By David Enna, Tipswatch.com

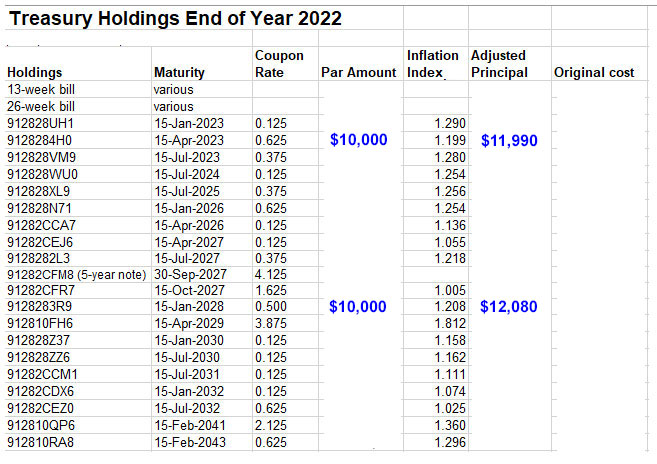

A lot of readers ask about the ladder of TIPS investments I have built over the years. Yes, I do have a ladder, and it does hit every year from 2023 to 2032, and then jumps forward to 2041 and 2042.

Notice the gap? That’s because there are no TIPS issues that mature from 2033 to 2039. Why? Because the Treasury no longer issues 20-year TIPS, leaving a gap in maturities. So I will need to pick up those missing years, one at a time, beginning with this month’s auction of a 10-year TIPS, maturing in 2033.

While it might sound like my ladder was well planned, honestly it was built haphazardly, from purchases of 5- and 10-year TIPS, mostly at auction, and only when I judged real yields to be “attractive.” So the ladder has a lot of maturities this year, in 2023, and then in 2027, because of my purchases of 5-year TIPS in 2018 and 2022, the only two years in the last decade when real yields moved well above zero.

Here is what my ladder looks like, with a few nominals thrown in and actual investment amounts removed. I use an Excel spreadsheet to update the inflation indexes (drawn from the Wall Street Journal) and adjust my principal amounts a few times a year:

