(And here’s the esoteric and confusing way that is calculated)

By David Enna, Tipswatch.com

August 11, 2021 update: The July inflation report keeps the COLA on track for an increase of about 6%

Inflation trends through June 2021 make it look likely that next year’s cost-of-living adjustment for Social Security beneficiaries could fall into a range of 5.8% to 6.2% for 2022, the highest increase since a 7.4% bump in 1982. But if inflation continues at its current torrid pace, the COLA could be even higher.

The Social Security Administration’s COLA formula is ridiculously complex and little understood. Is it related to U.S. inflation? Yes, but not the inflation index you hear about each month. Does it reflect 12 months of U.S. inflation? Not really. Does it underestimate actual U.S. inflation? Most years, yes.

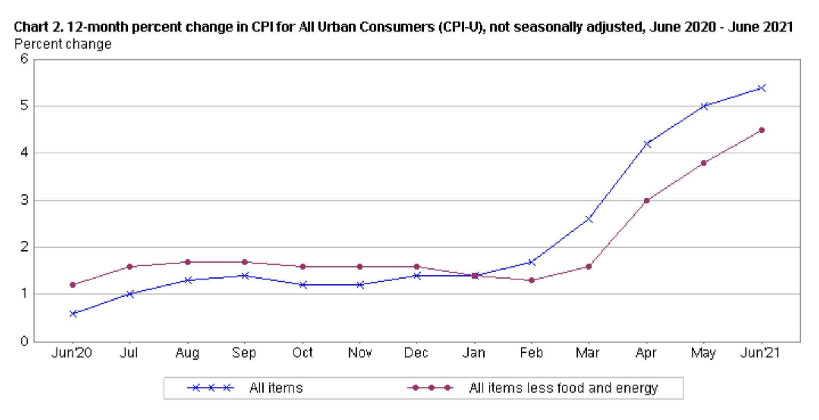

U.S. inflation (measured by CPI-U) is running at 5.4% as of June, but the Social Security Administration doesn’t use CPI-U. Instead, it uses the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). For that index, the June annual increase was actually higher, at 6.1%.

You are going to see that number — 6.1% — used often as the projection for the Social Security COLA in 2022. It is the current estimate of the Senior Citizen’s League, a credible advocacy group. It looks to me to be a reasonable projection, but at this point, the COLA’s complex formula makes things iffy. Let’s take a look at how the COLA comes together …

The Index

CPI-W includes data only from households with at least 50% of income coming from clerical or wage-paying jobs. I’ve noted in the past that CPI-W generally lags slightly behind CPI-U, which means the Social Security COLA also generally lags behind the standard measure of U.S. inflation. This year, at least through June, it is running higher than official inflation.

CPI-W isn’t widely tracked or reported, but the Bureau of Labor Statistics updates the index each month in its overall inflation report. Right now, you could say, “Well, CPI-W is running at an annual rate of 6.1%, so that will likely be the COLA increase for 2020.” But that’s not true. In fact, the June number isn’t necessarily an accurate indicator, as shown in this chart:

June sets the baseline for the COLA increase, but then we come to …

The Formula

The SSA doesn’t look at a full year’s data to determine the COLA. Instead it uses the average CPI-W index for the third quarter — July, August and September. Here is the language from the SSA site:

A COLA effective for December of the current year is equal to the percentage increase (if any) in the average CPI-W for the third quarter of the current year over the average for the third quarter of the last year in which a COLA became effective. If there is an increase, it must be rounded to the nearest tenth of one percent. If there is no increase, or if the rounded increase is zero, there is no COLA.

This wording means that the SSA eliminates years where inflation was zero or negative, and so there isn’t a “bounce-up” effect on benefits after a year of deflation. Instead, it goes back to the last year where there was an increase in benefits. But that won’t matter in this 2022 calculation, because the COLA rose 1.3% last year.

