I’m traveling in Costa Rica for a couple weeks and I will often be in areas with weak or zero Internet connections. So I won’t be writing much and I may miss responding to some of your questions.

The holiday season is here but the news never stops. Fed Chairman Jerome Powell gave the stock and bond markets a boost Wednesday by suggesting that the December rate move by the Fed might be less aggressive. In other words, an increase of 50 basis points is coming. Just like everyone already knew. This was the Fed “signaling” the obvious. And of course the stock and bond markets are celebrating with a rally — stocks higher and bond yields lower.

On Dec. 13 at 8:30 a.m. EST the Bureau of Labor Statistics will release the November inflation report. I will be back at work that day, but I have no idea what to expect. The Cleveland Fed’s Inflation Nowcasting site is projecting an all-items increase of 0.47% for November and 7.49% year over year. But these Nowcasting predictions have been too high recently. We’ll see.

One day later, on Dec. 14, the Federal Reserve will announce its decision on the new federal funds rate. The obvious expectation is a 50-basis-point increase to a range of 4.25% to 4.50%. The Fed could be closing in on a “terminal” rate, but a lot will depend on future inflation reports and the status of the U.S. economy.

Then, a week later, on Dec. 22 at 1 p.m., the Treasury will close its auction of a reopening of CUSIP 91282CFR7, creating a 4-year, 10-month Treasury Inflation-Protected Security. This will be an interesting auction, coming a week after both the November inflation report and the Fed’s rate hike decision. Because this TIPS has a coupon rate of 1.625%, it’s possible it will be selling at a premium price. It is currently trading on the secondary market with a real yield of 1.29%, a stunning decline from the originating auction’s yield of 1.732% just six weeks ago. (And I’m just reminding everyone I called that October auction a unicorn — a rarely seen event. Looks like I might have been right.)

I will be posting a preview story on that TIPS auction on Sunday, Dec. 18, and posting the result on Dec. 22 after the auction closes.

Finally, on Jan. 1, 2023, the I Bond purchase calendar will reset and allow new purchases of up to $10,000 per person for that calendar year. Because the I Bond’s fixed rate is now 0.4% these savings bonds will remain attractive. I’ll be posting an I Bond buying guide for 2023 in early January.

Happy holidays and thanks for reading.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Despite the I Bond’s appeal, investors shouldn’t ignore the sizable yield advantage for TIPS.

By David Enna, Tipswatch.com

We’ve just gotten through a year of “I Bond mania,” which has brought a lot of welcome attention to a little-known, rarely discussed, but very safe and sensible investment. Now I have a news alert: I Bonds are no longer the star of the inflation-protected universe. That role has shifted to Treasury Inflation-Protected Securities, with real yields now hitting decade-plus highs.

I like both investments, and I will continue to buy both. But because of this year’s surge in real yields, TIPS have become much more desirable. Combine that with a sense of urgency, because there is no way to know how long this advantage will last. Here are the numbers from Friday’s market close:

I Bond: Current fixed rate of 0.4%, which equates to a real yield (above inflation) of 0.40%.

5-year TIPS: Current real yield of 1.71%, a yield advantage of 131 basis points over the I Bond.

10-year TIPS: Current real yield of 1.57%, a 117-basis-point advantage.

30-year TIPS: Current real yield of 1.63%, a 123-basis-point advantage.

Here is a chart showing how the advantage has shifted strongly to TIPS in the last half year:

Click on the image for a larger version.

Does this mean you should be rushing to sell your I Bonds to buy TIPS? Absolutely not. I Bonds have a key advantage over TIPS as a short-term investment, because their current interest rate is backwards-looking, based on past six-month inflation. The I Bond’s current inflation-adjusted variable rate is 6.48% annualized, for six months. That is too attractive to ditch.

But as an investment you plan to buy and hold for 5 or more years, TIPS have a huge yield advantage over I Bonds. That shouldn’t be ignored. It is “normal” (historically, I mean) for the fixed rate of the I Bond to lag below the TIPS real yield. That’s okay, because I Bonds have a lot of other desirable features.

