By David Enna, Tipswatch.com

This article is the fifth in a series looking at how my three favorite bond funds — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed after 2013, when the Fed signaled it would back off on bond purchases and eventually raise short-term interest rates.

Why do this? Because we may be heading into a similar scenario in 2022 and beyond, with the Fed tapering off bond purchases and eventually (and gradually) raising short-term interest rates. The performance after 2013 could tell us a lot about what’s ahead.

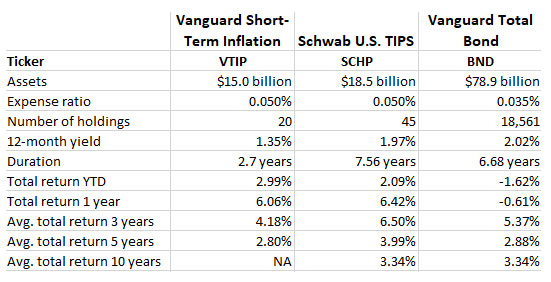

To recap, here are the three bond funds I am tracking; they are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a summary of their basic statistics and performance:

2017: ‘The calm before the storm’

Looking back, 2017 was the final year of relative bond market stability in the post-2013 era of “winding down quantitative easing.” This was despite three — yes three! — increases in the Federal Reserve’s key short-term interest rate. They came like this:

- March 17, 2017: Increase of 25 basis points to a range of 0.75 – 1.00%

- June 14, 2017: Increase of 25 basis points to a range of 1.00 – 1.25%

- December 13, 2017: Increase of 25 basis points to a range of 1.25 – 1.50%

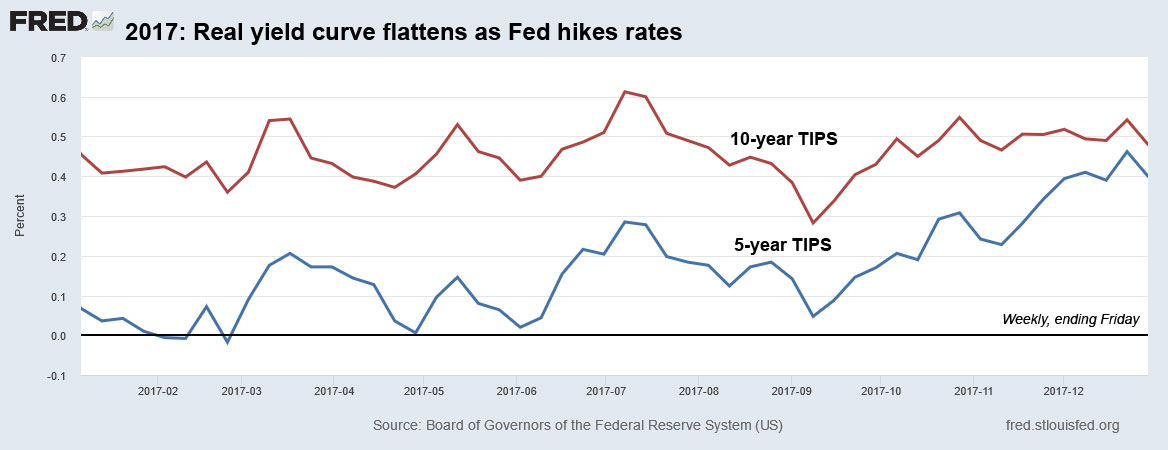

The result wasn’t a taper tantrum, like in 2013, but the bond market’s yield curve began to flatten, often considered an omen of economic recession. The theory is: Longer-term yields will rise along with short-term yields (which are set by the Fed) if the market sees solid economic growth in coming years. But the market in 2017 wasn’t seeing that, and its pessimism suppressed longer-term yields and led to a relatively benign year for the bond market.

Here was the year’s trend in 5- and 10-year real yields, which became dramatically tighter at the end of the year:

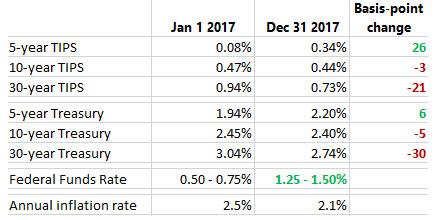

But really, very little happened in 2017. Yields across the board — nominal and real — stayed in attractive zones, with real yields solidly above zero and inflation breakeven rates running at a reasonable 2.0%. Here are the statistics for 2017:

Note that inflation ended 2017 at an annual rate of 2.1%, giving support to the Fed’s decision to gradually — and consistently — increase interest rates.

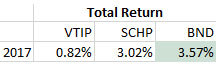

This was the beginning of a wonderful — and too brief — era when you could find money market accounts paying 1.5% and 5-year bank CDs paying up to 3%. It was also a year of relative peace in the bond market, even with Fed rate increases looming. This chart shows the trend in net asset value for our three funds, and although there was a lot of low-bore volatility, all three funds ended up for the year, even before distributions:

The flattening yield curve held down the potential of Vanguard’s short-term TIPS fund, VTIP. When you look at total return, the total bond market (represented by BND) performed the best, but SCHP also had a good year.

All of this was setting up a more dramatic bond market in 2018, when the Federal Reserve continued to raise interest rates … four times. While 2018 wasn’t a disastrous year, it broke a two-year trend of relative stability in the bond market.

Coming tomorrow: A look back at 2018

- 2013: A year of surging real and nominal yields

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2018: Did the Federal Reserve go too far?

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Why do you need a tips ETF when you can purchase tips directly from treasury direct?

In general, I’d prefer to buy individual TIPS at auction, and hold them to maturity. In the past, I made these purchases at Treasury Direct, but now I want to move those purchases to a traditional IRA brokerage account. A lot of investors — the great majority I’d expect — prefer to own the TIPS funds versus individual TIPS, for convenience and simplicity.