In an auction that capped two days of turmoil in the market for Treasury Inflation-Protected Securities, the Treasury just announced that CUSIP 912828B25 was reopened with a yield to maturity of 0.659% plus inflation, just under the 0.661% this TIPS generated at its initial auction on Jan. 23.

In an auction that capped two days of turmoil in the market for Treasury Inflation-Protected Securities, the Treasury just announced that CUSIP 912828B25 was reopened with a yield to maturity of 0.659% plus inflation, just under the 0.661% this TIPS generated at its initial auction on Jan. 23.

View the Treasury announcement.

This is a 9-year, 10-month TIPS with a coupon rate of 0.625%, meaning today’s buyers are getting it at a slight discount, with an adjusted price of about $99.91 per $100 of value, including in a small amount of inflation appreciation since January.

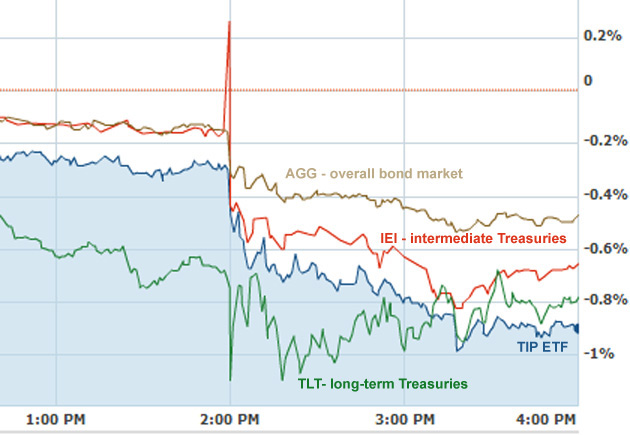

Although this auction broke a string of of eight consecutive 9- or 10-year TIPS auctions with higher yields, buyers today benefited from an upswing in TIPS yields this week, in reaction to the Federal Reserve’s cloudy message on future interest rates. On Monday, this same TIPS closed on the secondary market at 0.493%. That’s a jump of 17 basis points in four days.

Inflation breakeven rate. The nominal 10-year Treasury closed Wednesday with a yield of 2.78%, and has barely budged this afternoon at 2.77%. The 2.77% yield sets up a 10-year inflation breakeven rate of 2.11%. This is a fairly attractive number, and down slightly from the 2.12% of the January auction. It means that if inflation averages more than 2.11% over the next 10 years, this TIPS will outperform a traditional Treasury.

Reaction to the auction. The Wall Street Journal noted ‘lackluster demand’ for TIPS at this auction, ‘reflecting uncertainty about the economy’s ability to generate inflation in the coming years.’ From the report:

After starting the year strong, TIPS have had a tough time in March, handing owners a 0.7% total loss so far through Wednesday. TIPS are a hard sell these days, with the combination of little inflation in the current economy and the Federal Reserve cutting down on stimulus.

The Bloomberg report also noted pointed at low inflation as the cause for the ‘below-average demand’ at this auction:

“It’s a negative environment for inflation right now,” said Aaron Kohli, an interest-rate strategist at primary dealer in New York BNP Paribas SA. … “Investors are not worried about inflation anytime soon. Any risk premium that had been built in is just going away. If the Fed is on a path to taper when inflation is low, it makes no sense to build in a risk premium.”

You might want to be a "travel writer", along with your excellent Tips and I-bond columns. You are pretty good…