Advantages of I Bonds vs. TIPS

Both I Bonds and TIPS protect you against unexpected inflation. If inflation in the next 30 years suddenly soars to 7%, 10%, 15%, your principal will increase by that amount because of the inflation-adjusted interest rate for I Bonds or inflation accruals for TIPS.

I Bonds are a simple investment to buy and track, much simpler than a TIPS with a constantly changing market value and inflation accruals that update daily.

I Bonds accurately track U.S. inflation but can never go down a cent in value if we hit a period of deflation. This isn’t true for TIPS, which lose some principal value after every month of deflation.

I Bonds earn tax-deferred interest, while TIPS in a taxable account get hit by current taxes on both the coupon rate and the inflation adjustments in any year, even though the inflation accruals aren’t paid out until the TIPS matures or is sold.

I Bonds can be used tax-free to pay for educational expenses, under some circumstances.

I Bonds don’t trade on any secondary market and their value is never at risk if interest rates rise.

I Bonds allow you fantastic flexibility. You can redeem them after one year, costing you three months of interest. Or redeem them after five years and pay no penalty, or just hold them for 30 years and cash out.

Disadvantages of I Bonds vs. TIPS

As I noted above, I Bonds currently have a real yield well below the real yield of TIPS of all maturities.

I Bonds can’t be purchased in a tax-deferred account. This can make raising money for an I Bond purchase difficult, especially for retired people with no regular income. TIPS can be purchased in a tax-deferred brokerage account, so raising the money can be done without tax consequences.

I Bonds can’t be sold for a year, and there is a 3-month interest penalty for redemptions before 5 years. TIPS can be sold in the secondary market at any time, possibly at a loss or possibly at a gain.

In times of very low inflation, your 6-month annualized return for I Bonds can drop to a very low level, even 0.0%. But I Bonds in this case may outperform TIPS, which would lose principal value in that scenario.

Keep in mind, however, that even during times of deflation, a TIPS will continue to pay out its coupon rate. So a TIPS with a higher coupon rate has some added deflation protection. For example, the new TIPS issued in October has a coupon rate of 1.625%, so that is a buffer against annual deflation of at least 1.625%.

I Bond purchases are capped at $10,000 per person per year. TIPS purchases are essentially unlimited. It takes a lot of years of investing to build a sizable allocation in I Bonds. With TIPS, you can do that in a day.

I Bonds can only be purchased in electronic form at TreasuryDirect, a government site that has many critics. TIPS can be purchased at any major brokerage, often with zero commission and fees.

I Bonds can’t be sold on the secondary market, meaning there is no way to capture a capital gain if interest rates fall substantially. TIPS can be traded for gain or loss.

You cannot create a joint account at TreasuryDirect, so a couple would need to set up two accounts, one with I Bonds registered as Spouse 1 with Spouse 2, and the other, Spouse 2 with Spouse 1.

Why advantage TIPS?

We’ve gone through a decade-plus of extremely low interest rates, thanks to Federal Reserve interventions in the Treasury market. Real yields — meaning yields above inflation — were negative for much of this time. We have finally come out of this misery with a bang: Real yields for TIPS are now reaching levels we haven’t seen since 2008, in the case of the 5-year TIPS, and 2010 for the 10-year TIPS. At the same time, the market continues to price in fairly low future inflation, just 2.29% over the next 10 years, based on the last 10-year TIPS auction. That makes TIPS appealing versus nominal Treasurys.

I Bonds remain a great investment, in my opinion, and I will definitely be buying them up to the purchase limit in 2023. I Bonds are superior as a short-term investment of 1 to 2 years because of their backward-based interest rate and predictable return.

But TIPS right now are a superior longer-term investment, based solely on these historically attractive real yields. As I noted in a recent article, I was able to nab a 20-year TIPS with a real yield of 2.02% on the secondary market, and also filled 2030 and 2031 slots in my TIPS ladder with real yields just a bit over 1.5%. You can’t do this kind of investing with I Bonds, because of the $10,000 per person per year limit on purchases.

