A multi-year surge in inflation made CUSIP 912828S50 a winner.

By David Enna, Tipswatch.com

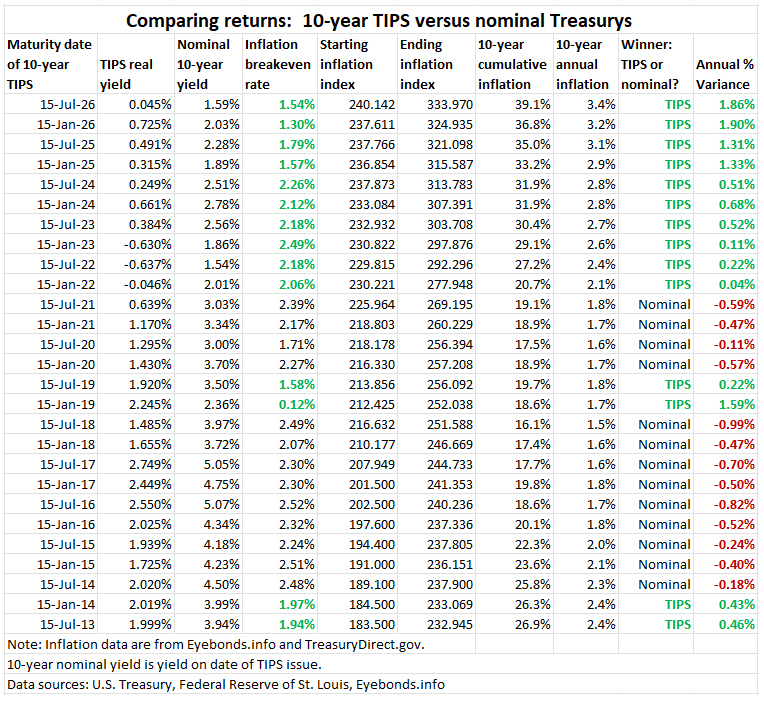

The summer of 2016 was a dark time for investors in Treasury Inflation-Protected Securities. By June of that year, 5-year real yields had gone deeply negative and in early July, 10-year real yields briefly dipped to -0.06% on July 8, 2016.

That set up very unpromising auction of a new 10-year TIPS on July 21, 2016, generating a real yield to maturity of just 0.045%, the lowest in more than three years. This was CUSIP 912828S50. The coupon rate was set at 0.125%, the lowest the Treasury will go on a TIPS.

The auction drew fairly strong demand, despite the very low real yield. Why? Because on that day a 10-year Treasury note was trading with a nominal yield of 1.59%, setting up an attractive inflation breakeven rate of 1.54%. That meant the TIPS would out-perform if inflation surpassed 1.54% over the next 10 years.

As it turned out, inflation has averaged 3.4% (rounded) over the last 10 years, making the TIPS a much stronger investment than the nominal Treasury, earning 1.86% more a year over 10 years. We know the final investment results for CUSIP 912828S50 because the May inflation report set its final inflation index for the July 15 maturity: 1.39327.

The TIPS generated a nominal annual return of 3.381% — in essence matching inflation over the 10 years. The Treasury note’s yield of 1.59% severely lagged inflation. For its moment in time, CUSIP 912828S50 was a very good fixed-income investment.

Simple lesson: A TIPS will out-perform when inflation rises to unexpected levels, as it has done over the last 10 years. The results for CUSIP 912828S50 continue a multi-year trend of TIPS benefiting from unexpectedly high inflation.

TIPS vs. an I Bond

An I Bond issued in July 2016 had a fixed rate of 0.10%, a slightly better return than CUSIP 912828S50’s real yield of 0.045%. Data from Eyebonds.info show that the I Bond has had an annual nominal return of 3.24% through June 2026, slightly less than the TIPS.

This result is a bit misleading because the I Bond on July 1 had just completed a composite rate of 3.22% and was transitioning to 3.44% for six months. And these results don’t yet reflect the surge in inflation in April and May 2026. In the end, the I Bond will slightly outperform the TIPS.

