By David Enna, Tipswatch.com

A new research paper by a Marquette University professor found that Series I Savings Bonds created annual returns substantially higher than high-yield savings accounts (HYSAs) between 1999 and April 2026.

The emeritus professor, Dr. David Krause, is the founding director of the university’s Applied Investment Management program. His academic focus encompasses investments, economics, statistics, and financial technology.

Krause’s paper is titled “High-Yield Savings Accounts vs. Series I Bonds: Which Is Better for Beating Inflation?” You can download a .pdf version here. This is from the abstract:

The historical analysis reveals that I Bonds delivered an average annualized real return of positive 0.83% over the 27 year sample period, while HYSAs delivered a negative 0.91% real return. …

I conclude that for investors with a holding period of at least one year, I Bonds offer a superior structural hedge against inflation compared to HYSAs. The $10,000 annual purchase limit remains the primary constraint for larger portfolios.

Krause notes that as of April 2026, U.S. inflation was running at 3.8%, but the national average interest rate on a standard savings account was just 0.38%. In response, many savers are turning to I Bonds and HYSAs to safely boost returns.

What is an HYSA? High Yield Savings Accounts are deposit accounts offered primarily by online banks and credit unions, Krause notes. They provide significantly higher annual percentage yields than savings accounts at traditional banks.

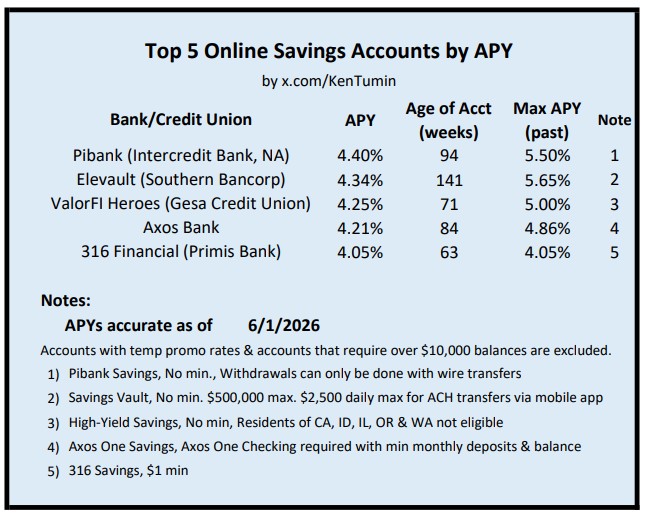

The Federal Reserve does not track HYSA rates, and data for years past are slim, so Krause created a “proxy” using an adjustment to the 1-year Treasury bill rate, currently 3.88%. Compare that to best-in-nation HYSAs at around 4.0%. Ken Tumin, who tracks savings yields on this site, posted this chart recently on X.com:

These best-in-nation yields are unusual, however, and note the declines from recent highs. A credit union where I have an account currently offers an HYSA with a yield of 3.2%. Similar products are Vanguard’s Cash Plus account at 3.35% or Fidelity’s Cash Management account with a money market fund yielding 3.29%. Tumin has noted:

Krause writes:

As of May 2026, top tier HYSAs offer APYs between 4.0% and 4.1%. However, these rates are variable and change at the discretion of the issuing institution. Unlike I Bonds, HYSA rates have no direct contractual link to inflation. They may fall even as inflation rises, a phenomenon observed during the 1970s and again during the post 2008 period. …

My central finding is that while HYSAs offer superior liquidity, I Bonds provide a superior structural hedge against inflation.

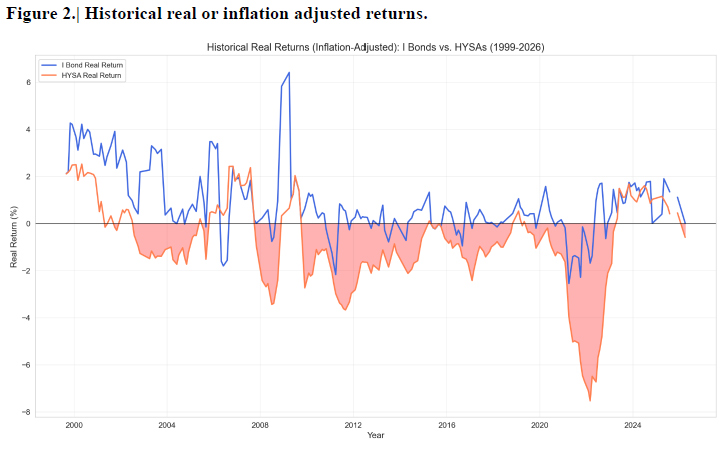

Here is a key illustration from the Krause study, showing a comparison of above-inflation returns for I Bonds versus HYSAs:

Krause’s research showed that I Bonds offered substantially better returns — and better protection against inflation — than HYSAs over the 27-year period.

I Bonds delivered positive real returns in 239 of 310 months, which represents 77.1% of the sample period. The average annualized real return was positive 0.83%. Even during challenging periods such as the 2008 financial crisis and the 2022 inflation spike, I Bonds maintained positive or only slightly negative real returns due to their inflation linked variable rate and the principal floor.

HYSAs delivered positive real returns in only 99 of 310 months, which represents just 31.9% of the sample period. The average annualized real return was negative 0.91%. HYSA real returns turned negative during every significant inflation acceleration. These periods included 2000 to 2001, 2005 to 2006, 2008 briefly, 2011, and most dramatically in 2021 to 2023. At the trough of the 2022 inflation spike, HYSA real returns fell to negative 0.61% on a monthly basis.

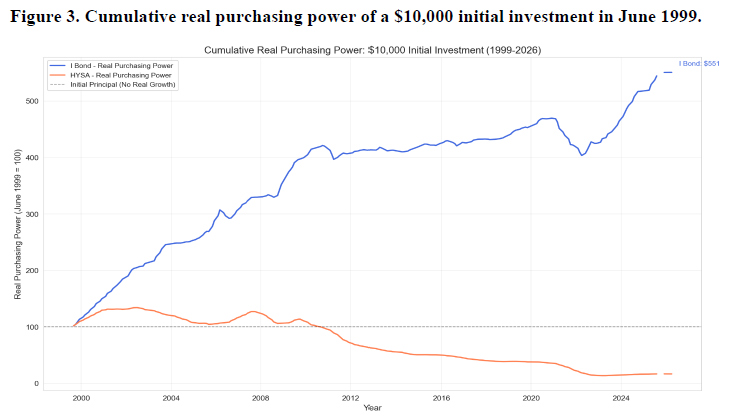

And here is another important illustration from the study:

Keep in mind that the chart shows the effect of inflation on purchasing power, so these are inflation-adjusted returns, not nominal returns. Krause points out:

In nominal or non-inflation adjusted terms, both investments grew. However, inflation eroded the HYSA purchasing power below its initial level. The I Bond, by contrast, preserved and modestly enhanced purchasing power despite two severe inflation shocks in 2008 and 2022 and a prolonged period of near zero interest rates from 2010 to 2021.

Liquidity and Penalty Considerations

Krause looked at the early-withdrawal penalty for I Bonds and found that early redemption substantially reduced the one-year real return, down to 0.19% versus 0.87% for current I Bonds held five years.

This finding suggests that I Bonds are best suited for funds that can be committed for at least two to three years. For true emergency funds requiring immediate access, a HYSA may be more appropriate despite its lower expected return.

Conclusion

As noted in the comments section, Krause’s proxy for past HYSA yields seems to underestimate top-of-market yields and instead tracks closer to “more typical” yields offered online and at banks and credit unions. But I think his conclusions are sound.

Krause notes that “I Bonds have historically provided superior inflation protection compared to HYSAs.” That trend, Krause believes, will continue into future years:

This advantage is projected to continue based on forward looking scenario analysis. The mechanism is clear. I Bonds have a direct contractual link to the Consumer Price Index through their variable rate. HYSAs depend on the monetary policy transmission mechanism, which introduces lags and uncertainty.

The fixed rate component of I Bonds is particularly valuable. Currently at 0.90%, it guarantees a positive real return regardless of inflation before accounting for taxes. HYSAs offer no such guarantee.