I imagine that a lot of I Bond faithful will disagree with my opinion, and I do understand that I Bonds are very attractive because of their simplicity, safety and rock-solid deflation protection. But TIPS are just a better investment in November 2022. Real yields of 1.5% are now available across the TIPS yield spectrum. Is that attractive? Just take a look at where we were a few months ago:

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Fed president James Bullard gave auction investors a gift today.

By David Enna, Tipswatch.com

James Bullard

Investors in today’s Treasury offering of $15 billion in a 10-year TIPS reopening auction should give a tip of the hat to St. Louis Fed president James Bullard, who shook up the bond market (just a bit) with some hawkish rhetoric on interest rates. According to CNBC:

“Thus far, the change in the monetary policy stance appears to have had only limited effects on observed inflation,” Bullard said. “To attain a sufficiently restrictive level, the policy rate will need to be increased further.”

Bullard contended that 5% could serve as the low range for the where the funds rate needs to be and that upper bound could be closer to 7%.

A federal funds rate of 7%? That’s a mighty jump from the current range of 3.75% to 4.00% and seems rather alarmist. But Bullard is continuing the Fed’s unofficial strategy of talking tough whenever the stock and bond markets seem to be getting euphoric. The result: Stock and bond markets yawned and took it mostly in stride, with bond yields inching — but only inching — higher this morning.

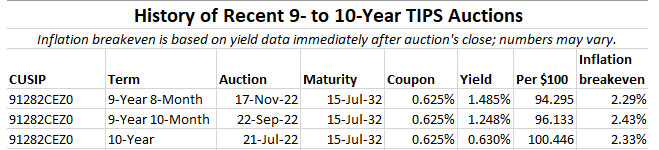

All of this led to the 1 p.m. close of the reopening auction of CUSIP 91282CEZ0, creating a 9-year, 8-month Treasury Inflation-Protected Security. This TIPS, which trades on the secondary market, closed Wednesday with a real yield of 1.37%. But Bullard’s comments appeared to give investors some caution, pushing the auctioned high yield up to 1.485%. The bid-to-cover ratio was a mediocre 2.25, indicating fairly weak demand.

Because the auctioned real yield was much higher than the coupon rate of 0.625%, investors got this TIPS at a discount, with an adjusted price of about $94.29 for about $102.15 of principal, after accrued inflation is added in. This TIPS will have an inflation index of 1.02147 on the settlement date of Nov. 30.

For today’s investors, all is good. The real yield of 1.485% was the highest for any 9- to 10-year TIPS auction since April 2010, when a 9-year, 9-month TIPS got a real yield of 1.709%. For anyone counting, there have been 75 TIPS auctions of this term since April 2010. Today was a milestone.