TIPS versus other alternatives

The total bond market, represented by Vanguard’s Total Bond ETF (BND) has had an average annual return of 1.47% over the last 10 years, trailing both the July 2016 TIPS and the I Bond.

The TIP ETF, which hold all maturities of TIPS, has had an annual total return of 2.32%, also trailing the TIPS and I Bond.

Vanguard’s short-term TIPS fund, VTIP, has had a annual total return of 3.02%, but still slightly trails the TIPS and I Bond.

Thoughts

Despite the gloom of investing in TIPS in the summer of 2016, those investments turned out to be relatively attractive for one reason: A strong surge higher in U.S. inflation, which continues today. Inflation protection brings value to your portfolio.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• TIPS investor: Don’t over-think the threat of deflation

• Upcoming schedule of TIPS auctions

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

On July 15, 2016 you could sell dollars at 1330 per ounce of gold, give or take. If you wanted dollars for that gold today you would get 4147 of them, an annualized dollar return rate of 12.05%. It’s not an investment, but it was an attractive alternative to this TIPS at the time of the auction if you were in the market for non-income-producing debasement hedges.

David, bro, hear me out: you do a lot of these posts and they’re great. Two things I’d like to see you add for the layman/dummy such as myself. 1) you show the total return stat as a percentage. That’s great, also maybe something like growth of 10k would be illustrative. So like, with TIPS 10k would have grown to 15k while treasuries would have grown to 13k etc.

Also, you may balk at this but may be helpful to compre this more against the broader investment universe. So if you put $10k into Tips, I-bonds, UST, Barclays Agg, and S&P 500, on the start date, what did they all grow to?

I know you aren’t calling TIPS/i-bonds a substitute or fair comparison to equity investments so you don’t want to show them side by side as the investment objective is completely different.

However, a lot more people (and people new to this site in particular) have more familiarity with the S&P and maybe you showing that side by side every now and again would reinforce the message that these are very different investments used for different purposes.

A question- I view AI search results as a possible threat to excellent niche sites like yours. Instead of finding a link to your site when they ask what is an I-bond, they will now get an AI generated answer. Have you seen traffic fall off over the past year or so? I think the bogleheads site has experienced this- less traffic, fewer questions posted, and they view it as ai driven.

On the value of a $10,000 investment, for I Bonds at least, that is very easy to find. Just go to EyeBonds.info, click on the I Bonds link and select the month of issue and $10,000 value: https://eyebonds.info/ibonds/home10000.html For the July 2016 I Bond, the value as of July 1 2026 was $13,788. For a TIPS, it isn’t as easy to figure out the exact cash flow since interest is paid out every year and does not compound.

In my reports on each matured issue (like this one) I include a comparison with the Total Bond Fund, which is essentially the same as the Barclays AGG. The S&P500 isn’t really relevant to a discussion of very safe investments: SPY’s total return has averaged 15.46% over the last 10 years. And this is why you want to have a diversified portfolio that includes equities.

On AI, generally, when you search for info on TIPS or I Bonds, you see information drawn from this site (with links, but come on). That is great and also super annoying. Both Bogleheads and this site benefit from reader opinions and contributions which add to the value.

Worth pointing out your comparison of this TIPS to a TIPS fund is not really apples to apples. A TIPS fund simulates a rolling TIPS ladder. So different vs a single purchased TIPS.

Yes, different. If you have a specific time period in mind, such as 10 years in this case, the individual TIPS is preferable in my opinion. If you are amassing inflation-protected money “for the future,” a TIPS fund can work. Investors just need to be aware that the predictable return of an individual TIPS is never possible with a general-purpose TIPS fund.

This discussion raises in my mind what is the optimal amount of inflation bonds to hold in a diversified bond portfolio? I own only I-bonds, no TIPS, and they constitute about 19%. More than half of that 19% is in I bonds purchased in 1999-2002 which have done spectacularly well. Perhaps they should be their own separate category because I will be forced to take distributions on those soon. All the others include EE bonds, core bond index funds, money market, TIAA traditional, a small bit of municipals and internatioal bonds, junk bonds, investment grade corporates. I’m not counting my emergency fund but perhaps I should at this stage. I haven’t retired yet but will in a few years. The bond market is so vast with so many choices I get overwhelmed and paralyzed into inaction.

