Despite a real yield deeply negative to inflation, CUSIP 912828UH1 outperformed a nominal 10-year Treasury.

By David Enna, Tipswatch.com

Sometimes what looks like a perfectly awful investment will end up surprising you. That is the case with CUSIP 912828UH1, a 10-year Treasury Inflation-Protected Security that had an originating auction on Jan. 24,2013. It matured Sunday, 10 years later. So how did it do as an investment?

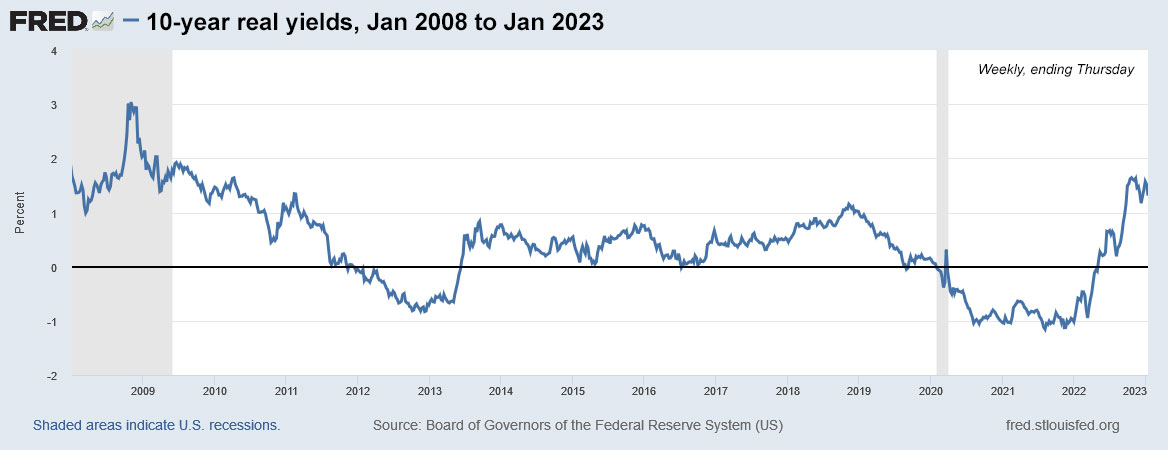

The originating auction got a real yield to maturity of -0.630%, a really bad-looking number. It means investors were willing to accept a return 0.630% less than inflation over the next 10 years. Why would they do that? Because yields for all safe investments were deeply depressed. At the time, a 10-year Treasury note had a nominal yield of 1.86%, also highly unattractive.

So this ends up being a matter of which ugly-duckling investment did better if purchased in January 2013 — a 10-year TIPS or a 10-year Treasury note?

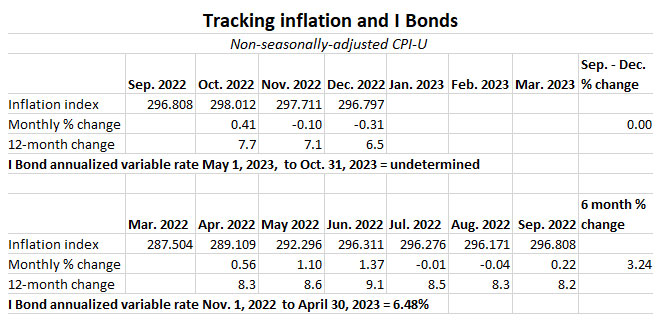

The auction set CUSIP 912828UH1’s coupon rate at 0.125%, the lowest the Treasury will go for a TIPS. And its 10-year inflation breakeven was a lofty 2.49%, much higher than today’s rate of 2.18%, even after two years of ultra-high inflation. In January 2013, annual inflation was running at 1.6%, versus today’s 6.5%.

All of this makes CUSIP 912828UH1 look like an awful investment.

In reality … not so bad

This TIPS ended its life Sunday with an inflation index of 1.29050, meaning it got a cumulative gain from inflation of about 29.1%, or an annualized increase of about 2.6%. Since the inflation breakeven rate was 2.49%, it outperformed the 10-year nominal Treasury by about 0.11% a year. Not spectacular, but this does demonstrate that even a TIPS with a negative real yield and a high inflation breakeven rate can turn out to be a “relatively” good investment.

For most of the last 12 years, TIPS have under-performed nominal Treasurys of the same term, because inflation ran at unexpectedly low levels through much of that time. But the trend has reversed because of the high inflation of the last two years.

My investment in 912828UH1

I didn’t buy at the originating auction, but I did cave in at the May reopening and bought $15,000 of par value, getting a “more attractive” real yield to maturity of -0.225%. This was in a taxable account at TreasuryDirect, and the inflation breakeven also was more attractive at 2.14%. I had to pay $15,511 because of the premium price and inflation index of 1.00837. This TIPS matured Sunday and TreasuryDirect delivered $19,357.50 to my bank account.

That’s a gain of 24.8% on my purchase price, plus I collected 0.125% annually, rising with inflation. So the annualized return was around 2.6%. Was it a great investment? Not really. But good enough. And now I have cash to fund my I Bond purchases in 2023.

One more thing: A followup

Back in early September I wrote an article titled: “What’s up with those crazy real yields on ultra-short-term TIPS?” In the article I used CUSIP 912828UH1 as an example, because I was getting a lot of questions about it, based on this market quote showing a gaudy real yield of 4.047%:

The article explained that because there was only one more coupon payment remaining, and only a few months of highly iffy inflation accruals, the market was probably pricing this issue correctly. Go back and read the article, if you want, but I said it looked like buying on Sept. 1 at the then-current price would result in an annualized return of about 4.28%, better than the yield at the time on a 6-month Treasury, then at 3.34%.

But it did a bit better than that. Here is how it turned out:

So an investor putting $10,000 into this TIPS on Sept. 1 ended up with an investment return of $252, which equates to a nominal return of 2% in 4 1/2 months, or an annualized return of 6.0%, much better than what a 6-month Treasury was paying at the time.

Notes and qualifications

My TIPS vs. nominals chart is an estimate of performance, because annualized inflation rates are based on a full month of inflation in the beginning and ending months, when actually TIPS accruals are based on a half month for the first and last months, with the origination and maturity occurring on the 15th of the month.

Keep in mind that interest on a nominal Treasury and the TIPS coupon rate is paid out as current-year income and not reinvested. So in the case of a nominal Treasury, the interest earned could be reinvested elsewhere, which would potentially boost the gain. For certain, we don’t know what the investor could have earned precisely on an investment after re-investments.

In the case of a TIPS, the inflation adjustment compounds over time, and that will give TIPS a slight boost in return that isn’t reflected in the “average inflation” numbers presented in the chart.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…