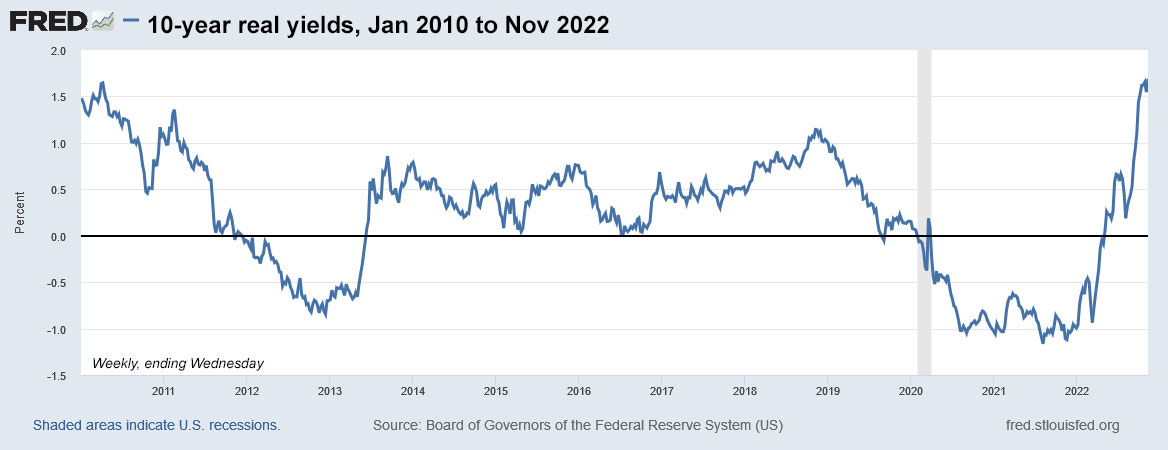

Real yields have been climbing throughout 2022, a trend that escalated in March once the Federal Reserve committed to increasing interest rates and cutting its balance sheet in the face of 40-year-high U.S. inflation. Here is the year-to-date trend in 10-year real yields:

Click on the image for a larger version.

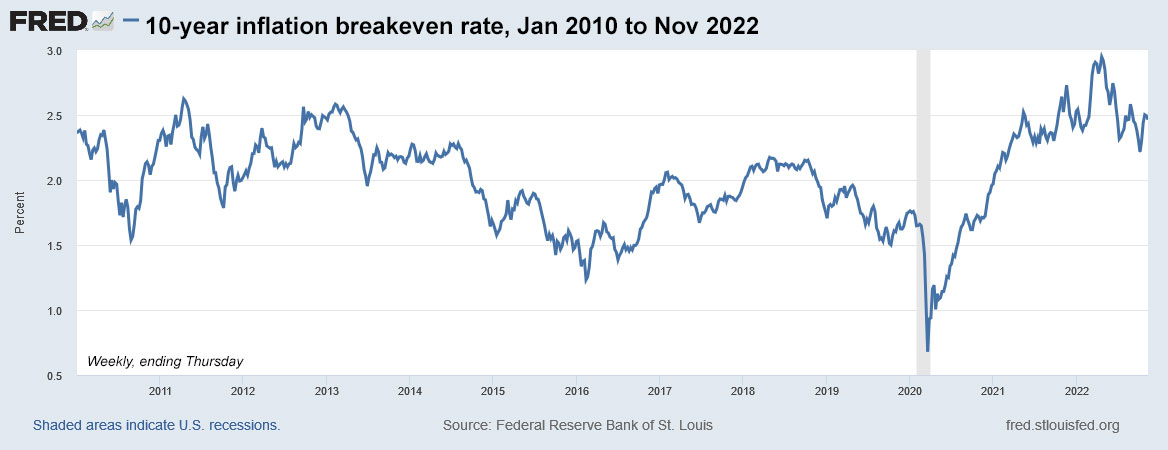

Inflation breakeven rate

At the auction’s close at 1 p.m. ET, the nominal 10-year Treasury note was yielding 3.77%, giving CUSIP 91282CEZ0 an inflation breakeven rate of 2.29%, the lowest for this term since an auction in July 2021. That’s an attractive rate, in my opinion, making this TIPS a decent bet versus a 10-year Treasury. If inflation averages more then 2.29% over the next 10 years, this TIPS will out-perform. Inflation over the last 10 years, ending in October, has averaged 2.6%.

Here is the year-to-date trend in the 10-year inflation breakeven rate, showing how inflation expectations have been trending downward as the Federal Reserve maintains its hawkish posture:

Click on the image for a larger version.

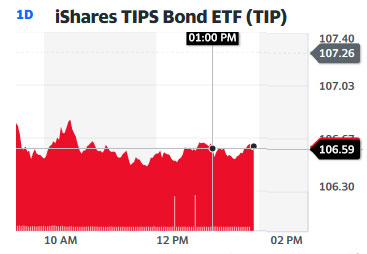

Reaction to the auction

Source: Yahoo Finance

The overall TIPS market had been trading lower all morning, indicating higher yields, as shown in the one-day chart for the TIP ETF, which holds a broad range of maturities. This chart is all about the statements by Fed president James Bullard, and the auction result had almost no effect on TIPS prices.