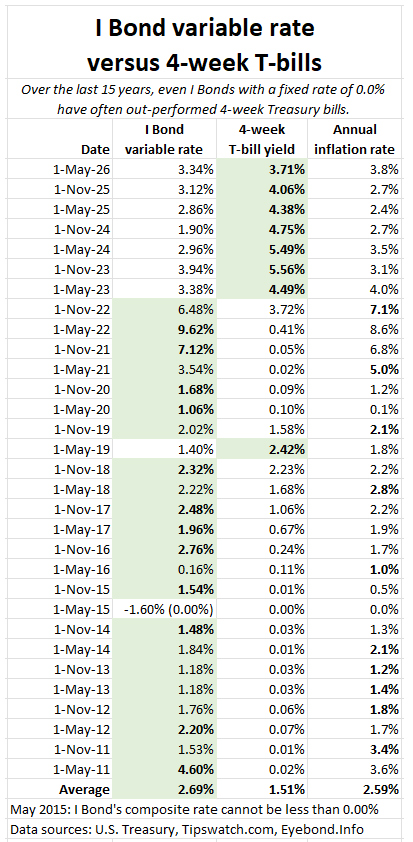

I Bonds versus 4-week T-bills

I am definitely not an academic researcher, but I did get a small mention in Krause’s paper. In my case, I have been tracking the performance of the I Bond’s variable rate (minus any fixed-rate adjustment) versus the returns of 4-week Treasury bills.

The pure variable-rate yield is reflected in I Bonds with a 0.0% fixed rate. Those aren’t highly attractive these days, with the fixed rate now set at 0.9% and looking likely to rise higher at the November 1 reset.

Here is how this performance stacks up, looking ONLY at the I Bond’s variable rate versus the then-current 4-week T-bill yield.

Even without the effect of any fixed rate, I Bond yields on average have surpassed both 4-week T-bill yields and the U.S. inflation rate since 2011. Why did this happen? Because for many years after 2011 the Federal Reserve held short-term interest rates well below the U.S. inflation rate (a trend that has now returned). The April 2026 inflation rate of 3.8% is shown in the chart, and May’s annual rate is expected to be higher. We will get the May 2026 report Wednesday morning.

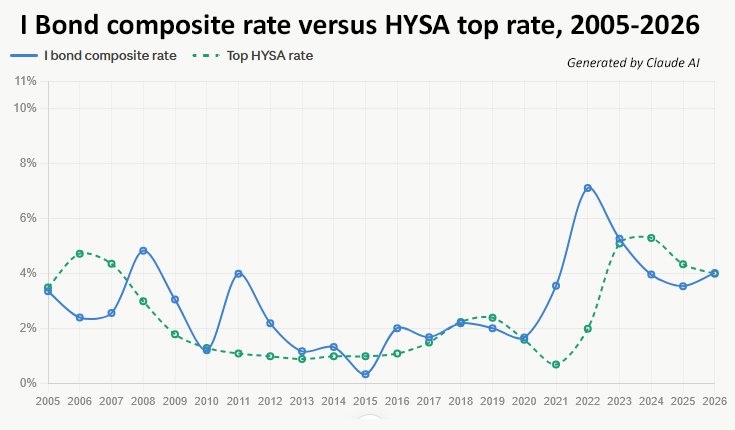

Add in the fixed rate, and obviously the performance becomes much better. For example, the current six-month composite rate is 4.26%, much better than the 4-week’s nominal yield of 3.71%. Here is a chart generated by Claude AI that compares the I Bond’s composite rate versus the top HYSA rate over the last 20 years:

This was my query to Claude: “How do returns of Series I savings bonds compare with HYSAs over the last 20 years?” There are times of I Bond under-performance, but those are minimal compared to strong out-performance by I Bonds during inflationary surges. This was Claude’s closing commentary:

I bonds have been a better deal in high-inflation environments (2021–2022) and when the Fed keeps rates near zero. HYSAs shine when the Fed is in a tightening cycle and inflation is cooling. Right now they’re close enough that the decision really comes down to whether you need the liquidity.