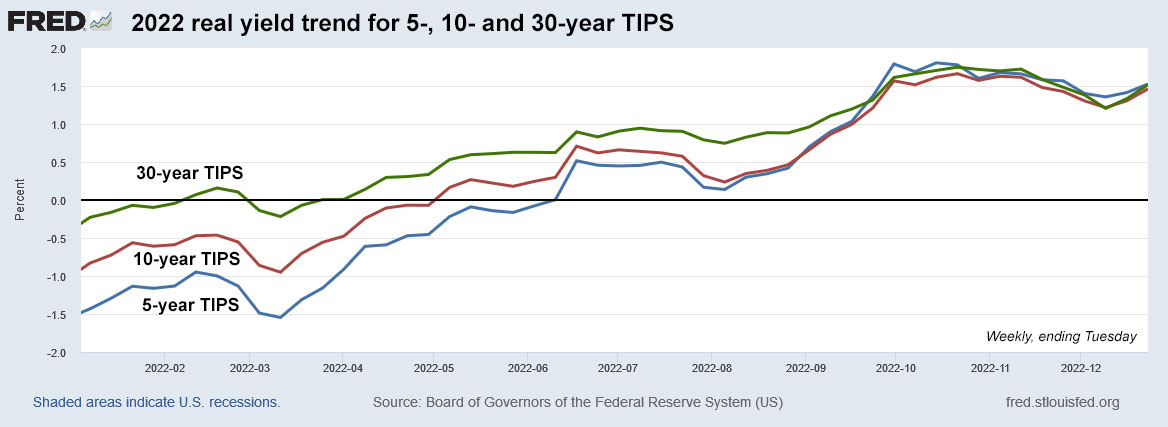

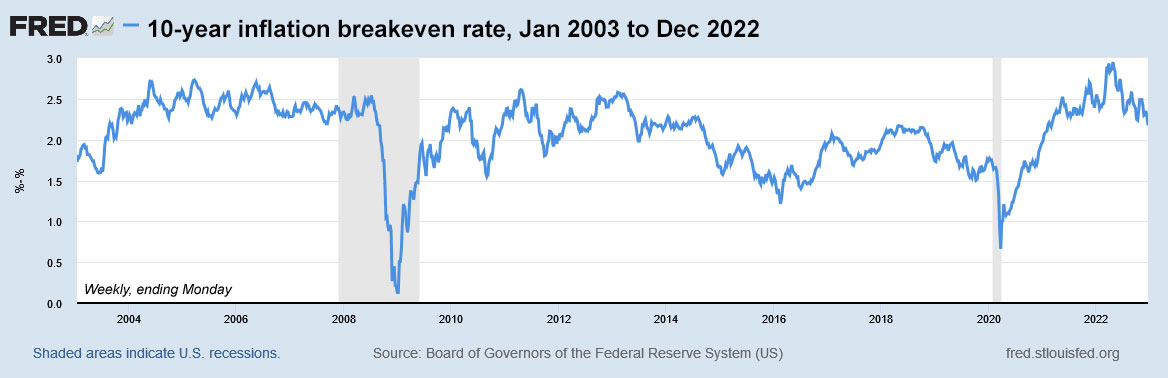

Now here we are in 2023, and again real yields are well above zero across the entire TIPS yield spectrum, with the 5-year at 1.68% and the 30-year at 1.55%. If you are interested in building a TIPS ladder, this is a great time to begin.

Why is a TIPS ladder attractive?

I recently read a well-thought out article titled, “TIPS Funds Vs. A Ladder,” on the SeekingAlpha site. The author is Ralph Wakerly, an investor, entrepreneur and consultant with over 35 years of investment experience. Wakerly argues that historical inflation data suggest the next decade of inflation “may run considerably above the ~3% that consumers and investors expect,” making TIPS a highly attractive investment.

I suggest that you read his entire article, but here are some of his major points:

“For investors at or near retirement, a TIPS ladder is an effective means of generating reliable, predictable income. …TIPS are most effective and reliable if held to maturity. This argues in favor of buying individual bonds via a ladder, not a mutual fund or ETF. …

“You can build an effective TIPS ladder that is relatively simple, with a manageable number of holdings via a mix of auction buys and via the secondary market. …

“A bond ladder via a brokerage account like Fidelity or Vanguard costs nothing. There are no transaction costs and no annual expenses.”

TIPS funds versus a ladder

You can find many smart investors (Bogleheads, especially) who argue that a TIPS fund or ETF is no more risky that holding individual TIPS to maturity. While there may be some logic to this argument (duration matching often comes up as a reason) you have to recognize that the biggest TIPS fund, the TIP ETF, had a total return of -12.24% last year, even as inflation soared to a 40-year high. If you own individual TIPS and are holding to maturity, you can ignore these market swings and just rake in the inflation accruals. At maturity, you are going to get par value x inflation accrual.

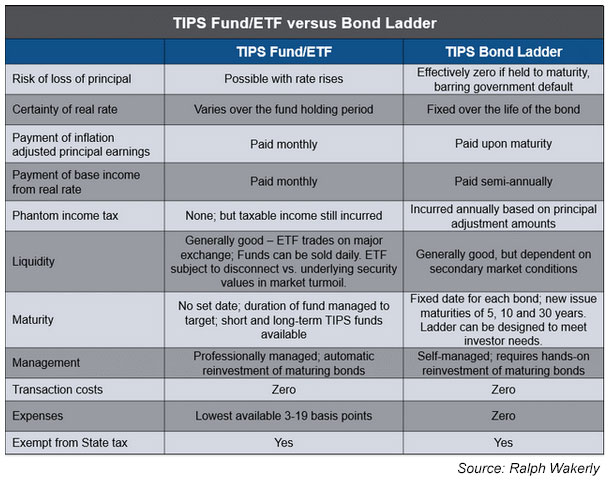

Wakerly came up with this comparison of TIPS funds vs. individual TIPS, an excellent summation:

Consider interest rate risk

As Wakerly notes. “This was painfully evident this year. Fund investors have been punished as the 10 year real TIPS rate went from -1% to the current 1.6%. … However, individual TIPS bonds held to maturity protect against principal loss in the event of rising real rates.”

