Historical evidence clearly shows non-seasonal inflation lags from October to December, picks up from January to March.

By David Enna, Tipswatch.com

The one really big thing I have learned while writing about inflation and inflation protection over the last 12 years is this: You can’t assume anything about inflation. Years ago, I was perfectly willing to make predictions. Now, after getting spanked by inflation again and again, I just say: “Let’s wait and see.”

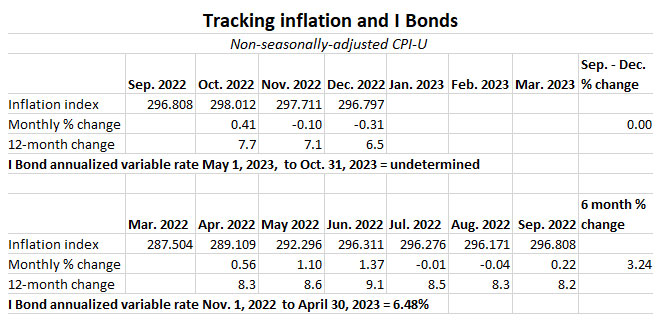

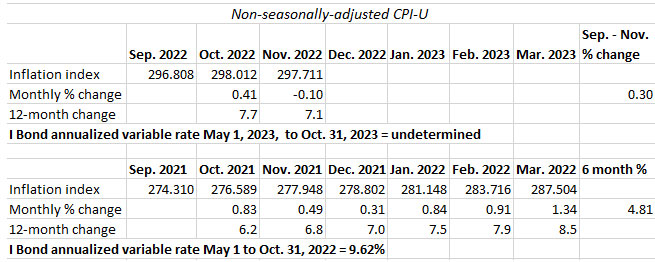

Take last year for example: When the June 2022 inflation report was released, the third in the six-month string for setting the I Bond’s variable rate, inflation was running at 3.03%. In just three months! That seemed to indicate — if this trend continued — the new variable rate could rise to 12% at the November reset. Several news reports touted 10% to 12% figures. I cringed.

The trend didn’t continue, and we hit three months of low inflation from July to September, resulting in a perfectly reasonable variable rate of 6.48%.

Now we are three months into a new six-month span that will reset the I Bond’s variable rate on May 1. The trend of seemingly low inflation is continuing and right now we are looking at a variable rate of 0.0%. Could that happen? Yes. Will it happen? Let’s wait and see.

Today, I decided to look at the last 10 years of October to March rate-setting periods for I Bonds, focusing on the ones where inflation started off slowly. And then ask: What was end result after the full six months? Let’s take a look.

2020

From October to December 2020, non-seasonally adjusted inflation ran at just 0.07%, indicating a “trend” toward a variable rate of 0.28%. But then inflation picked up from January to March 2021, and the resulting variable rate was quite a bit higher: 3.54%, annualized.

We saw a similar pattern in the April to September 2020 period, when inflation ran at -0.12% in the first three months, projecting a trend toward a variable rate of -0.48%. But then inflation popped higher, and the annualized variable rate ended up at 1.68%.

2019

From October to December 2019, inflation ran at 0.08%, projecting a trend toward an annualized variable rate of 0.32%. Inflation picked up (a bit) from January to March 2020, resulting in a variable rate of 1.06%.

2018

From October to December 2018, non-seasonally adjusted inflation ran at -0.48%, projecting a trend toward an annualized variable rate of -1.92%. At the time, I wrote this:

This is a fairly disastrous trend for holders of I Bonds, because even though an I Bond’s composite interest rate can’t go below zero, a negative variable rate will wipe out a matching amount of the I Bond’s fixed rate. … Still, this negative trend could reverse, at least partially, in the next three inflation reports.

And yes, the trend did reverse, with the annualized variable rate ending up at 1.4%.

2017

From October to December 2017, inflation ran at -0.12%, projecting the potential for a new variable rate of -0.48%. But then inflation rebounded in January to March 2018, resulting in a variable rate of 2.22%.

2016

Inflation from October to December 2016 ran at 0.0%, just like we are seeing in the last three months of 2022, projecting the potential for a 0.0% variable rate. But inflation rebounded from January to March 2017, resulting in an annualized variable rate of 1.96%.

2015

Non-seasonally adjusted inflation from October to December 2015 ran at -0.60%, projecting a possible trend toward a variable rate of -2.4%. Pretty disastrous, right? But it didn’t happen. Inflation rose enough in January to March 2016 to bring the variable rate up to 0.16%.

2014

Inflation from October to December 2014 ran at -1.35%, projecting a possible trend toward a variable rate of -5.4%. Deflation was bad, but not that bad. Inflation from February and March 2015 rebounded enough to get the variable rate to -1.60%, still a very ugly number.

Since I Bonds were first launched in 1998, there have been only two rate-setting periods resulting in a negative variable rate: This one in 2014, and the October 2008 to March 2009 period, which got a spectacularly low rate of -5.56%.

One oddity of I Bonds is that if you are going to have a negative variable rate, it’s better for it to be deeply negative. That’s because the composite interest rate can’t go below 0.0%, so you won’t lose a cent of principal, and you will be out-performing inflation for those six months. When inflation rebounds higher, you get the full benefit without suffering any penalty for deflation.

Historical perspective: A lesson learned

I could have continued this listing. In 2013, the October to December period ran at -0.47%, but the resulting annualized variable rate was 1.84%. In 2012, the October to December period ran at -0.78%, but the resulting variable rate was 1.18%. That is far back as my compiled data go.

Even if you look at 2021, when inflation was surging, the October to December period ran at 1.63%, projecting a trend toward a possible variable rate of 6.52%. But inflation surged even higher in January to March 2022, resulting in the epic variable rate of 9.62%.

Clearly, since this trend has continued for 10 straight years, non-seasonally adjusted inflation tends to under-report in the October to December period, and then rebound in the January to March period. This was easily seen in the November inflation report, with seasonally-adjusted inflation coming in at 0.1%, but non-seasonal at -0.1%. And then for December, seasonally-adjusted was -0.1%, while non-seasonal was -0.31%. Seasonal and non-seasonal balance out over 12 months, so we should see some gains in non-seasonal inflation in the months ahead.

So back to the question: Will the I Bond’s variable rate go to zero at the May 1 reset? Based on this historical evidence, I don’t think it will. It will be higher that 0.0%. But anything can happen. Let’s wait and see.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It has been said that all wars are wars of religion. Our country is based on Judeo-Christian principals, along with…