By David Enna, Tipswatch.com

The Treasury on Thursday will offer $20 billion in a reopened 5-year TIPS, CUSIP 91282CJH5, creating a 4-year, 10 month Treasury Inflation-Protected Security.

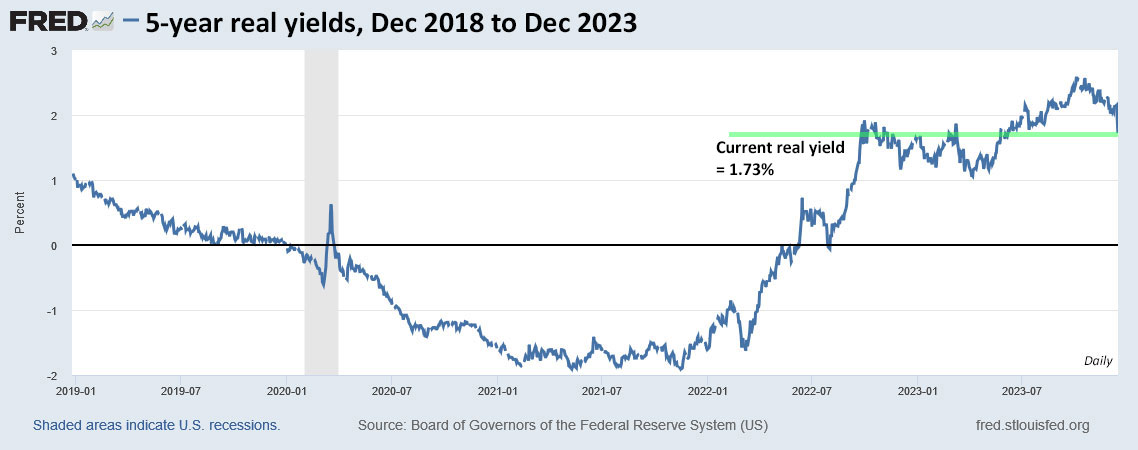

The TIPS to be reopened, CUSIP 91282CJH5, trades on the secondary market and could have been nabbed by investors just a month ago with a real yield to maturity of 2.37%. At Friday’s close, according to Bloomberg Yields Curve, that yield has now fallen to 1.73%. That’s a drop of 64 basis points in one month. Incredible.

And continued volatility is likely next week, right up to the auction’s close at 1 p.m. EST Thursday.

How attractive is this TIPS?

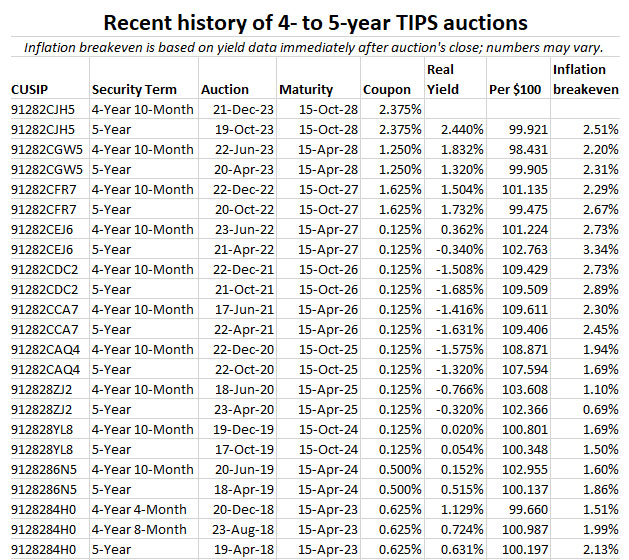

While a real yield of 1.73% seems suddenly disappointing, it is still attractive by historical standards. It could be the third or fourth highest yield for any auction of this term going back to October 2008, 48 auctions ago. Just look at the auction history for 5-year TIPS over the last year:

- Dec. 22, 2022, reopening, real yield of 1.504%

- April 20, 2023, new issue, real yield of 1.320%

- June 22, 2023, reopening, real yield of 1.832%

- Oct. 19, 2023, new issue, real yield of 2.440%

A real yield of 1.73% fits into this mix, but of course we’d all love to have bought heavily on Oct. 19 when the above-inflation yield hit 2.440%. (If you recall, this was actually a disappointing result for many investors. How times have changed!)

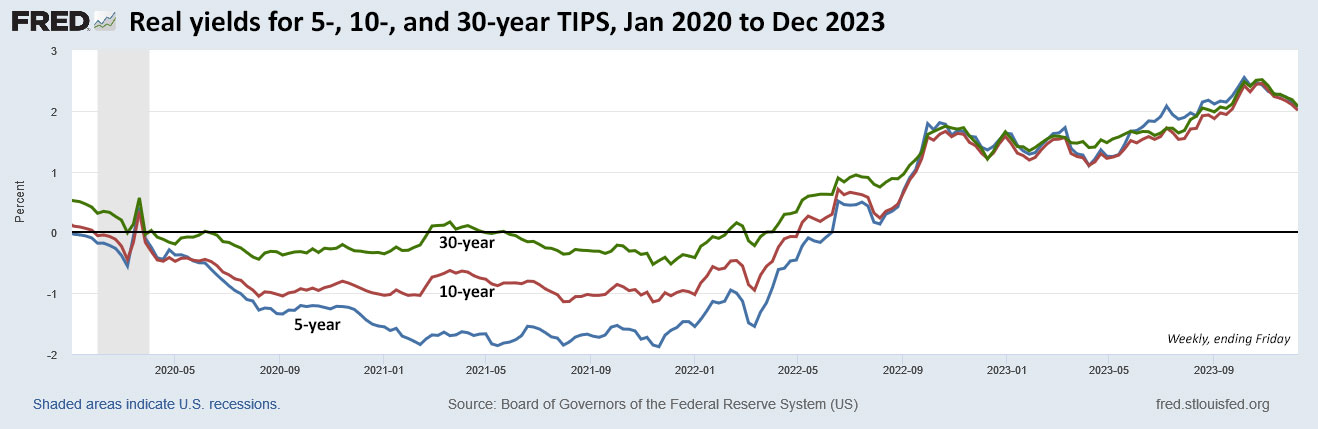

Here is the five-year trend in the 5-year real yield, showing that the current yield remains attractive by comparison to years of severely depressed rates:

