By David Enna, Tipswatch.com

The just-released June inflation report is going to be greeted with glee, I think. It was exactly what the stock and bond markets were hoping for.

What happened? The Consumer Price Index for All Urban Consumers rose 0.2% in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all-items index increased 3.0%, the lowest annual rate since March 2021.

Core inflation, which removes food and energy, increased 0.2% for the month (the smallest monthly increase since August 2021) and was up 4.8% year over year.

All of these results came in lower than economist expectations. And it is remarkable to note that annual U.S. inflation has fallen from its high of 9.1% exactly a year ago, to this current rate of 3.0%, getting close to historical norms.

Of course, core inflation remains too high at 4.8% and has been barely inching lower over the last six months. Here is the 12-month trend in all-items and core inflation:

Now that all-items inflation has hit the 3.0% mark (surprisingly quickly), I think continued cuts in inflation are going to be difficult. Part of the reason for the rapid decline in annual inflation has been extremely high year-ago monthly increases (0.91% in February 2022, 1.34% in March, 1.10% in May and 1.37% in June). As we head into the last half of 2023, year-over-year comparisons will be with much lower numbers:

For the first half of 2023 — January to June — U.S. inflation increased 1.95%, which equates to an annual rate of nearly 4%. If we continue on that pace for the rest of this year, the annual inflation rate will start climbing higher. So many factors can effect future inflation: gasoline prices, wage increase, shipping costs, crop failures, etc. It’s too early for the Fed or the markets to declare inflation defeated.

The June inflation report

Gasoline prices rose 1% in June, partially offsetting the 5.6% decrease in May. Gas prices are down 26.5% over the last year, having a huge effect in bringing overall inflation lower.

But the BLS noted that the index for shelter (up 0.4% for the month) was the largest contributor to the monthly all-items increase, accounting for more than 70% of the increase. Other items from the report:

- The cost of food at home was unchanged, but up 5.7% year-over-year.

- The index for meats, poultry, fish, and eggs decreased 0.4% in June.

- Costs of used cars and trucks fell 0.5% for the month and is now down 5.2% year-over-year.

- Costs of new vehicles were unchanged.

- Costs of medical care services were also unchanged.

- The index for motor vehicle insurance was up 1.7% and is now up 16.9% year over year.

What this means for TIPS and I Bonds

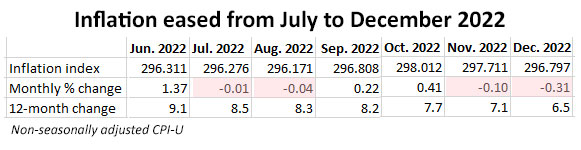

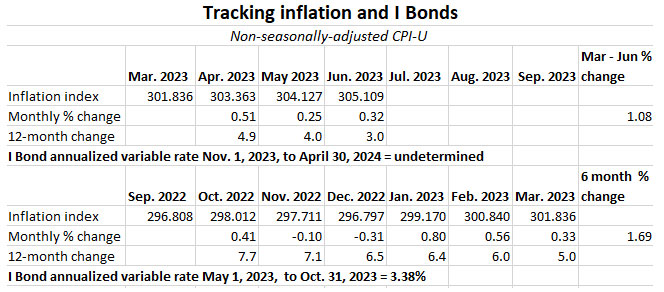

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For June, the BLS set the CPI-U index at 305.109, an increase of 0.32% over the May number.

For TIPS. The June inflation report means that principal balances for all TIPS will increase 0.32% in August, after a 0.25% increase in July. Here are the new August Inflation Indexes for all TIPS.

For I Bonds. The June report is the third of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate. So far, inflation from the end of March to June has increased 1.08%, which if nothing else happens would translate to a new annualized variable rate of 2.16%. But three months remain, so it is far too early to make predictions.

I’d guess we are probably heading toward a new variable rate of around 3.4% to 3.7% (the new fixed rate, however, could be 0.9% or higher, setting up a composite rate of 4.5%+ for six months).

Inflation in the summer months is highly volatile, and non-seasonally adjusted inflation tends to run lower in the second half of the year, after running higher in the first half. Here are the numbers so far:

What this means for the Social Security COLA

The June inflation report sets a baseline for next year’s cost-of-living adjustment for Social Security beneficiaries. The COLA will be determined by comparing the average inflation indexes for July to September with the same number for those months in 2022. View historical data.

For June, the BLS set the CPI-W index at 299.394, an increase of 2.3% over the last 12 months. Last year’s three-month average for July to September was 291.901. So just based on June data, we’d be looking at a COLA increase of about 2.6%, but a lot can happen over the next three months.

I have updated my Social Security COLA page with projections based on differing inflation rates for July to September. Right now, I’d say the COLA looks likely to be in the range of 3.0% to 3.2%. I hope to write about this later in July.

What this means for future interest rates

My belief is that the Federal Reserve will raise short-term interest rates at least once more, and probably twice more in 2023. After that, it could go on a long-term pause, holding rates at these high levels until inflation is clearly defeated.

But, who knows? This morning’s Bloomberg headline says: “US Inflation Hits Two-Year Low, Giving Hope for End to Fed Hikes.” That’s accurate. There is hope. From the article:

Treasury yields plummeted, stock futures rose and the dollar slid following the report. The chances of an additional Fed rate increase after this month slipped to well below 50%.

The report underscores the progress of reducing price pressures since inflation peaked a year ago, aided by more than a year of interest-rate hikes and easing demand. Even so, price pressures are running well above the Fed’s target and will keep policymakers inclined to resume raising interest rates at their July 25-26 meeting.

At this point, the Fed would lose credibility if it fails to raise its federal funds rate 25 basis points in two weeks. That increase has been strongly signaled. After that, the future is uncertain (which is always the case, yes?)

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

“So there is a lot of time to ponder a purchase in May or October.” I think you meant to…