At a time of rising real yields, TIPS funds are going to suffer. But an individual TIPS will stay on its course to maturity, where it will pay par value + inflation accrual (or at the very least, par value). If you hold a TIPS in a brokerage account, it can be painful to see the loss in “market value” because that is how the broker will report it each day. But in reality, your TIPS is actually holding its principal value (unless deflation strikes), and rising with future inflation. Wakerly says:

In my opinion, this is the most important advantage of buying individual bonds in a ladder versus a fund. This is especially important for retirement investors who want predictable income and cash flow.

Is a ladder really diversified?

Of course it is, if you do a decent job of spacing out maturities and the amounts invested. The TIP ETF only has about 48 holdings — that is all the TIPS trading on secondary markets. A ladder with a few holdings with attractive real yields, maturing at a date to match your needs, is well diversified. Wakerly notes:

From a bond diversification standpoint there isn’t a need to buy a fund. Unlike corporate or muni bonds where you want to diversify default risk across issuers, TIPS are effectively riskless assets backed by the full faith and credit of the US government.

On the other hand, keep in mind that TIPS are a highly specialized investment, designed to protect assets against future inflation. Most people would want to pair their TIPS holdings with low-cost stock index funds, traditional bond funds and some nominal fixed income, such as bank CDs or Treasurys.

Building a ladder

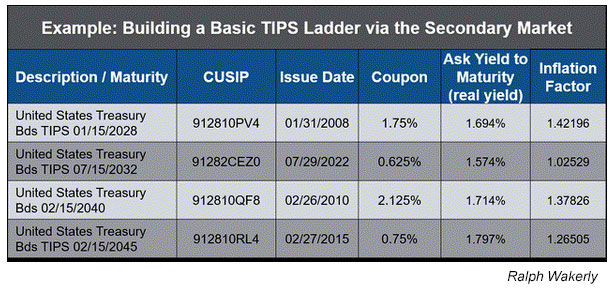

Wakerly says he is building a ladder with an eye on future income needs, so he is focusing on TIPS with a weighted maturity of 18 years. You’d need to consider your future needs. In my case, I am already retired and just trying to protect capital against future inflation, so my ladder focuses more on the near term. Here is Wakerly’s sample ladder:

Another strategy: I have heard from many readers who say they have built a TIPS ladder in their traditional IRA account to account for future required minimum distributions long into the future.

Conclusion

I highly recommend reading Wakerly’s complete article, which goes into greater detail, and another he recently wrote on TIPS titled, “TIPS Performance Could Rival That Of The S&P 500 Over The Next Decade“. (I’m not endorsing that opinion, but after the highly volatile 2022, anything could happen.)

But I do agree with his closing opinion:

“A TIPS ladder is an effective way to invest, especially for those in or near retirement who are comfortable creating their own do-it-yourself annuity. The ladder is currently generating one of the highest yields in the past 14 years with higher certainty of returns, and better principal protection than a mutual fund or ETF.”

One more thing …

For another interesting read on TIPS ladders, check out financial adviser Allan Roth’s October article, “The 4% Rule Just Became a Whole Lot Easier” in which he describes how he painstakingly built a TIPS ladder that will allow 4.36% inflation-adjusted withdrawals over 30 years. He notes, “This is a very attractive strategy for someone wanting a guaranteed inflation-adjusted cash flow in addition to Social Security.”

Roth built this ladder with the help of a Bogleheads contributor, Bob Hinkley, and his article set off a lively — and helpful — discussion in the Bogleheads forum. The article was also referenced in a December Morningstar article titled, “How to Build a TIPS Ladder“.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks for the detailed explanation. I believe you are saying the "breakeven inflation rate" should reflect the inflation expectation rather…