In one week, real yields have increased as much as 30 basis points. Will this trend continue? Yes, if the Fed continues on its current course.

By David Enna, Tipswatch.com

In the last week, the U.S. bond market seems to have finally faced up to reality: There is no longer any reason for interest rates — both real and nominal — to continue at ridiculously low levels. This could either be the beginning of a months-long trend higher, or just another bond market head fake.

Several news events and trends have combined to bring us to this point, including continued very high U.S. inflation, research showing that the Omicron Covid variant is less lethal, and several positive jobs reports. But the key event seems to have been the release of the Dec. 14-15 minutes of the Federal Reserve’s Open Committee Meeting. This is how the Wall Street Journal summarized those minutes:

“Federal Reserve officials at their meeting last month eyed a faster timetable for raising interest rates this year, potentially as soon as in March, amid greater discomfort with high inflation. … Some officials also thought the Fed should start shrinking its $8.76 trillion portfolio of bonds and other assets relatively soon after beginning to raise rates, the minutes said.”

Obviously, inflation is a huge concern for the Fed, because in the opening months of 2022 it is now considering: 1) ending its quantitative easing bond-buying by March, 2) also in March, beginning to increase short-term interest rates, and 3) then quickly transitioning to reducing its massive balance sheet of Treasury holdings and mortgage-backed securities.

Nos. 1 and 2 mean the end of an accommodative Fed policy, and markets have been reacting to those expected (but accelerated) actions with a yawn. But No. 3 — reducing the Fed’s balance sheet — means actual tightening of the U.S. money supply, and the market wasn’t prepared to hear that.

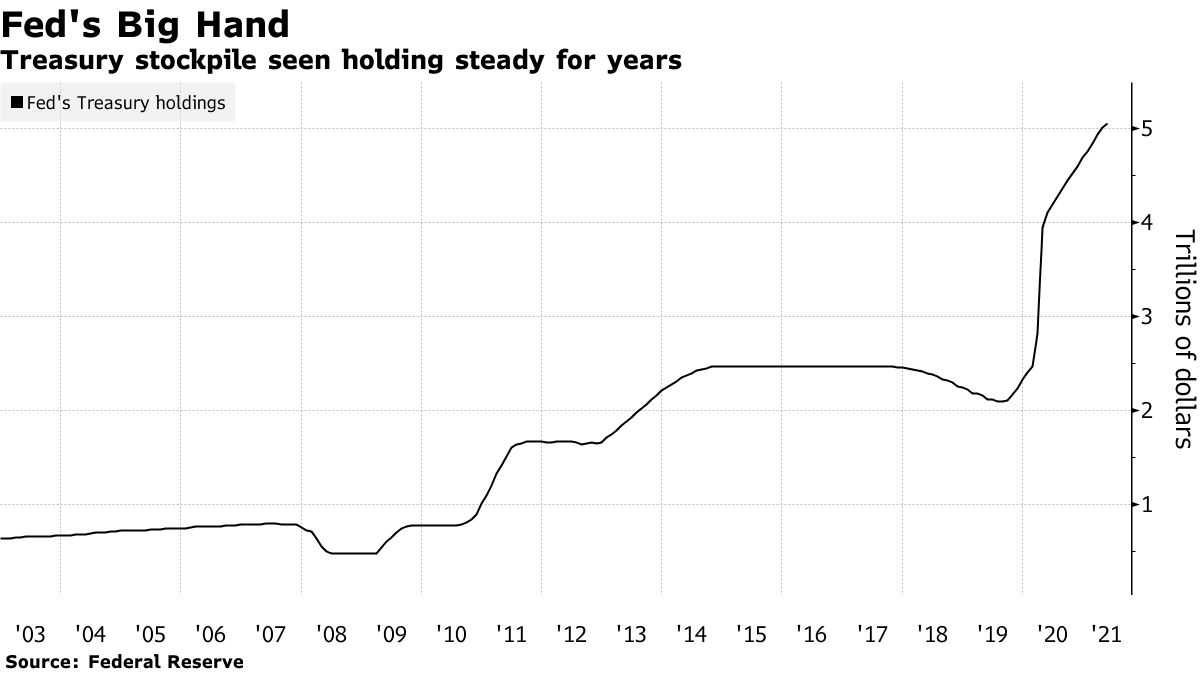

This Bloomberg chart was from a May 20, 2021, article with the now-ironic headline “Don’t Fear the Taper: Fed to Dominate Treasury Market for Years.” The point of the article was that even after the Fed completes its tapering of bond buying, it would continue rolling over its massive holdings of Treasurys and continue surpressing longer-term interest rates.

In this chart, you can spot the last time the Fed began tapering an earlier quantitative easing, at the beginning of 2014. Note that the Fed’s balance sheet remained stable after the tapering for nearly four years. Actual reduction of the balance sheet began in 2018, and it wasn’t extreme, but it resulted in chaos in the bond and stock markets at the close of 2018, a year when the Fed also increased its federal funds rate four times. The S&P 500 fell nearly 15% from Dec. 1 to Dec. 24, 2018, and ended the month down nearly 10%.

