By David Enna, Tipswatch.com

While on holiday in France, I got an email from reporter Susan Tompor asking about the current attractiveness of Series I Savings Bonds. Are these investments drawing more attention as inflation rises?

My immediate reaction was, “yes, definitely.” But I added, “For savvy investors seeking inflation protection, TIPS are the more attractive investment right now, because market real yields have moved much higher than the 0.9% fixed rate on I Bonds.”

Responding to Tompor, my advice on I Bonds was to hold off on 2026 purchases until at least mid-October, when we will know the new variable rate and get a good idea of the next fixed rate, due to be reset on November 1. This is from her article:

If inflation continues to sizzle, Enna told the Detroit Free Press, it’s possible that the fixed rate could move to 1% or even 1.2% for I Bonds issued from Nov. 1, 2026, through, April 30, 2027. …

Enna said he bought I Bonds earlier this year but others may want to wait to see if they can get a higher fixed rate when buying in November or December.

It’s true that I bought my 2026 I Bond allocation in April and so I will have to be happy with a 0.90% fixed rate (which is fine). When the new fixed rate is announced in November, I will be able to load up on it through April 2027.

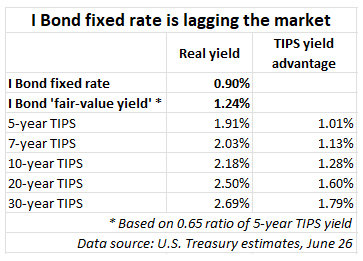

I Bond watchers believe the fixed rate is based, primarily, on this formula: Apply a 0.65 ratio to the 5-year TIPS real yield over the six months before the rate reset. At the last reset on May 1, the 5-year real yield was 1.33% and has now increased to 1.91%, a massive 58-basis point move higher in just two months.

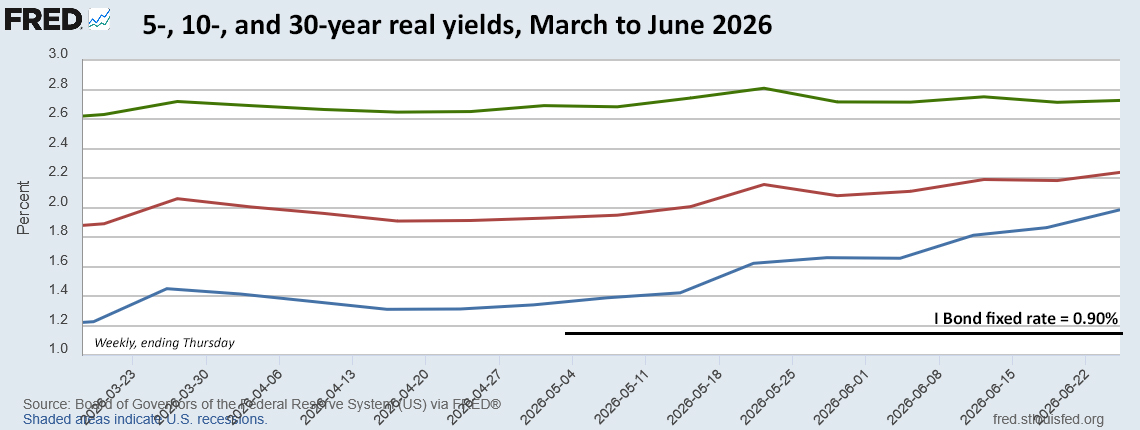

The I Bond’s fixed rate lags market changes, which can work for or against an investor. Right now the lag is a negative. Here is the trend in the 5-, 10- and 30-year TIPS real yields since March, compared to the I Bond’s fixed rate of 0.90%:

Note that the 5-year real yield — the key indicator for a future I Bond fixed rate — has been moving higher faster than the longer-term yields, which were already elevated. This should continue if the Federal Reserve decides to raise short-term interest rates later this year. (The move higher is probably an indication of market expectations of higher rates. Of the auctioned TIPS issues, the 5-year maturity is the most sensitive to Fed rate decisions.)

At today’s real yields, I’d assign a “fair-value real yield” of 1.24% to the I Bond, based on the 0.65 ratio of the current 5-year real yield of 1.91%. Because the 5-year TIPS has a strong yield advantage, I would favor it as an investment. The 5-year TIPS and I Bond are directly comparable, since the I Bond can be redeemed after 5 years with no penalty.

That same logic applies across the board for TIPS, because the I Bond’s fixed rate is lagging recent interest-rate increases:

What’s the strategy?

For TIPS investors, I’d say right now is a good time to build out a multi-year ladder with real yields near or above 2.0% for most maturities. Yes, real yields can continue rising, but getting a real yield of 2%+ is a good target.

For I Bond investors, do nothing right now. The fixed rate will remain at 0.90% and composite rate at 4.26% for any investment through October. So there is no need to act now to lock in a 0.90% fixed rate when it seems likely the fixed rate will rise at the November reset. And the variable rate could also rise above the current 3.34%. That seems likely, but I can’t predict future inflation.

I have been saying the November 1 composite rate could be “dazzling,” but that will depend on how quickly the oil shock recedes and other inflation cools.

If you already purchased your 2026 allocation — $10,000 per person per year — the gift box strategy remains an option for people with a trusted partner, at least for the time being. Also, the November 1 rate reset will remain in effect through April 2027, so investors can pile in after January 1.

Reminder: I Bonds have many advantages over TIPS, and those justify the 0.65 yield ratio: Rock-solid deflation protection, tax-deferred interest, full compounding of interest, flexible maturity, and lack of any market-price fluctuations.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I-bonds have some good features, and I have invested with them for almost 30 years. The continued lack of transparency from Treasury and awkwardness of the web site have led me to wind down my exposure over the coming years as my bonds get close to maturity. I would hate to expose my heirs the hassle of trying to receive money from these securities if I were to pass. TIPS work well enough in a tax protected brokerage account.

BTW, Susan Tompor is the best. Thanks for helping her out. I read all her columns in the Freep.

I just filled the 2037 to 2039 “hole” by buying an additional 3 years of the 2036 TIPS bond. My thinking was that taking advantage of a 2.2% real yield was too good an opportunity to miss rather than waiting for new bonds to be issued at possibly much lower yields.

It’s true I’ll need to re-invest when the bond matures to get some growth in 2037-2039 but that’s OK for me. I thought maybe this approach was worth sharing.

why is the i bond yield structured to be so much lower than tips? That, along with the investment limit makes i bonds generally unattractive.

The I Bond fixed rate is based on past real yield trends for the 5-year TIPS. The fixed rate remains for six months. At times, that is a positive for I Bonds when real yield dip sharply lower. But right now, that fixed rate is lagging.

Did you ever get confirmation that this is really the case that they’re based on 5-year TIPS trends? Last I read up on this, the treasury was opaque regarding how they made I-bond fixed rate determination. Note that I’m asking whether this is what they actually do or whether it’s just a pattern that we’ve all noticed that works for the last decade or so.

It’s a 100% reliable pattern over the last 10 years. The Treasury could change course at any time.

That wasn’t my question. I asked you if you have confirmation that this is what they’re actually doing vs. a pattern you and others have found. From your response, I take it that there is no confirmation from the treasury that this is how they actually set rates but it is just a pattern that has been discovered. Curve fitting or actually causal? No way to know without a statement from the Treasury. And, as you note, even if it is actually causal, they could always change it.

They’re such different beasts in how they operate that I’ve never been convinced that a comparison makes a lot of sense.