Final thoughts

I Bonds purchased today offer the advantage of a guaranteed 0.9% return above U.S. inflation, for as long as you hold the bond. High-yield savings accounts could surpass inflation, but there is no guarantee. And the interest rate could fall if market trends send short-term rates lower.

There is a use for both investments. I Bonds work well for holdings of five years or longer and T-bills and HYSAs for short-term cash needs. Krause notes:

For the retail investor asking which is better for beating inflation, the historical and forecast evidence points clearly to Series I Savings Bonds.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

—————————

Donate? This site is free and I hope to keep it that way. Some readers have suggested having a way to contribute. I welcome donations, any amount. And FYI, ads on this site pay for about one visit to Costco.

—————————

Follow Tipswatch on X for updates on daily Treasury auctions and real yield trends (when I am not traveling).

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades. NOTE: Comment threads can only be three responses deep. If you see that you cannot respond, create a new comment and reference the topic.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

For the patient folks – the November I-Bond fixed rate reset is promising to be higher than 0.9%. As of right now it would move to 1.0%. But the trend on DFII5 continues upward…

Hi David, I’m still working on ways of minimizing the upcoming tax bomb for my 1998-2001 I-Bonds. One minor tweak I’m planning is to redeem and transfer some of them in 2026 to 2027 and to purchase new I-Bonds that I don’t plan to redeem until 2032, after the tax bomb has passed. The interest on those new I-Bonds will be deferred until 2032 when I’ll be back in the 12% (15% by then) tax bracket rather than the 22% (25%) tax bracket if I was earning any other kind of interest from 2028 to 2031 that isn’t tax-deferred.

There is a practical floor to HYSA rates which are going to be higher than short term T bill rates, though. It may not be the 1% of T Mobile Money but is not going to be 0.01%. Ally, Alliant, Live Oak Bank, etc. all settled around 0.50% as I recall.

This seems correct because when I wrote that T-Mobile Money article in June 2021, the 4-week Treasury bill was yielding 0.01%, and so was the Vanguard Treasury Money Market. But several online banks had offerings at 0.50% at that time.

Thank you for including a disclaimer that the final chart was generated by AI. But when using AI, I think it would help the reader to include an explanation of the prompt / process for generating the chart, so readers can better understand its credibility In other words, was the underlying data determined by the user (you) elsewhere and then provided to the AI to merely generate a chart, or did the user’s prompt request the AI to gather the data, perhaps undermining credibility?

As marce607c0220f7 points out, the Kruase report may rely on an unreliable assumption about HYSA rates. The AI generated chart might have used different underlying data for the HYSA rate compared to the Krause report, but the reader is unable to assess the reliability of the chart without an explanation of methodology.

This was my query to Claude: “How do returns of Series I savings bonds compare with HYSAs over the last 20 years?” Claude attempted to show the “top” HYSA rate, and I think Krause’s proxy formula was (possibly inadvertently) pointing at “typical” HYSA rates. Try the search in Claude; it provides an interesting analysis. Here was the final conclusion:

The last 20 years were “odd” because of many years of interest-rate repression by the Federal Reserve, even when inflation was well above zero. Plus we had a two-year climb to the highest inflation rate in 40 years. Because of those two factors, I Bonds outperformed. I don’t know if we will see those factors again, but I want the insurance of inflation protection.

Do you think Claude used the Tipswatch site as a source for its analysis?

Robt, In this case, I don’t think so. But most times when you ask about TIPS or I Bonds, Claude and ChapGPT refer to this site.

I would enjoy a historical comparison of the performance of 5 Year TIPS, 5-Year T-Notes, and I Bonds (after the 5 year penalty disappears). That would be an interesting apples to apples comparison from a term perspective.

You can see a comparison of 5-year TIPS and 5-year notes on my TIPS Vs Nominals page. (Also 10-year TIPS versus 10-year notes.) I write an article at each maturity, such as this one for the 5-year TIPS that matured in April. In that case, I Bonds were the winner.

Excellent! Thank you.

At the very least they could index the maximum yearly purchase amount to inflation. That would still help middle income folks. I’ll let the very wealthy deal with their own problems.

