By David Enna, Tipswatch.com

The Treasury just announced results of its $19 billion offering of a reopened 5-year TIPS, CUSIP 91282CGW5, and investors should be pleased.

This 4-year, 10-month Treasury Inflation-Protected Security got an auctioned real yield of 1.832%, the highest for any auction of this term since October 2008. There have been 46 auctions of 4- to 5-year TIPS over that time and only one other — in October 2022, got a real yield higher than 1.7%.

Real yields (meaning the yield an investor will earn above U.S. inflation) have been moving higher in recent weeks, reacting to the Federal Reserve’s potential plan to raise short-term interest rates once or twice again this year.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation.

So, if inflation averages 2.5% over the next 4 years, 10 months, an investor in this TIPS would earn a nominal annualized return of 4.33%. If inflation averages 4%, the return would be 5.83% … and so on.

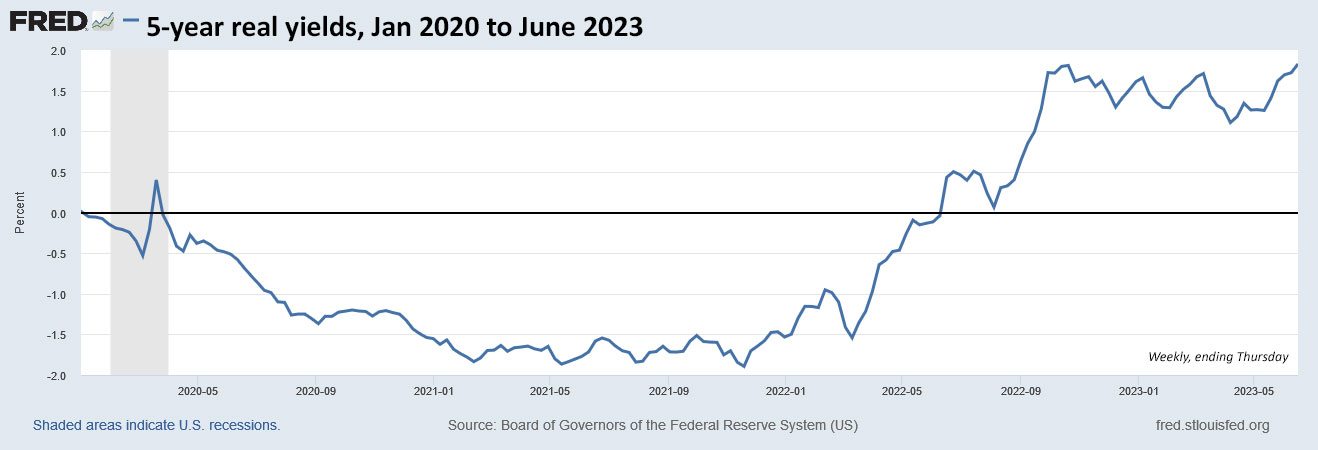

Here is a history of 5-year real yields over the last 14 years, showing the long periods of deeply negative real yields, right up until March 2022, when the Fed began aggressively battling inflation with higher interest rates:

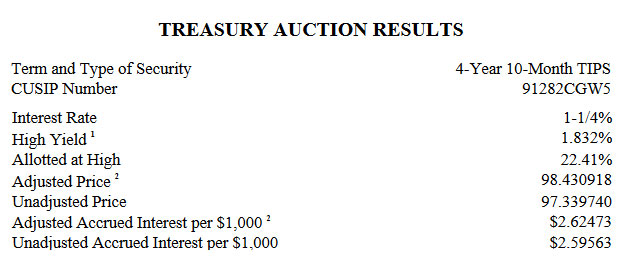

Auction result, pricing

Here are details from the Treasury announcement:

Key factors for investors: 1) the unadjusted price of 97.339740 and 2) the inflation index of 1.01121 on the settlement date of June 30, 2023. This is how the investment pricing works out:

In essence, a $1,000 investment at par for this TIPS will cost $984.31 on the closing date, even though the investor will have $1,011.21 of principal on that date. From that point forward, the investor will earn the coupon rate of 1.25% applied to the principal balance, which will rise (or possibly fall) with future monthly inflation.

