For most of last week, I was stressing out about today, when I will be leaving for South America for a tw0-week-plus trip. It wasn’t the travel that had me stressed. It was the fact that on May 1 the Treasury would announce the I Bond’s new fixed/composite rate and I’d be away from internet for hours.

My hoped-for sighting.

Well, that worked out. The Treasury — for the first time ever — announced the new rates early, on Friday, since all purchases from Friday through October will be receiving the new fixed rate of 0.9% and composite rate of 4.3%. Thank you, Treasury, for the early announcement.

I am expecting to have very little internet access for much of this trip — which includes high mountains, Amazon jungle and remote islands. And that means I will be late posting news, approving comments and answering questions. There will be some news that needs covering before I get back, and I hope to get to it when the internet gods allow it.

What’s ahead

May 2. TreasuryDirect is going down for maintenance from about 6:30 to 8:30 am EDT. Don’t be surprised if it lasts longer. This shouldn’t be a big deal; there are no Treasury auctions scheduled for Tuesday.

May 3. At about 2:15 pm EDT, the Federal Reserve will announce its latest interest rate decision. Everyone expects a 25-basis-point increase in the federal funds rate, putting the rate in the range of 5.00% to 5.25%, slightly above the current U.S. inflation rate of 5.0%.

The key thing will be the message the Fed sends about rates going forward. I don’t usually write about these Fed announcements, which are covered by 1,000 media outlets. But it will be an important bit of news to watch.

May 7. TreasuryDirect is going to remove its notorious “virtual keyboard” sometime this week to “improve the customer experience.” I actually like that keyboard, but it has very few fans. One problem is that it discourages users from creating complex passwords using a password manager. So it actually lessens security, somewhat.

I have no idea what will replace it. Usually, I would write a guide about the changeover, but that probably won’t be possible, because I will be in an the Amazon jungle about that time.

May 10. The Bureau of Labor Statistics will release its April CPI report. All CPI reports are crucial, but this one is a little less so since the March report set the I Bond’s current variable rate of 3.38%. I will try to post an analysis when I can get connected.

The Cleveland Fed’s inflation nowcasting is predicting all-items inflation of 0.6% for April and 5.2% year over year, putting U.S. inflation back on an upward path. That would be bad news for the markets, but these Cleveland Fed predictions often miss the mark.

May 11. Treasury will announce the May 18 reopening auction of CUSIP 91282CGK1, creating a 9-year, 8-month TIPS. I would normally post a preview article on Sunday morning, May 14. That might (or might not) happen.

May 18. If all goes as planned, I will be home on the day of the 10-year TIPS auction, which closes at 1 p.m. EDT, and things will be returning to normal. I will posting the results and an analysis after the auction.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Composite rate will fall from 6.89% to 4.30%, but the fixed rate of 0.9% is highly attractive for long-term holders.

By David Enna, Tipswatch.com

Surprise! I Bonds purchased from May to October 2023 will get a fixed rate of 0.9% and a composite rate of 4.3%, TreasuryDirect announced this morning, jumping the gun on its expected May 1 press release. It’s all right there on its homepage:

At first, I thought this was posted by mistake, jumping ahead of Monday’s announcement. In the 12 years I have been writing about I Bonds, the new rates have never been announced early.

A few minutes later, the TreasuryDirect site went down, possibly because of the “what the hell?” factor driving traffic. But I was able to return to the site a bit later and it loaded, with the same information.

I had been speculating that the I Bond’s new fixed rate would be about 0.6%, so 0.9% is great news. It is the highest fixed rate since the reset in November 2007. The fixed rate tells you how much the I Bond will earn above official U.S. inflation. It is equivalent to the “real yield to maturity” of a Treasury Inflation-Protected Security.

The site has the full information on the new rate and how it was determined, combining the new inflation-adjusted variable rate of 3.38% with the new fixed rate of 0.9%.

