TIPS remain attractive. And now bank CDs are worth a serious look.

By David Enna, Tipswatch.com

It’s been kind of wild to go from seeing the possibility of TIPS with a real yield of 2% in early March to the possibility of 1% as we head into April.

The significant event in this downdraft came March 8, when Silicon Valley Bank announced a $1.8 billion loss on the sale of securities, including Treasury and mortgage bonds. The next day, shares of Silicon Valley Bank fell 60% and depositors began an social-media-fueled run on the bank.

The failure of SVB and Signature Bank led to a Federal Reserve bailout of non-protected depositors. And that bailout in turn fueled speculation that the Fed would soon pause its planned interest rate increases. But in the background, inflation still looms over the U.S. economy.

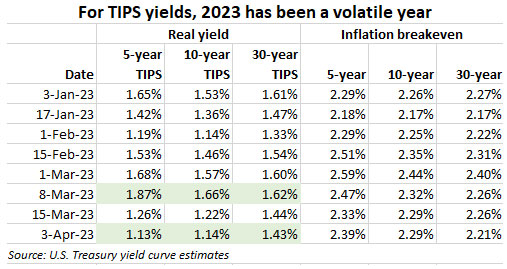

Here is the year-to-date trend for real yields on 5-, 10- and 30-year TIPS, along with the matching inflation breakeven rates:

I’ve highlighted this year’s high for real yields, which came on March 8, and also the low, which came 19 days later on April 3. Inflation breakeven rates haven’t been greatly affected by this turmoil, indicating that nominal yields have been tracking closely with real yields.

In the midst of this market turmoil, a 10-year TIPS was reopened at auction on March 23, getting a real yield to maturity of 1.182%, marking a drop of about 48 basis points in two weeks. Since then, real yields have continued falling.

Next up is a Treasury auction of a new 5-year TIPS on April 20. In just over a month, that upcoming auction has gone from looking stellar (real yield of 1.8%+) to looking just okay (real yield of around 1.13%). But a lot can happen in the next two weeks. I’ll be posting a preview article on that auction on Sunday, April 16.

I’ll point out that things continue to change quickly. Real yields appear to be heading even lower today.

What this all means

TIPS remain attractive. It’s painful to watch real yields decline right before you purchase a TIPS, but at this point real yields for TIPS remain above 1%. That’s a decent number given the ultra-low rates of the last dozen years. I’ll probably still be a buyer at the April 20 auction.

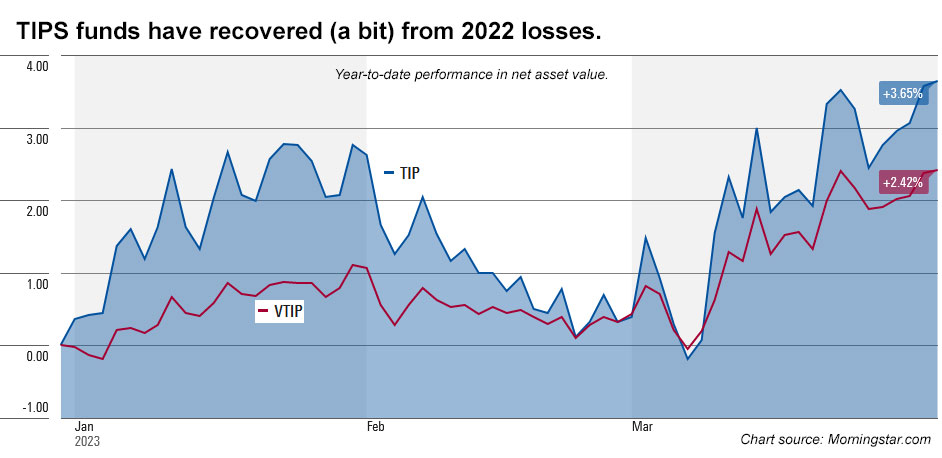

TIPS funds and ETFs are getting a boost. With markets anticipating a Fed rate slowdown, bond funds have been doing well in 2023. The broad-based TIP ETF is back above $110 (trading today at $110.66) after falling to as low as $104.96 last October. Holders of these TIPS funds can breathe a sigh of relief after a disastrous 2022.

Here is the year-to-date trend in the net asset values of the iShares TIPS Bond ETF and Vanguard’s Short-Term Inflation-Protected Securities ETF:

What about I Bonds? We are going to get a reset on both the fixed and variable rates for the U.S. Series I Savings Bond on May 1. The variable rate will probably fall to a range of about 3.2% to 3.5%, down dramatically from the current 6.48%. The fixed rate looks likely to hold at around 0.4%, I think, or just a bit higher.

I’ll still be a buyer up to the $10,000 purchase limit, probably in April but possibly in May. We’ll know more after the March inflation report is released on April 12.

I know a lot of investors will be bailing on I Bonds this year, but I like them as a long-term investment, pushing inflation-adjusted cash into the future with zero risk. Sometime in the future, I believe, interest rates will again be near zero and I Bonds will be out-performing every other safe investment.

Nominal Treasurys are losing appeal. Thinking of investing in nominal Treasury bills, notes or bonds? Focus on the T-bills with maturities of 6 months or less, where yields continue to be appealing. Here’s a comparison of Treasury estimates from March 8 to April 3:

While short-term rates have declined slightly, the drop in medium-term Treasury rates has been much more dramatic, with the yield on a 2-year Treasury note down 108 basis points and the 5-year down 82 basis points. The 10-year note is down 55 basis points, surpassing the 39-basis-point decline in the 10-year TIPS real yield. I my opinion, this makes TIPS more appealing versus the nominal Treasury.

Bank CDs are gaining appeal. I posted an analysis Sunday morning noting that certificates of deposit offered by banks and credit unions are becoming more attractive as financial institutions scramble to build deposits. One- and two-year CDs are now yielding more than 5%. You can find a 5-year CD with a yield of 4.5%, which sets up an inflation breakeven rate of 3.4% versus a 5-year TIPS. That looks compelling.

Will inflation average more than 3.4% over the next 5 years? It’s possible, but it’s a close call. That makes TIPS and high-yielding bank CDs complimentary investments.

Cash is now A-OK. Getting 4%+ safely on your cash holdings is a wonderful thing, after years of earning around 0.01%. (It was strange at tax time to realize you didn’t have to report your lofty annual interest of 92 cents.)

Those ultra-low interest rates forced many investors to take risks, boosting bizarre investments like Dogecoin, NFTs and GameSpot. But I should mention that one very safe investment — the U.S. Series I Savings Bond — also surged in popularity as inflation began rising.

Now cash is earning a spot in your portfolio. For shorter-term cash needs, T-bills are the choice, or a high yielding Treasury money market fund like Vanguard’s VUSXX. In a recent article, investment manager William Bernstein made the case for combining TIPS for the long term and T-bills on the short term. He noted:

A TIPS is risky in the short term and riskless in the long run, which is precisely the opposite of, and complementary to, a T-bill, which is riskless in the short term but, because of reinvestment rate volatility, risky in the long run.

Final thoughts

TIPS remain appealing because of the inflation protection they provide as we are head into an uncertain future. For me, I Bonds will remain an automatic investment. I will continue to roll over 13- and 26-week Treasury bills as a core cash holding. And will keep hunting for attractive CD rates, either directly from banks or through brokerages.

In other words: I’m staying the course. What do you think? Post your thoughts in the comment section below.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

That prompted me to add to my TIPS today.