By David Enna, Tipswatch.com

This article is the fourth in a series looking at how my three favorite bond funds — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed after 2013, when the Fed signaled it would back off on bond purchases and eventually raise short-term interest rates.

Why do this? Because we may be heading into a similar scenario in 2022 and beyond, with the Fed tapering off bond purchases and eventually (and gradually) raising short-term interest rates. The performance after 2013 could tell us a lot about what’s ahead.

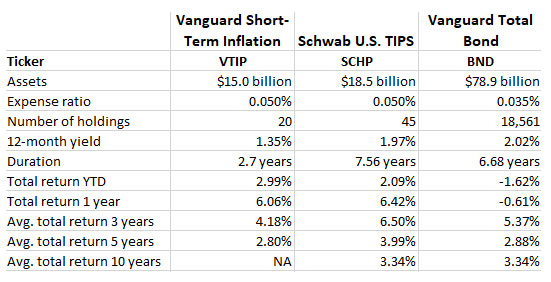

To recap, here are the three bond funds I am tracking; they are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a summary of their basic statistics and performance:

2016: Real yields fall, nominal yields rise. TIPS are the winner

In general, when nominal yields (like those on traditional Treasurys) rise and fall, real yields (like those on TIPS) follow pretty much along, separated by “the inflation breakeven rate” — the market’s expectation of future inflation. The exception occurs when inflation expectations change dramatically, and in 2016, that happened.

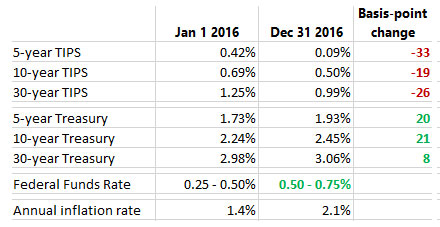

Official U.S. inflation had run at an annual rate of 1.5% in 2013, 0.8% in 2014 and 0.7% in 2015. But in 2016, surging gasoline prices (up 9% year over year) pushed official U.S. inflation up 2.1% for the year. Just like today, though, this surge in inflation partly resulted from weak prices a year earlier. Inflation had declined 0.1% in December 2015, ending that year at 0.7%.

Nevertheless, this surge in inflation seemed to justify the Federal Reserve’s intention to continue gradually increasing its federal funds rate, which rose 25 basis points on Dec. 14 to a range of 0.5 – 0.75%, the second of nine eventual rate increases. Here are the 2016 statistics:

At this point, remember, the Federal Reserve had ended its bond-buying quantitative easing efforts in October 2014. And even though real yields fell in 2016 for all maturities, TIPS still maintained a yield positive to inflation. (This is the sort of thing you see when the Federal Reserve has stopped manipulating the market. Ahh, nostalgia.)

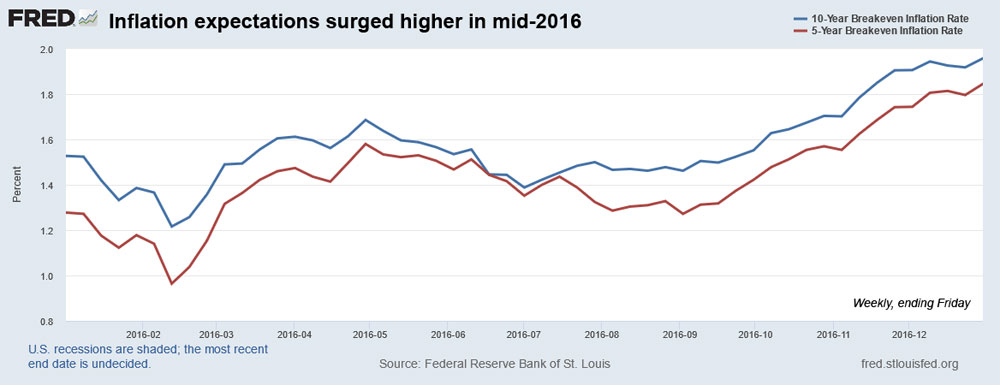

The divergence in yields — falling real yields and rising nominal yields — is directly related to inflation expectations. The market was pricing in higher future inflation, as can be seen clearly in this trend chart for 2016:

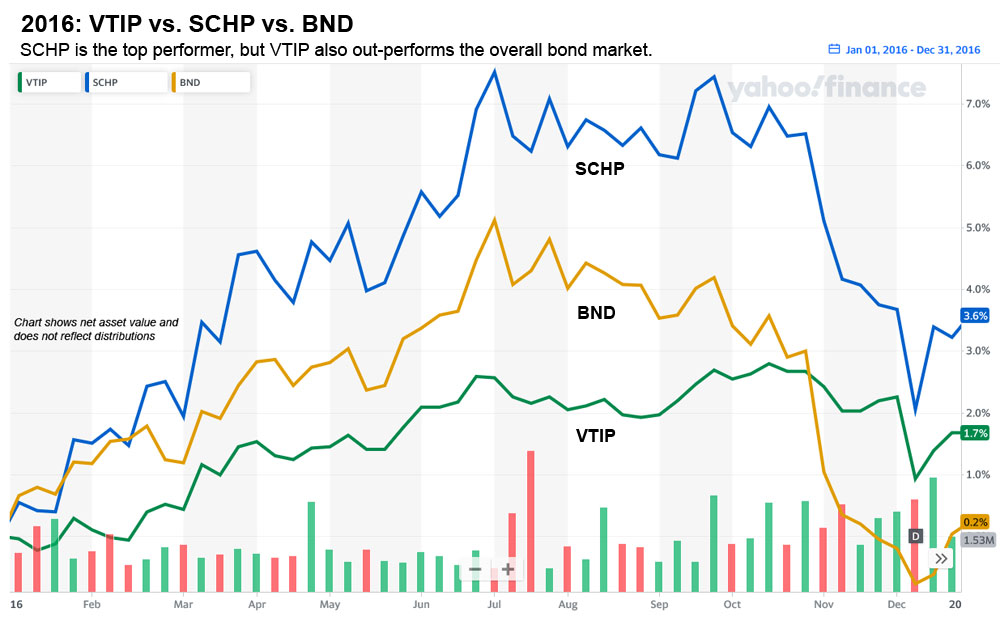

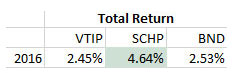

Under these conditions, you’d expect TIPS to out-perform nominal Treasurys, and they did. Here is how our three funds performed in 2016, with the chart showing changes in net asset value and not reflecting distributions:

Well into 2016, Schwab’s U.S. TIPS ETF (SCHP) was having a spectacular year, up 7% in net asset value. But all three bond funds took a clipping from October to November as it became clear the Federal Reserve would carry through with its plan for a December rate increase.

Again, net asset value can be a misleading measure of a bond fund’s performance because it does not reflect distributions. But SCHP was 2016’s clear winner, driven higher by 1) falling real yields and 2) higher inflation adjustments to principal. Both VTIP and BND also had respectable total returns of about 2.5%.

Conclusion

For bond investors, 2016 was a good year, even with the Federal Reserve carrying through with its well-signaled December 2016 increase in short-term interest rates. The divergence of yields — with real yields falling and nominal yields rising — gave the TIPS funds an advantage. In the years from 2013 to 2021, this was the year with the strongest divergence. We’ve seen something similar in 2020 and 2021, but not to this degree.

Coming tomorrow: A look back to 2017

- 2013: A year of surging real and nominal yields

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2017: ‘The calm before the storm’

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

This discussion raises in my mind what is the optimal amount of inflation bonds to hold in a diversified bond…