Fixed rate

0.90%

Semiannual (1/2 year) inflation rate

1.69%

Composite rate formula: [Fixed rate + (2 x semiannual inflation rate) + (fixed rate x semiannual inflation rate)]

[0.0090 + (2 x 0.0169) + (0.0090 x 0.0169)]

Gives a composite rate of

[0.0090 + 0.0338 + 0.0001521]

Adding the parts gives

0.0429521

Rounding gives

0.043

Turning the decimal number to a percentage gives a composite rate of

4.30%

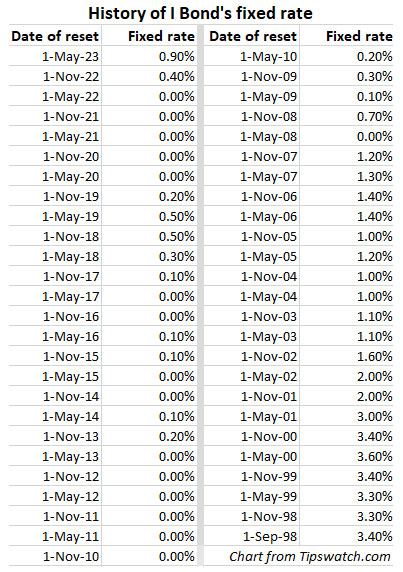

TreasuryDirect’s page listing the history of fixed rates now includes the 0.9% rate, more than doubling the 0.4% fixed rate in effect for purchases through April 30.

The current composite rate for I Bonds purchased through April 30 is 6.89% and that will fall to 4.3% for purchases from May to October 2023. But the fixed rate of 0.9% makes the May-to-October purchases very attractive.

Just as an aside, the new composite rate for I Bonds purchased from November 2022 to April 2023 will be 3.79%, which reflects the fixed rate of 0.4% and inflation-adjusted rate of 3.38%.

TreasuryDirect said this week that the last day to place orders for the 6.89% rate was yesterday, April 27. (I placed my order on April 26.) So I am assuming that any I Bond purchased today will get the new May 1 rate. And that could be why the Treasury decided to post the new rate information, since we can assume it will take effect for purchases today.

EE Bonds

The Treasury also announced that the new fixed rate for EE Bonds will be 2.5% for savings bonds issued from May 1 to Oct. 31, 2023. This is up from the current fixed rate of 2.1%. The Treasury is retaining the policy that EE Bonds are guaranteed to double in value if held for 20 years, creating an effective interest rate of 3.53%.

Gift box strategy?

The Treasury limits purchases of I Bonds to $10,000 per person per year, so investors need to think through a strategy for the best time to invest. If you were planning on holding the I Bonds for less than 2 years, the smart move was to buy in April, locking in an annual return of about 5.4%. For long-term holders, buying in May is preferable, locking in the 0.9% fixed rate for the full 30-year term of the I Bond.

Earnings from the new 0.9% fixed rate create a breakeven period of about 3 years, 8 months. If you plan to hold less than 3 years, 8 months, buying in April works out better. Anything longer will make the May rate more attractive.

The dilemma: Now the fixed rate rises to 0.9%, but you already bought your full allocation this year. (True for me.) What do you do?

If you bought in April, like I did, you can still use the gift box strategy if you have a spouse or a trusted friend or family member with a separate TreasuryDirect account. Using this strategy, anytime before the end of October you can place $10,000 into the TreasuryDirect gift box, assigned to your partner, and your partner would do the same for you.

Some basics of the gift box strategy:

When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

“I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Rolling over 0.0% fixed rates?

If you are holding I Bonds with 0.0% fixed rate — especially those held for five years or more — you can consider redeeming those older I Bonds for new ones with the 0.9% fixed rate. When you redeem, you will owe federal taxes on the interest earned.

I think this is a sound strategy, especially if you don’t want to raise another $20,000 to buy I Bonds this year in two separate accounts.

One key thing to consider is to wait until the current variable rate of 6.48% has completed and the new rate of 3.38% has begun. You have until October to make a purchase of I Bonds with the 0.9% fixed rate. No rush.

If you have held the I Bond less than five years, consider waiting an extra three months to have the three-month interest penalty apply to the lower composite rate.