Incidentally, inflation seems to be cooling fast. According to The Cleveland Fed inflation nowcasting, cpi has receded from over 4 a few weeks ago to around 3.5. Bloomberg is projecting not much in terms of central bank moves around the world in 2026-27.

CPI lags PPI by about 6 months.

PPI on June 11th was 6.5%, 5.1% excluding food and energy.

This upcoming week we should have updated PPI numbers, so if that remains in the same ballpark, we would expect that to move through the system and materially start to impact CPI towards the end of 2026.

We also are aware that oil prices are being kept in check by China opting to draw down their reserves, presumably in an effort to not spike global energy prices (it would hurt everyone, but they’re part of everyone), but at some point they’ll have to resume normal purchase volumes. Russia’s refining capacity is also being heavily targeted and there will be some eventual impact on energy prices.

Too early to tell, but PPI numbers in the next week will give an indication as to where CPI numbers are heading. Moreover, communication from the Fed consistently points to “the first part of the number” being the focus — as in 2.9% is more the goal than 2.0% — and there’s increasing expectation from large investment institutions that rate cuts are not only unlikely, but rate increases are becoming a possibility.

I’m not expecting a return to low rates or inflation in the very short term.

Thanks for raising the Kevin Warsh statement, “You’ve heard me say before, I tend to focus on the left of the decimal point. Well, the two is the left of the decimal point.” This definitely indicates that he would be willing to accept inflation up to nearly 2.9%, well above the traditional target. Despite the target, inflation over 30-year periods has never been lower than 2.3% for 30-year periods beginning in 1971. I’d say 2% inflation is a myth in the long term.

My household holdings have about 15% to 16% of the total in inflation protection. I am comfortable with that, but I also have a big holding of 2001 I Bonds that need to be redeemed in the next five years to ease the tax hit. Total bond funds have been dogs for a decade, but we still have core holdings there. Eventually, that will turn around, I suspect. I agree that inflation will cool off the May high of 4.2%, but even without the oil crisis, I think inflation was heading higher in 2026. So holding in the 3s through the end of the year?

Vanguard says their analyses land at 20-40% of fixed income in inflation adjusted bonds, which is what I follow.

If I looked at the percentage of just fixed income in our portfolio, it is about 30%, maybe a bit higher.

The war is back on so it remains to be seen how fast inflation cools.

Question for Mr. Enna – If the I Bond will outperform the 10 year TIPS in the end, when is “the end”? Is that for a July redemption to match the holding period of the TIPS bought at auction?

It’s true that the I Bond under-performed, slightly, in the 10-year period the TIPS existed. And if an I Bond holder bought in July 2016 and sold in July 2026, that investor earned 3.24% annually instead of 3.381% for the TIPS. The reason is that the I Bond’s rate-setting period ended in March and the TIPS benefited from 1 1/2 more months of inflation accruals: 0.85% in April and 1/2 of 0.63% in May. I Bond investors will get the benefit of those increases later on in the year. Overall, these turn out to be very similar investments.

Thanks for the analysis. I especially appreciate the comparison to alternatives. I was not an investor in TIPS at that time, but it gives me history to consider. The viability of VTIPS as an alternative is interesting.

Check out ICPI (Shares 0-1 Year TIPS Bond ETF). It is a Shares TIPS ETF with a duration of 0.53 versus VTIP which has a duration of 2.40.

ICPI has existed only since November 2025 and so it doesn’t have much of a track record. The fact that it is from iShares is attractive. The expense ratio is 0.09% versus 0.03% for VTIP, not a huge deal. Its YTD total return is 2.56%, versus 1.67% for VTIP, so that is a plus. At the moment, there are 5 TIPS maturing in the next year, so that is the basis of the portfolio. Not much risk here, I agree.