The prepayment of accrued interest will be returned at the first coupon payment on Oct. 15, 2023.

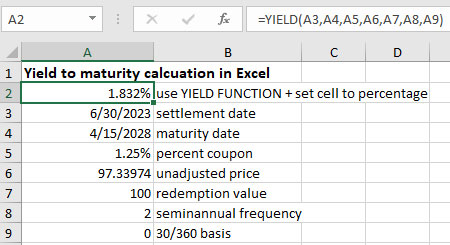

Calculation of real yield to maturity

Several readers have asked about how to do a calculation to check the real yield to maturity. Since this is a Treasury issue, I am confident the 1.832% real yield is accurate, and my rough estimate comes to close to that number. But reader Jim came up with the answer in the comments section below:

The real yield (“High Yield” in Treasury Auction Results) is a classic Yield To Maturity calculation using the issue date, maturity date, coupon rate, coupon frequency, unadjusted price and face value of the bond. It also is based on the day count assumption of a 30/360. If you wish to replicate the computation the easiest way is to use the YIELD function in excel. For this auction it would look like this, YIELD(6/30/2023,4/15/2028,1.25%,97.339740, 100,2,0). YTM is found by finding the rate necessary in the basic bond value equation so that the discounted future coupon payments and bond face amount equals the price paid for the bond. This is done by iterations using different rates until you find the correct value. Best to let a computer do it for you!

So, using Excel’s YIELD function, this is how you can set up the formula and find the result:

Inflation breakeven rate

At the auction’s close at 1 p.m. EDT, a 5-year Treasury note was trading with a nominal yield of 4.03%, creating an inflation breakeven rate of 2.2% for this TIPS. That is the lowest auctioned breakeven rate for this term since an auction in December 2020.

Although 2.2% is a relatively “highish” breakeven rate by historical standards, it seems quite reasonable at a time when U.S. inflation is running at 4.0%. In indicates that this TIPS is cheaply priced versus the nominal Treasury of the same term.

Here is the history of the 5-year inflation breakeven rate over the last 14 years:

Reaction to the auction

Things seemed to go smoothly. Through the morning, CUSIP 91282CGW5 was trading on the secondary market with a real yield in the range of 1.82% to 1.86%. The bid to cover ratio was a solid 2.56, so demand looked reasonably strong. After the auction’s close, the TIP ETF — which holds the broad range of maturities — moved slightly higher, indicating slightly lower yields. That’s an indication of a positive market reaction to the auction.

I was a buyer at this auction, even though I already purchased CUSIP 91282CGW5 at the April auction. A real yield of 1.83% was impossible to pass up. I might (or might not) have been able to do better earlier in the day on the secondary market, but Vanguard’s brokerage was only offering lot sizes of $100,000 or more.

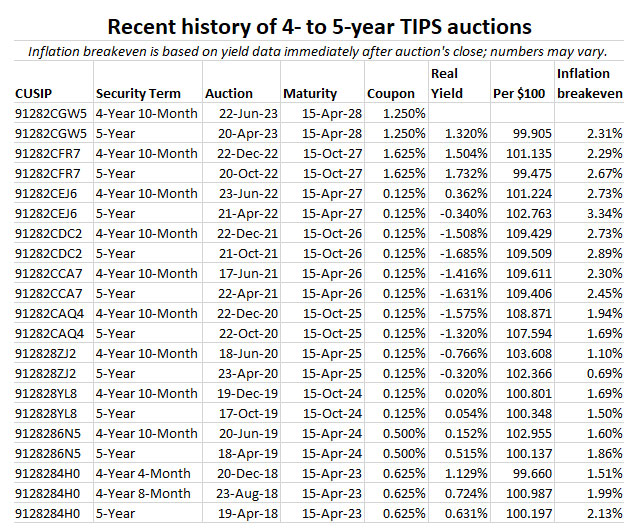

No problem. I am happy with today’s result. If you were a buyer today, post your thoughts in the comments section below. Here are auction results for TIPS of this term over the last 5 years:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I meant regarding 'wait it out' on I-bonds... but to me, TIP bonds right now are a horse of a…