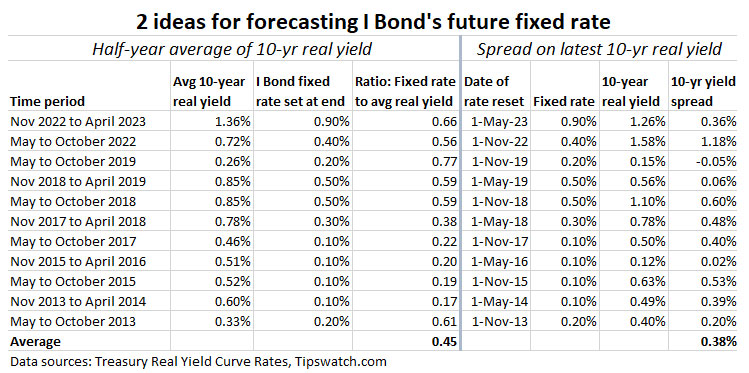

Projecting the fixed rate

We still don’t know how the Treasury decides on setting the fixed rate of the I Bond, but it’s becoming clear that the rate tracks higher and lower with real yields of Treasury Inflation-Protected Securities. We just don’t know how much. TreasuryDirect recently added this “less vague” statement to its FAQ page on I Bonds, clearly indicating that market real yields are a factor in setting the fixed rate:

The Secretary of the Treasury, or the Secretary’s designee, determines the fixed rate. The rate is based on market rates that have been adjusted to account for the value of components unique to savings bonds. These include the early redemption put option, tax deferral feature, deferred purchase feature, and Treasury’s administrative costs.

Here is the final version of my two prediction models for the I Bond’s fixed rate. The columns on the left show how the fixed rate compares with the average of the 10-year real yield over the last six-month rate-setting period. The columns on the right show how the fixed rate compares with the latest real yield of the 10-year TIPS.

Click on the image for a larger version.

I have limited these numbers to the times when the Treasury raised the fixed rate above 0.0% going back to November 2013, solidly in the era of Federal Reserve intervention in the U.S. bond market.

If you look at the calculation on the right, the average yield spread between the latest 10-year TIPS and the I Bond fixed rate is 38 basis points. The new fixed rate of 0.9% is 36 basis points below the current 10-year real yield of 1.26%. So that looks good as a predictor, but this calculation isn’t very reliable except to predict if the fixed rate is likely to rise or fall.

The half-year average calculation is more reliable, I think, and in more recent rate changes the ratio has been in the range of 0.59 to 0.77. Today’s fixed rate announcement of 0.9% puts the ratio at 0.66, right in the middle. I think this half-year-average formula is more reliable, but still nowhere near perfect.

To close, here is the history of all fixed rates for I Bonds back to their inception in September 1998:

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Moody’s Analytics, a market research firm that is a subsidiary of Moody’s Corp., just issued an April 2023 analysis with new information about the debt crisis and the approaching X-date, when the Treasury will run out of cash needed to pay the government’s bills on time.

A key point in the analysis is that the date appears to be coming earlier than researchers originally thought:

The Treasury debt limit—the maximum amount of debt that the Treasury can issue to the public or to other federal agencies—was hit on January 19, and since then the Treasury has been using “extraordinary measures” to come up with the additional cash needed to pay the government’s bills.

Nailing down precisely when these extraordinary measures will be exhausted … — the so-called X-date — is difficult. It depends on the timing of highly uncertain tax receipts and government expenditures.

Since Moody’s Analytics began estimating the X-date early this year, we have thought it to be in mid-August. But April tax receipts are running 35% below last year’s pace, which is meaningfully weaker than anticipated. And despite weaker tax refunds than anticipated, it appears that the X-date may come as soon as early June. If not, and Treasury is able to squeak by with enough cash, then the X-date looks more likely to be in late July.

The Moody’s report reinforces my argument that the debt crisis is beginning to be seen in clear disruptions in the bond market. It says:

Time is running out for lawmakers to act and increase or suspend the debt limit, and global investors are suddenly focusing on the risks posed if they do not act in time.

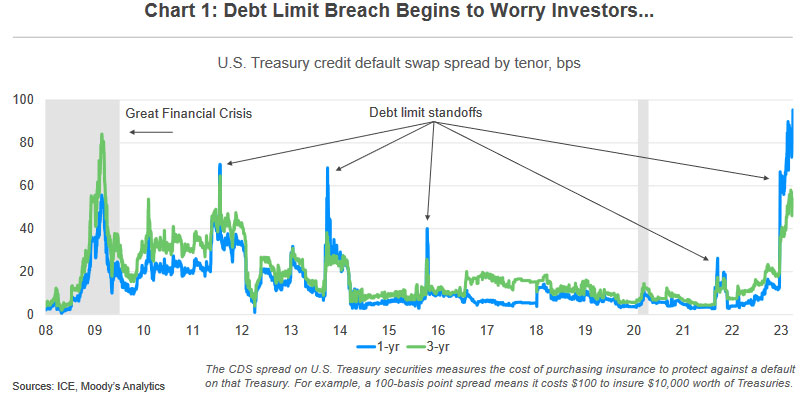

The analysis points out that credit default swaps on U.S. Treasurys — the cost of buying insurance in case the Treasury fails to pay its debt on time — have jumped in recent weeks, to levels even higher than past debt-ceiling disruptions.