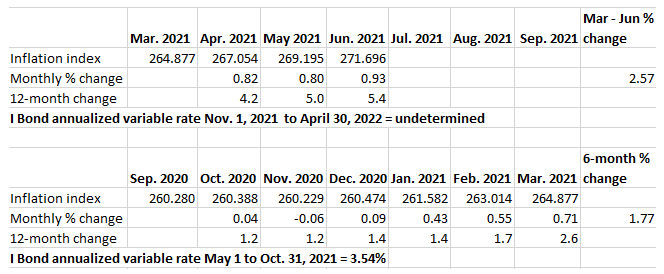

So, although 12-month CPI-W was up 6.1% in June, that number is only the baseline for the 2022 COLA increase. The only inflation numbers that will matter are for the third quarter: July, August and September. Last year, the CPI-W index averaged 253.412 in the third quarter. The June 2021 index was set at 266.412, or 5.1% higher than that average. So if we have zero inflation in the third quarter of 2021, the Social Security COLA be set at 5.1%.

U.S. inflation can be stubbornly finicky in the summer months, so predicting inflation from July to September is an impossible task. Hurricanes, gas shortages, food crop failures, stock market plunges, supply shortages, pandemic resurgence, etc., etc. It’s a guessing game, and nearly every summer brings some surprises.

Projecting the 2022 COLA

At this point, CPI-W is running at 6.1% over the last year, so you’d expect a continued inflationary trend of about 0.5% a month in July, August or September. But what if inflation dips after the multi-month surge so far in 2021? Could it run at 0.0% for three months? Doesn’t seem likely. But what about 0.4% a month? That seems possible.

Let’s take a look at how differences in 3rd-quarter inflation would alter the 2022 COLA:

My thinking is that after months of red-hot U.S. inflation, we could see things cool off a bit this summer. Used car prices aren’t likely to continue surging at a 45% annual pace, for example. Even air fares and hotel costs could slip if pandemic fears keep brewing. But other effects — gasoline and food costs, for example, and a possible spending surge caused by the new child care tax credit — could keep inflation rising a brisk pace.

Another factor is that CPI-W had a mild surge last summer, rising 0.6% in July and then 0.4% in August and 0.2% in September. That will make those numbers a bit harder to top than the June 2020 index, which was up 6.1% in June 2021.

So, if you think that CPI-W inflation will rise on average 0.3% a month in the 3rd quarter, you’d end up with a 5.8% COLA increase in 2022. If the average rises to 0.4%, the COLA would be 6.0% and if it rises to 0.5%, 6.2%. I think those are the most likely results, as I have shown in the chart.

That leads me to project that the 2022 Social Security COLA will fall into a range of 5.8% to 6.2%, and so let’s just go with 6.0% as most likely number.

Where can this go wrong? The stock market was taking a pummeling today, and two things also happened: Crude oil prices dipped sharply (down more than 7% today) and the U.S. dollar is getting stronger (up about 1.2% in the last month). Lower oil prices and a stronger dollar could dampen inflation over the next few months. Summer = market volatility.

What this means for Social Security recipients

The Social Security Administration currently estimates that the average retired beneficiary receives $1,555.25 a month, so a 6% increase would boost that monthly payment to about $1,648.56, an increase of $93.31 a month. If you are in the Social Security “limbo” period — older than 62 but not yet taking benefits — your future benefits would also climb by this percentage.

However, recipients can also expect that Medicare Part B costs will rise in 2022, which will subtract — at least partly — from the higher benefits. The base premium is now $148.50 a month. I could see that rising to $158 a month, cutting the effect of the COLA increase by $9.50 a month. But this is just speculation.

We won’t know the actual COLA number until 8:30 a.m. EDT on October 13, 2021, when the Bureau of Labor Statistics releases the September inflation report and completes the data needed for the 3rd quarter average of CPI-W. I will be tracking these numbers for July, August and September as each inflation report is issued.

I keep a running total of the CPI-W changes on my Social Security COLA page.

One more thing. One interesting side issue is that a 6% increase in benefits in 2022 could speed up Social Security’s path toward depleting its “trust fund” of accumulated payroll taxes. Once that happens, possibly in the early 2030s, Social Security will need to rely on incoming payroll taxes, which could cover only about 75% of projected benefits. Congress could — and should — address this issue quickly by gradually raising the full retirement age, or raising the income cap on payroll taxes, or taxing 100% — instead of 85% — of Social Security benefits for wealthy beneficiaries. Or some combination. We’ll see.

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Real and nominal yields tend to move together, higher or lower. In the same direction, but not necessarily by the…