So, investors at today’s auction got a gift from Bullard, amounting to an 11-basis point increase in real yield over the next 9-years, 8 months. Getting the highest real yield in 12+ years looks like a solid investment.

Today’s auction closes the books on CUSIP 91282CEZ0, a TIPS that transitioned the 10-year market from remnants of the easy money days of 2021 to the tighter policies of 2022. Its coupon rate of 0.625% — which now looks low — was the highest for any TIPS of this term since May 2019. A new 10-year TIPS will be auctioned on Jan. 19, 2023.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Have we passed the peak for real yields? Or is this another head-fake?

By David Enna, Tipswatch.com

Well, that was a wild week. Look back to Nov. 3, when both 5- and 10-year TIPS real yields were closing in on 12-year highs, with the 5-year at 1.82% and the 10-year at 1.74%, based on U.S. Treasury estimates. Then came Thursday’s October inflation report, and everything changed.

October inflation came in well below expectations, only the second downside surprise in more than a year. Annual all-items inflation was running at 7.7%, below estimates of 8.0%, and core inflation came in at 6.3%, below estimates of 6.6%. Both the stock and bond markets took this as a signal the Federal Reserve can soon begin easing future interest rate increases. The S&P 500 soared nearly 6.5% in the next two days. The U.S. bond market — represented by the AGG ETF — rose about 2.1% in a single day (the bond market was closed Friday in honor of Veterans Day).

For bonds, higher prices equal lower yields. And real yields on Treasury Inflation-Protected Securities moved substantially lower from Nov. 3 to Nov. 10, according to Treasury estimates:

The 5-year real yield fell from 1.82% to 1.48%, a drop of 35 basis points.

The 10-year real yield fell from 1.74% to 1.43%, a fall of 31 basis points.

The 30-year real yield fell from 1.76% to 1.58%, a drop of 18 basis points.

And now, on Thursday, the Treasury will offer $15 billion in a reopening auction of CUSIP 91282CEZ0, creating a 9-year, 8-month TIPS. At this point, although real yields are down, this TIPS still looks attractive. But we are entering a week of high uncertainty.

I’ve been a fan of this TIPS, buying a small amount at the originating auction on July 21, which produced a real yield of maturity of 0.630% and set the coupon rate at 0.625%. At the time, that was the highest coupon for a new TIPS in three years. Then I bought a larger amount in the first reopening on Sept. 22, which boosted the real yield to 1.248%, the highest in more than 12 years.

CUSIP 91282CEZ0 trades on the secondary market, and at the week’s close it had a real yield of 1.40% and a price of $92.98 for $100 of value, according to Bloomberg’s Current Yields page. That quote may include some international trading on Friday, because it is a bit below the Wall Street Journal‘s Thursday real yield estimate of 1.432%.

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.40% means an investment in this TIPS will exceed U.S. inflation by 1.40% for 9 years, 8 months. If inflation averages 2.5%, you’d get a nominal return of 3.9%, pretty much on par with a nominal U.S. Treasury. But if inflation averages 4.5%, you’d get a nominal return of 5.9%.

So let’s go with the real yield of 1.40% and price of $92.98, which is below par value because the real yield is currently well above the coupon rate of 0.625%. This TIPS will carry an inflation index of 1.02147 on the settlement date of Nov. 30. That means investors will be paying about $94.98 for $102.15 of accrued value, plus maybe 23 cents more for accrued interest.

An investor buying $10,000 in par value of this TIPS will pay about $9,521 for about $10,215 in accrued value plus $23 in accrued interest. That is a rough estimate and things can change before Thursday.

It’s still attractive. While we might have been dreaming two weeks ago of 10-year real yields reaching 2.0% or higher, a yield in the range of 1.40% is still attractive, at least in view of the past decade of ultra-low interest rates. It would be the highest real yield for any 9- to 10-year TIPS auction since April 2010, when a 10-year TIPS reopening auction got a real yield of 1.709%.