So while Bloomberg was advising investors to not fear the Fed in May 2021, conditions are changing dramatically in 2022. And things could escalate this week with the release of the December 2021 inflation report, due out on Jan. 12 at 8:30 a.m. EST. Will the U.S. annual inflation rate rise to exceed 7.0%? It’s possible. (The consensus estimate is 7.1%, but these estimates have been very unreliable over the last 12 months.)

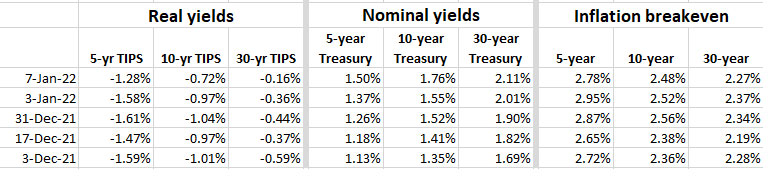

Here is how real and nominal interest rates have reacted over the last month:

Note that the real yield (meaning the yield compared to inflation) of a 5-year TIPS increased 30 basis points in a single week and the real yield of a 30-year TIPS could soon break through the zero barrier for the first time since May 2021. The real yield of a 10-year TIPS rose 25 basis points last week. These are significant moves higher.

But also notice that inflation breakeven rates have held fairly stable. The market is now pricing in future Fed actions to tamp down inflation, with a view that future inflation will average around 2.5% over the next decade.

What this means for TIPS and I Bonds

As real and nominal yields rise, you can expect the values of funds investing in TIPS and Treasurys to take a hit. Here are year-to-date total returns for three key funds (and realize that the year is only 5 market days old at this point):

- Vanguard Total Bond Market ETF (BND): Total return of -1.40%.

- Schwab’s U.S. TIPS ETF (SCHP): Total return of -2.23%.

- Vanguard’s Short-Term TIPS (VTIP): Total return of -0.66%.

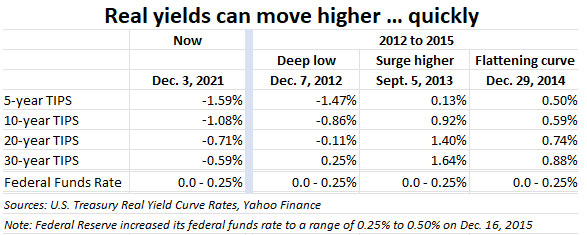

It looks likely that the 30-year TIPS real yield will rise above zero relatively soon, and that is also possible for the 5- and 10-year TIPS, but most likely much later in the year, if at all. Then again, look at the rate history of 2013, when real and nominal yields rose dramatically, even though the Fed took no actions that year except to say it planned to taper quantitative easing:

I created this chart for an article last month, speculating on the possibility of 10-year real yields rising above zero, which could cause the Treasury to increase the I Bond’s fixed rate at the May or November resets. I think that looks unlikely for May, but is a possibility in November, depending on how things play out.

If inflation eases, the pressure will be off the Fed to reduce its Treasury horde, and real yields could continue below zero for much of the year. However, if the Fed does increase its federal funds rate four times in 2022, I think it is likely that the 5-year TIPS yield could rise above zero.

If the 10-year nominal Treasury rises to a level near 2.50% (still relatively low by historic standards), the real yield of a 10-year TIPS should rise to close to zero, or above. Anything much higher and you could see the I Bond’s fixed rate rise, at some point in the future.

However, keep in mind that if the real yields of TIPS rise above zero, and the I Bond’s fixed rate remains at zero, then TIPS will again, finally, be a very competitive investment.

At any rate, my personal plan is to buy my I Bond 2022 allocation this month, to capture the current 7.12% variable rate for six months, and then the next rate, also likely to remain high, for another six months. That’s what I recommend, but many people will disagree, hoping for a higher fixed rate. I don’t think that will happen in May, at least. November could be interesting.

For TIPS investors looking to build out ladders into the future, an increase in real yields will make TIPS much more attractive. If you want to be a net buyer of TIPS, you want real yields to increase.

The Fed can change course

If the stock and bond markets take a frightening turn downward, expect the Fed to back off on a 4th interest rate increase this year, and a reduction in its Treasury balance sheet could be put off for months, maybe years. But the bond buying will end, either way. And short-term interest rates will go higher, either way.

The key will be the rate of U.S. inflation over coming months. It looks likely that high inflation will continue through March at least, before easing off to something closer to 4% for the rest of 2022. But inflation is impossible to predict. The Fed brought us this current surge in inflation. Will it have the courage to bring it under control?

Some historical context:

2013: A year of surging real and nominal yields

2014: The deck was stacked against TIPS funds

2015: The Fed actually did something!

2016: Inflation rises; TIPS out-perform the overall bond market

2017: ‘The calm before the storm’

2018: Did the Federal Reserve go too far?

2019: The Fed cries ‘uncle’; bond investors celebrate

2020: Chaotic year of pandemic fears, stunning stimulus

2021 and beyond: What’s ahead for U.S. financial ma

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Great article! Thank you, David.

David: Great article and valuable perspective. As a retiree, bonds and inflation are key issues to me, and your articles are really valuable. It will be fascinating to watch how things play out with such major influences by the Fed in holdings. Now if I can just get that crystal ball I got at a garage sale to work better….

So true, Clark. The Fed, the stock market and inflation bring constant surprises.