At close to 100 basis points, CDS spreads on six-month and one-year Treasury securities are already substantially more than in 2011 when that debt limit drama was so unnerving it caused rating agency Standard & Poor’s to strip the U.S. of its AAA rating.

Cick on the image for a larger version. Source: Moody’s Analytics

The analysis also notes the recent sharp decline in the yield of the 4-week Treasury bill, which was the major point of my article earlier this week:

As it has become clear in recent days that April tax receipts were coming in weak and the X-date may be just a few weeks away, investors have piled into the safety of one-month Treasury securities. Yields have plummeted, from 4.75% at the start of April to less than 3.4% currently. At the same time, yields on three-month Treasury bills have continued to rise. The difference between one- and three-month Treasury bill yields has never been as wide. Global investors thus appear to be attaching non-zero odds that the debt limit drama will end with a default sometime in June or July.

Source: Moody’s Analytics

The GOP spending proposal

The analysis goes on to examine the ramifications of the House Speaker Kevin McCarthy’s proposal to roll back discretionary U.S. spending in 2024 to 2022 levels — in exchange for a one-year increase in the debt limit. It’s an interesting analysis, and I’ll let you read it and reach your own conclusions. It seems highly unlikely that McCarthy’s proposal will end up being the final settlement of this issue.

At any rate, the White House issued a statement Tuesday declaring that if McCarthy’s bill reached President Biden’s desk, “He would veto it.”

What’s next

Moody’s Analytics notes that the Treasury debt limit drama is heating up and is likely to get much hotter in coming weeks. It notes:

If the X-date is as soon as early June, it seems a stretch for lawmakers to come to terms fast enough, and they instead will likely decide to pass legislation suspending the limit long enough to line the X-date up with the end of fiscal 2023 at the end of September. This will buy some time …

Getting legislation that funds the government in fiscal 2024 and increases the debt limit across the finish line into law will surely be messy and painful to watch, generating significant volatility in financial markets. Indeed, a stock market selloff, much wider credit spreads in the corporate bond market, and a falling value of the U.S. dollar may be what is required to generate the political will necessary for lawmakers to avoid a government shutdown and breach of the debt limit.

My thinking has been that Congress will eventually have to kick the debt-limit issue down the road to avoid severe disruptions to the bond and stock markets. Moody’s suggests the extension could be to September, when we could relive this crisis again.

But the political divide — and the resulting game of chicken — seem a lot more severe this year, with just a few GOP House members potentially able to block any compromise. In a hopeful note, Moody’s concludes:

But when all is said and done, the legislation that lawmakers ultimately pass will likely be anticlimactic, allowing both House republicans and president Biden to declare political victory.

What should we do?

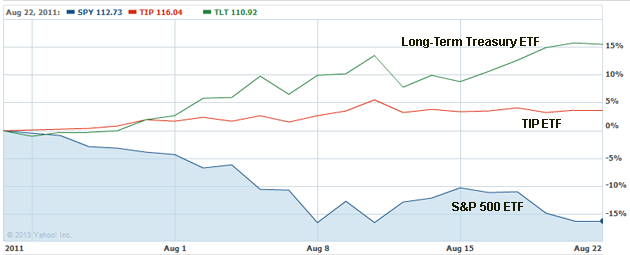

In a worst-case scenario we could see a repeat of August 2011, a very bad month for the stock market, but quite nice for bonds:

But I suspect that history won’t repeat itself in this way. Bonds benefited in 2011 from increased liquidity supplied by the Federal Reserve, but that might be out of the question in 2023 as the Fed battles inflation. The stock market in recent years has been through the wringer, over and over, and bounced back. But this time, it may not have the Fed as its savior.