Here is the trend in the 10-year real yield over the last 12 years, showing that current yields remain at decade-old highs:

Note that Treasury data for this chart does not include Thursday, when the real yield fell 21 basis points.

With the nominal 10-year Treasury note now yielding 3.81%, a 10-year TIPS with a real yield of 1.40% gets an inflation breakeven rate of 2.41%, in line with recent auction results. Inflation expectations have been falling in recent months, as the Federal Reserve shows resolve in fighting inflation with higher interest rates and balance sheet reductions. At this point, with U.S. inflation running at 7.7% annually, this breakeven rate looks reasonable.

Here is the trend in the 10-year inflation breakeven rate over the last 12 years, showing that the current rate remains at the top end of the historical range, but below the surge to nearly 3.0% in April 2022, just as the Federal Reserve was beginning to tighten:

Thoughts on this auction

Have we hit a top in the trend of higher real yields? Or was last week’s volatility just another head-fake in a year of bond market fluctuations? Personal opinion: It’s hard for me to resist this auction, since I have bought this same TIPS twice at lower real yields. On the other hand, have I already bought enough TIPS maturing in 2032? Should I look elsewhere? Should I wait until January’s auction of a new-issue 10-year TIPS, when real yields could be even lower? (Or not.)

Each investor will need to find answers to those questions. My general feeling throughout 2022 has been to load up on TIPS while real yields are attractive. My fear: This might not last long. Then again, maybe we have entered a “new era” in the U.S. bond market? Uncertainty.

As an alternative to this 10-year TIPS auction, I have considered going to the secondary market to buy TIPS maturing in 2030 and 2031, two holes in my TIPS ladder caused by the ultra-low yields of the 2020 to 2021 era. Those TIPS also had deep declines in yields after the October inflation report:

I checked on Fidelity’s trading platform Saturday morning and prices were slightly higher than Thursday’s close, but I can’t view prices for smaller lots. (Vanguard’s platform no longer lists any of these, not sure why.) There’s no way to know what we will see Monday, but if the real yields on these remain higher than the current yield of CUSIP 91282CEZ0 I might head in this direction to fill gaps in my TIPS ladder. Then I would look to fill the 2033 slot in January.

I still view this reopening of CUSIP 91282CEZ0 as a solid investment, despite the dip in yields. If you are considering investing, make sure to watch Bloomberg’s Current Yields page for real-time updates on its yield and price. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. ET Thursday.

Here is a history of 9- to 10-year TIPS auctions back to 2018, when the Federal Reserve launched its last tightening cycle, lasting until early 2020. Note that one year ago, on Nov. 18, 2021, a 10-year TIPS reopening got a real yield of -1.145%, the lowest in history for this term.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

It is CUSIP 912810RA8, first auctioned on Feb. 13, 2013. It wasn’t a great investment back in 2013. But now …

By David Enna, Tipswatch.com

Earlier this week, on Wednesday afternoon, I did something I’ve never done before: I bought a TIPS on the secondary market. Oh sure, many of you have done that many times before. But not me. I’m the “buy at auction and hold to maturity” guy.

Why would I do that? Because I had been eyeing the potential to buy a TIPS, probably with a maturity of around 20 years, with a real yield to maturity higher than 2.0%. Each day, sometimes several times a day, I’d take a look at TIPS maturing in 2040 to 2044, which seemed to be the sweet spot for that 2.0% real yield. (The 30-year TIPS — which I would not buy — actually had a lower real yield.)

The U.S. Treasury, unfortunately, stopped offering 20-year TIPS at auction back in January 2009 and very few were ever offered. I’ve argued it would be an excellent addition to the TIPS lineup, but the Treasury doesn’t seem to listen to me. The lack of this maturity creates a “hole” in TIPS maturities, with zero TIPS maturing from July 2032 to February 2040.

My personal TIPS ladder, until this week, ended with a 30-year TIPS I purchased back in 2011, with a still-sweet coupon rate of 2.125%. I wanted to extend that ladder by one final issue.