I’d be curious if the comparison included SGOV and MMF ETFs as a happy medium between returns and the accessibility of a HYSA.

Good article. VUSFX (and even better VWSUX) are much better than HYSA.

Just for comparison, SGOV has had an annual total return of 3.54% over the last five years, which might include some capital appreciation. Inflation has averaged 4.5% over that period.

For VUSFX, the total annual return over those 5 years was 3.41%. For VWSUX it was 2.31%, tax-exempt.

Spoonfeeding is so passe! With all do-gooders, ibond gifts for younger individuals for college, etc. may also be curtailed…so much for easy college financing for relatives for the future! And, as noted before, “transfers” will (continue) be permitted. The latter is a more convoluted process but if one wanted to eliminate the gift box “they” should also be attacking the “transfer” portal! And, TD allows multiple trusts and multiple accounts for legit sole proprietorships!

Krause’s HYSA “proxy” appears to be suspect. I glanced through the rates I’ve recorded each month for our Barclay’s account (opened in 2014) and quickly compared them to the orange HYSA proxy line in his Figure 1 graphic.

My records show rates from 0.9% to 1.0% when his proxy is on the “floor”* of 0.01% through 2014 and 2015. Likewise for the year 2020, I recorded Barclay’s rates falling from 1.7% to 0.45% while he again shows the HYSA proxy at 0.01%.

So, it would seem the I Bond’s (presumed) advantage over HYSA’s might be significantly less than Krause claims. All that said, I’m still buying and/or rolling over I Bonds to improve the fixed rates in our portfolio.

* “Values are floored at 0.01% to reflect the practical reality that banks rarely reduce savings rates to zero.”, Section 3.2 paragraph 3.

Hmm. I see David’s “I Bond composite rate versus HYSA top rate” graphic echo’s my observation concerning historic HYSA rates.

Note to self: read first, then comment. ; )

I also found the proxy rates to look odd but I have never followed HYSA statistics. I would “think” these accounts might track closely with the 13-week T-bill rate, which right now is 3.78%. (My credit union is offering less.) Banks do offer “promo” rates to pull in customers and some probably use these accounts to keep customers in-house. In June 2021, I wrote about T-Mobile Bank offering 1% on cash, which at the time looked “outrageously” high. At that time HYSAs were paying 0.5%, at tops, on promo deals. Vanguard Money Market was paying 0.01% (same as the 4-week T-bill), so realistically that is probably where most savings accounts were falling. I Bonds had a composite rate of 3.54%, a huge advantage.

A study of the real returns over these long time periods of the I-Bonds vs. the TIP bonds would perhaps be even more useful.

I see mentioned that for I-bonds held short term, after the early withdrawal penalty is deducted, there is very little difference in the returns of a high yield savings account (with less hoops than inside the Treasury account).

That was my first thought. Longterm, of course I-Bonds would be much better than a high-yield savings account, especially with a fixed rate on the bond. However, if it can’t be held for at least a couple of years, then the penalty brings it right back down (or even lower) than the savings account. The main thing is liquidity. If you’re going to use/need it within 36 months, then you might as well keep it in savings. The main thing is investing in something at least equal to or greater than inflation. Otherwise it’s no different than plaque on teeth or termites on wood. The value literally gets eaten away.

Problem is the limited purchase amount on I bonds, so its not really a game changer and more trouble than its worth. When the limit higher years ago didnt have the money. Now I got the money but purchase limit is too low to hassel with TD myself and heirs. So thus study has very little value IMHO.

You’d think they would at least link the limit to inflation!

Well, it does say “academic” so my expectation of its usefulness was pretty low… Bessent seems to be a pretty smart guy, I can’t understand why they don’t increase the amounts people can invest and more importantly come up with a better website interface to buy and track your positions. Something as easy as buying/selling/redeeming like Schwab or Fidelity. Crazy.

