By David Enna, Tipswatch.com

This article is the sixth in a series looking at how my three favorite bond funds — Vanguard Short-Term Inflation Protected (VTIP), Schwab U.S. TIPS (SCHP) and Vanguard’s Total Bond (BND) — performed after 2013, when the Fed signaled it would back off on bond purchases and eventually raise short-term interest rates.

Why do this? Because we may be heading into a similar scenario in 2022 and beyond, with the Fed tapering bond purchases and eventually (and gradually) raising short-term interest rates. The performance after 2013 could tell us a lot about what’s ahead.

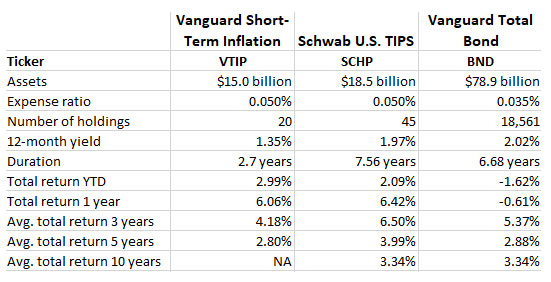

To recap, here are the three bond funds I am tracking; they are three conservative, liquid, mainstream bond funds with very low expense ratios. Here’s a summary of their basic statistics and performance:

2018: Did the Federal Reserve go too far?

Bond funds had a mediocre — but not disastrous — year in 2018, even with the Federal Reserve raising its key short-term interest rate, the federal funds rate, four times in the year. Here was the Fed’s rate-hiking schedule:

- March 21, 2018: Increase of 25 basis points, to a range of 1.50 – 1.75.%

- June 13, 2018: Increase of 25 basis points, to a range of 1.75 – 2.00%

- Sept. 26, 2018: Increase of 25 basis points, to a range of 2.00 – 2.25%

- Dec. 19, 2018: Increase of 25 basis points to a range of 2.25 – 2.50%

The December 19 increase was the last of a string of nine rate increases dating back to December 2015. At the time, a lot of financial experts (joined by a non-financial-expert U.S. president) criticized the final December increase as going too far, too fast. The financial markets went into a tailspin, as noted in this Dec. 20, 2018, report from The Guardian:

“The Dow Jones industrial average dropped 70 points after the announcement to finish the day down 1.49%, while the S&P 500 lost 39.2 points, or 1.54%. US stocks are on course for their biggest December decline since 1931, the depths of the Great Depression.

“The selling spread into Asian trade on Thursday, where the Nikkei in Tokyo was down 2.3% and the Hong Kong market was off 1.1%. In China, the Shanghai Composite was down 0.8%. …

“(President) Trump has waged a public campaign to halt further rate rises, a highly unusual move for a president, calling the increases ‘crazy’ and ‘foolish’ and arguing the Fed’s policy was’“the “biggest threat” to the US economy, larger than the administration’s trade dispute with China.’ “

The S&P 500 fell nearly 15% from December 1 to December 24 and ended the month down nearly 10%. Against that backdrop, the bond market looked relatively serene. Here are the statistics for 2018:

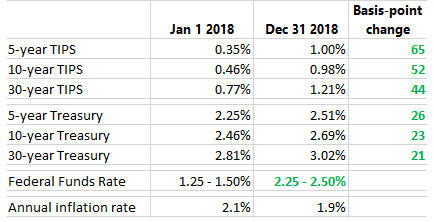

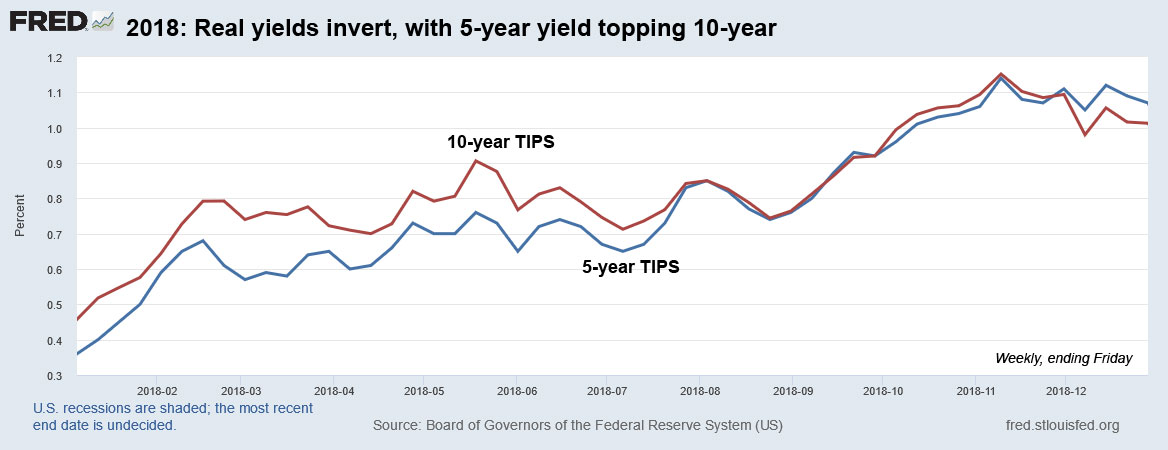

By the end of the year, the yield curve had completely flattened, screaming a warning of a future recession. On Dec. 31, the 4-week Treasury was yielding 2.44%, the 5-year, 2.51%, and the 10-year, 2.69%. Real yields had inverted, with the 5-year TIPS ending the year with a higher real yield than the 10-year, as this chart shows:

On Dec. 20, 2018, a 5-year TIPS reopening auction generated a real yield to maturity of 1.129%, the highest in nearly 10 years. That was one of the greatest auction bargains of the last decade. One year later, a TIPS reopening auction of the same term generated a real yield of just 0.02%.

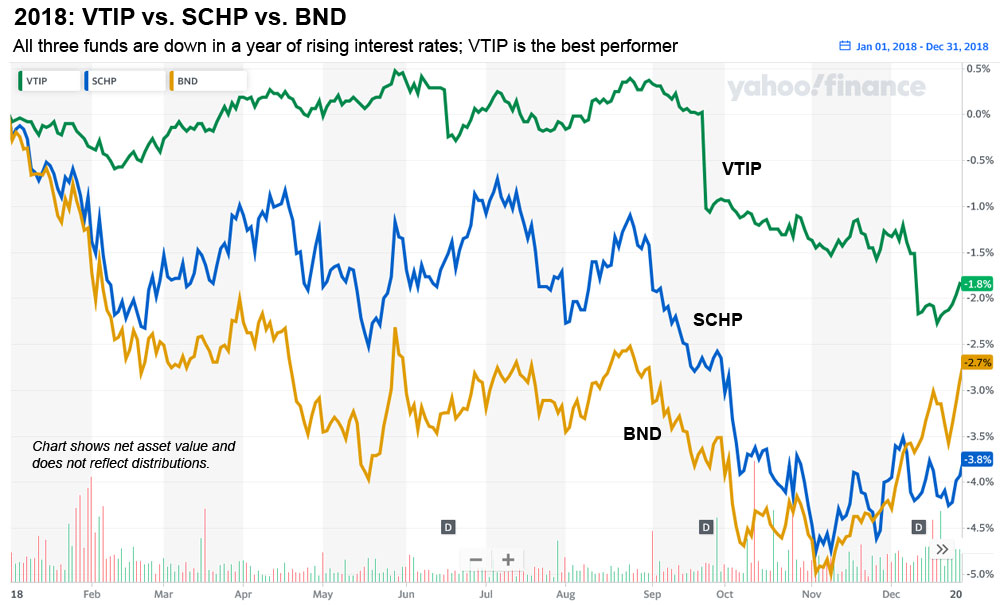

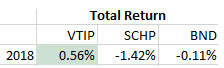

Amid all this rate-hiking fury, all three of our ETFs lost in net asset value in 2018, despite a gentle rally toward the end of the year. Here is the trend in net asset value, which does not reflect fund distributions:

Vanguard’s short-term TIPS fund, VTIP, ended up being the best performer in both net asset value and total return, generating a positive total return of 0.56% in 2018. Inflation in 2018 ran at 1.9%, enough to keep TIPS competitive. Still, Schwab’s U.S. TIPS ETF was the loser for the year. The total bond market was nearly flat, benefiting from nominal bond yields topping 2% across all maturities at the end of the year.

Conclusion

December 2018 was the peak of the Federal Reserve’s “non-accommodative” policy, after allowing short-term interest rates to top out at about 2.5%. The bond market flattened, but didn’t implode. It was the stock market’s harsh reaction that pushed the Fed into a corner. And just keep this in mind: The S&P 500’s total return declined only about 4.5% in 2018, after rising about 21.7% in 2017. Once again, my long-held theory proved true: The Fed will act to protect the stock market.

Coming tomorrow: A look back to 2019

- 2013: A year of surging real and nominal yields

- 2014: The deck was stacked against TIPS funds

- 2015: The Fed actually did something!

- 2016: Inflation rises; TIPS out-perform the overall bond market

- 2017: ‘The calm before the storm’

- 2019: The Fed cries ‘uncle’; bond investors celebrate

- 2020: Chaotic year of pandemic fears, stunning stimulus

- 2021 and beyond: What’s ahead for U.S. financial markets?

* * *

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Raise the rates. Kill the inflation. That's my opinion.