adjustment which the Fed does not calculate. However, the level of interest rates, or the slope of the yield curve could change as a result of Fed actions, which would impact them.

I always keep an open mind to change. Things will reveal themselves in time, no doubt.

I liked the results… added a little more of this issue.

I didn’t participate in the auction because the 2031 rung of my TIPS ladder is full, but I did take advantage of the unique opportunity of high equity values plus high real yields to rebalance a chunk of equities to fill in most of the rest of my ladder (only pending 2037 – 2039 TIPS now). This is really a great time for anyone building a ladder.

This is my struggle. Stocks have gone through the roof— both domestic and international. Talk about an inflation hedge— wow what a party! When to take profits?

I took profits the end of last year and first of this year, better to be out wishing I was in than in wishing I was out. I used up all my carry over loses from 30yrs in the market. This year I gotta safe harbor and will pay my fair share. Lols of dry powder for the next shoe to drop.

“better to be out wishing I was in than in wishing I was out.”

Yes, exactly… I’d also rather be in TIPS and inflation is lower than expected than not be in TIPS and it’s higher.

Dr Matt….Sell and buy options

A comment on possible rate increases: It seems just a few months ago that me and everyone else “knew for certain” that rates would be dropping soon. This just goes to show how unpredictable interest rates movements actually are. It’s not easy being a market timer! I think Bogle had it right.

I thought he was cagey and cryptic. The manifest content of what he said, along the lines of “inflation is too high and we’re going to do something about it…” is of course sensible. But beyond that we can only guess what comes next. Your observation that he is likely dealing with much dissent in the committee is right on. He may be the chair but he’s only one vote. Democrats believe he’s a political animal and will behave accordingly. My guess is he tries his best to postpone any rate hikes until after the election and hopes by then they will become unnecessary. Remember the old adage “the giveaways happen before the election and the takeaways happen after…”

Trump only keeps proven subservients around – we all know that.

Hilariously, those objective data scientists over at Bloomberg just insisted over and over that Warsh is a hard pivot to a price stability focus.

Sure … I’ll hold my breath until, say, November!

What does Price Stability Focus really mean? Why do they need more committees to report to the committee. More smoke and stuff against the fan. Consumers Prices double and we jeer, prices pull back 50% from the inflated level and we cheer.

The market was surprised. Why? Because Warsh’s tone and focus was unexpected.

So am I the only one thinking he came in to establish his “rep” here as an inflation-fighting hawk, so as to seem more credible later when pushing to cut rates?

That would also be more consistent with his statements and bias before becoming Fed Chairman.

In other words, things are not what they seem… Did no one else see through or past this? Seems the financial press totally took the bait.

My opinion: The bait was there to be taken. Now we need to see actual actions.

So I guess the big question is……will Warsh be Trump’s sock puppet? Even after he strongly denied he would to congress, but what else would you expect him to say.