They don’t increase the amount you can invest because they don’t care about meeting the needs of wealthy investors. The program is designed to meet the needs of middle income households. They also want to limit the expense during periods of high inflation, if wealthy investors loaded up that would significantly increase government expense. There is also lobbying pressure from the financial industry to keep the program restricted so they don’t have to compete with a risk-free, tax-deferred, inflation protected product offered by the Government. They also want to prevent the administrative burden of handling millions of larger accounts and customer service queries. You may have seen when the system crashed in 2022. They are in the process of improving the website interface so it’s more similar to a brokerage account , but it is taking way longer than it should

Agree TD is a nightmare. I still have a hard time finding my converted bonds. And not sending out a 1099 when stuff matures, is just an insult.

This comes up often, and it is true that 25 years ago you could buy a lot more in I-Bonds than you can today. However, it’s not hard to increase the limit of $10,000 per SSN, $20,000 per couple. It took an hour with Nolo Willmaker software to create revocable living trusts, $7 each with a Notary Republic and now you have a total of $40,000 per year per couple. Then you have the gift box loophole, which will rumored to close, is still open. That allows you to purchase gifts for your spouse, for example, and vice-versa, again expanding the purchase limit (we purchased $120,000 in a month this way a few years back). All of this is subject to what folks want or don’t want to do, but if you want to accumulate I-Bonds, you surely can.

How do you define wealthy? Comparing I bonds, a long term strategy to a short term High Yield account is ridiculous, since they serve a different purpose. Different liquidity too! You just created yourself an TD estate nightmare, since TD only allows joint type accounts, with no beneficiaries, outside of the trust. Good luck when your brain turns to mush and someone has to figure out all those account through probate court. I re balanced and 80% cash now of my liquid money. Would take me about 10+ yrs even using your strategy to deploy cash, being 76 that would be ridicules. MM as good as any waiting for the next shoe to drop on our nation. And you will bet those of us with lots of cash will clean up. Even during periods no rates, I held cash and clean up when a crash comes.

I responded to your original post, which was all about the contribution limit issues.You can easily get around that limit and I provided examples – there is, effectively, no practical limit at this time with the gift box. I’m not sure what estate nightmare you are referring to, my spouse and I each have 1 revocable trust with beneficiary designations for trust assets. I’m 20+ years younger than you, so Lord willing, my brain turning to mush will not happen any time soon.

For an asset with a flexible redemption of between 1-30 years, one can easily replace the need for a high yield savings account for at least some of their emergency funds – I know we have. We treat some of our I-Bonds (which we’ve been purchasing since 2007) as inflation protected cash that can be drawn upon if needed.

Perhaps your personal circumstances are different (and it seems they are based upon your follow up post), that’s fine, everyone makes their own choices best for their own circumstances.

The median American cash account balance (check, savings, money market) is $8,300. For the overwhelming majority of Americans, the annual limit is not just moot, it’s a financial goal far beyond attainment.

I hear statistics like this all the time but most of the people I know are living fairly comfortably. The cars I see on the highway are usually much nicer than my Corolla. The vacation theme parks are crammed with visitors.

The unique thing (and the great contradiction logically) about I Bonds is that they are most appropriate as an investment for higher middle class and lower wealthy class investors. This is about capital preservation, and if you don’t have capital, they don’t make a lot of sense. And if you are super rich, who cares? So the $10,000 purchase limit is a bit of a problem, except for investors willing to buy I Bonds over many years (as I have) or to use the work-arounds like the gift box and trusts.

Banks have never been a great place to keep your money. Banks look out for banks. They are quick to cut yields when interest rates are declining and very slow to raise them when interest rates are rising. Their investment platforms typically come with high fees and expense ratios. For me the main advantage of keeping money at a bank is to avoid monthly service charges for checking accounts and the like. Additionally you get hit with full taxation from any savings account at a bank, unlike I bonds which are exempt from state and local taxes.

I use credit unions for checking and savings due to lower fees and keep very little in those accounts.

Liquid near-term cash needs go in VUSXX at Vanguard (treasury money market fund, no state taxes). Emergency fund is in I bonds. Everything else is in the market, mostly in a 401k and Roth IRA. I use XDIV in my taxable brokerage to avoid dividend income.

I find this is a pretty good system. I used revocable living trusts to set up additional accounts at treasury direct to increase I bond purchase limits. BOXX also looks interesting for cash, but I haven’t bought it yet.