Pricing for CUSIP 91282CJH5

If we assume that this TIPS will auction with a real yield of 1.73% (things will change, but let’s assume) then it will get a price of about 102.98, according to the Bloomberg data. Why so high? Because this TIPS has a coupon rate of 2.375% — set by that Oct. 19 auction — well above the current market real yield. It will also have an inflation index of 1.00453 on the settlement date of Dec. 29.

With that information, we can speculate on the pricing, using a purchase of $10,000 par as an example:

- Par value: $10,000.

- Adjusted principal on settlement date = $10,000 x 1.00453 = $10,045.30

- Cost of investment = $10,045.30 x 1.0298 = $10,344.65

- Plus, accrued interest, probably about $49.

So, in summary, an investor purchasing $10,000 par at Thursday’s auction will pay about $10,345 for $10,045 of principal and then receive inflation accruals and a coupon rate of 2.375% through the maturity date of Oct. 15, 2028.

This is a similar price to what you would pay on the secondary market, of course. On Saturday morning Vanguard was showing an ask price of 102.98 and a real yield of 1..73%, right in line with the Bloomberg data. But come Monday, things will change.

Inflation breakeven rate

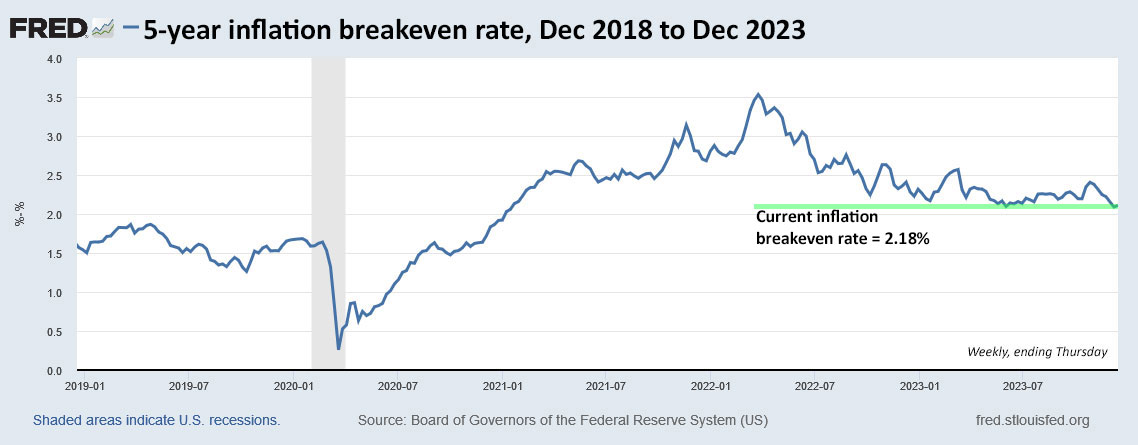

With a 5-year nominal Treasury yielding 3.91%, this TIPS currently has an inflation breakeven rate of 2.18%, well below recent auctions of this term. That is a plus for investors. It means this TIPS will outperform the nominal Treasury if inflation averages more than 2.18% over the next 4 years, 10 months. Over the last 5 years, inflation has averaged 4.0%.

Here is the trend in the 5-year inflation breakeven rate over the last five years:

Final thoughts

I won’t be a buyer because my TIPS ladder is fully loaded with 2028 maturities.

I know from feedback from readers that this particular TIPS won’t be attractive to many, either at auction or on the secondary market. Why? Because it will carry a premium price and additional principal. And a lot of investors don’t find that appealing. Does it really matter? Probably not. And sitting on the sidelines could just mean facing lower real yields in the near future. It’s a dilemma.

In the last two days, I have been tempted to say that the bond market is over-reacting to the Fed’s potential actions. The Fed, in theory, will cut short-term interest rates by 75 basis points next year. (The market thinks the cuts will be much more substantial.) The Fed is NOT launching quantitative easing and in fact will continue tightening through 2024 by reducing its balance sheet.

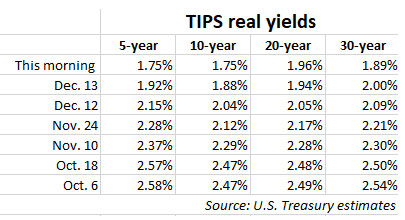

Future short-term rates shouldn’t have a great effect on current mid- to longer-term Treasurys. The 10-year TIPS yield has fallen 35 basis points in four days. Why? That is a real question for the markets to consider.

Plus, the Treasury next year will continue ramping up auction sizes. In fact, Thursday’s reopening auction is for $20 billion, the highest in history for an 5-year TIPS reopening. Consider this: As of this week, the U.S. public debt stood at $33.8 trillion. One year ago it was $31.3 trillion. That is an increase of 8%. How far can Treasury yields really fall?

So the Treasury market has a lot to work out. Meanwhile, I will be posting the auction results soon after the 1 p.m. ET close on Thursday. Here’s a history of recent auctions of this term:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

bdp453, it's not clear from your brief inquiry whether you are trying to learn the basic facts about TIAA Traditional,…