I had looked earlier in the day on Wednesday and found nothing I could snag above 2.0%. But I checked again Wednesday afternoon and noticed that CUSIP 912810RA8, which matures Feb. 15, 2043, was being offered with a real yield to maturity of 2.02% for my investment of $10,000. So … I bought it. This chart shows why I thought a 20-year real yield above 2.0% looked historically attractive:

This chart ends on Nov. 9, 2022, but does not reflect the slightly above-market yield of CUSIP 912810RA8.

Let’s look at CUSIP 912810RA8

The originating auction for this 30-year TIPS was on Feb. 21, 2013, and yes, I wrote a preview article about that auction. (I’ve been at this a long time.) I wasn’t too impressed. Even then I was worried if I would live long enough for the TIPS to reach maturity:

“My strategy with TIPS is to buy them and hold them to maturity. I don’t ever look at their prices on the secondary market, I don’t care. Viewed this way, TIPS are a very conservative, very predictable, and very boring investment. The problem with a 30-year TIPS is: Will I live long enough to see it mature? I am 59. I could live to 89.”

Oh, to be young again. Now I am 69, and looking at very same TIPS. My biggest problem back in 2013 was that the Federal Reserve had launched into quantitative easing, forcing Treasury yields lower. I noted that real yields at that point — around 0.60% — were historically low, which is not good for a very long-term investment. From my 2013 preview article:

“Someday – maybe soon, or maybe not – 30-year TIPS will again be yielding 1.5%, or 2%, or more. When that day comes, the secondary-market value of a long-term TIPS yielding 0.6% is going to be crushed.”

Zoom forward to November 2022. Now, finally, the real yield to maturity for this TIPS — at least on Wednesday — had finally broken the 2.0% barrier, reaching 2.02%. The original investors in CUSIP 912810RA8 had indeed taken a beating. The original auction got a real yield to maturity of 0.639%, setting the coupon rate at 0.625%. Investors paid an unadjusted price of $99.62 for $100 of par value. On Wednesday, this TIPS was selling on the secondary market with a price of $76.73, down 23% from the original purchase price.

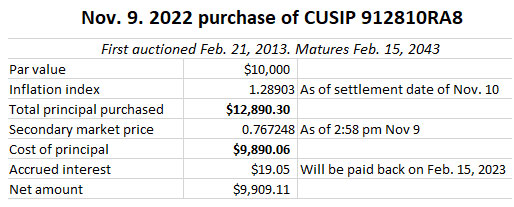

Now, let’s look at the basics of my purchase of $10,000 of par value in this TIPS:

This purchase at Vanguard (in a traditional IRA account) incurred zero commissions.

Note that I purchased $12,890 in principal in this TIPS for just $9,890. That means I paid below the par value of $10,000, which is guaranteed to be returned at maturity, even if severe deflation sets in. (I consider this more of an oddity that a true issue.) But more importantly, note that the original purchaser of this TIPS had accumulated $2,890 of inflation accruals, but the rise in the real yield from the original coupon rate of 0.625% to Wednesday’s real yield of 2.02% had wiped out that entire inflation accrual. Of course, the holder of this TIPS had collected a coupon rate of 0.625% along the way, but losing your entire inflation accrual is … painful.

This is a reason I am definitely not a fan of long-term Treasurys of any type, unless the nominal or real yields are historically attractive. And this TIPS investment could end up biting me if real yields continue climbing to 3% or 4%. But … no problem, I am holding to maturity, if I live that long.

Did I luck out?

Who knows, but Thursday’s weaker-than-expected inflation report has sent Treasury yields plummeting. As of the market close Thursday, CUSIP 912810RA8 was trading with a real yield of 1.83%, down about 19 basis points in one day, and its price was about $79.69 for $100 of value, about 3.8% higher than the price I paid. But … who cares? I really do intend to hold this to maturity.

The secondary market for TIPS is complex and if you intend to dip in with purchases, you need to understand the basics of any purchase … par value, inflation index, market price, accrued interest. I hope this article will help.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I still own BND as a core fund in a retirement account, despite the poor performance. The SEC yield can…