I am not a financial adviser and I’ll admit that I am not doing much differently in the lead up to this crisis. For example, some possibilities:

Sell all your stocks and move to cash? One of the big differences between 2011 and today is that cash is much more attractive, with yields above 5% for many short-term Treasurys. In August 2011, the 6-month Treasury bill was paying 0.16%. Today, cash is an appealing alternative. The only problem: How safe are Treasurys in a worst-case scenario? (The answer, in my opinion: still very safe.)

No, I personally won’t be selling out of the stock market. But I could see raising some cash because of the chance to …

Snap up attractive yields when you see them. This week I bolstered my bond ladder by buying a two-year, brokered, non-callable Morgan Stanley CD paying 4.7%. The 2-year Treasury note auctioned Tuesday at 3.97%, so the CD is a better deal. (This is in a tax-deferred account, so the state income tax issue doesn’t apply.)

Watch for market chaos. There could be a buying opportunity, and it could be as short as a few hours of a single day. I’d expect yields on some short-term Treasurys to begin rising higher in coming weeks, as the fear factor sets in. Then … a compromise is announced and everything moves back to what we now call “normal.”

Do nothing. Not a bad option. In the long term, the market will adjust. In 2011, after a miserable August, the S&P 500 ended the year with a total return of 2.1%, followed by 16.0% in 2012 and 32.4% in 2014.

What do you think? Tell us your strategy in the comments section below.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

On Thursday afternoon, I happened to be watching CNBC during a long on-air interview with Cathie Wood, CEO and founder of Ark Invest, an investment management firm.

Wood is an interesting person, obviously a high-risk investor whose shoot-for -the-moon style is completely opposite mine. I find a lot of her market commentary is designed to bolster the high-risk stocks her funds already own. She’s a believer. But midway through the interview, she said something that made me jump up and say, “NO!”

Listen to the first two minutes of this clip:

Here is the quote that gave me pause:

I think the markets are leading the Fed and I was struck today to learn that the one-month Treasury bill yield is 140 basis points — 1.4% — below the low end of the Fed funds rate. I remember in ’08 and ’09 the Treasury bill rates were an early indicator of how quickly the Fed was going to ease once it realized how much trouble we were in.

What is really happening here?

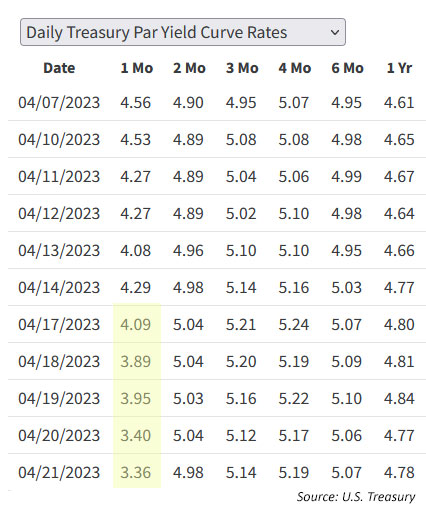

No, the bond market is not anticipating a quick turnaround by the Fed on short-term interest rates. If that were true, you’d see yields falling across all T-bill maturities. But that isn’t happening. Only the 4-week T-bill has seen yields plummet in the last three weeks, as you can see in this chart:

The chart, from the Treasury’s Yields Curve estimates page, shows that the 4-week T-bill’s yield has fallen 120 basis points in three weeks, while the 8-week is up 8 basis points and the 13-week is up 19 basis points. The same is true across the T-bill spectrum — every issue except the 4-week has seen yields rise in April.

Now, why would that happen? The reason is simple: Investors are pouring into the 4-week T-bill, forcing its yield lower, because of the near-certainty of market turmoil coming with the expiration of the U.S. debt ceiling. This is highly likely to reach “crisis” level by June, about 6 weeks from now. From the Washington Post:

If Congress doesn’t increase the limit on how much the Treasury Department can borrow, the federal government will not have enough money to pay all its obligations by as early as June. Such a breach of the debt ceiling — the legal limit on borrowing — would represent an unprecedented breakdown

If you look at the timing of this highly likely crisis, you can see that the 4-week T-bill can be purchased now and mature with a couple weeks to spare. So, in theory, it is much “safer” than the 8-week, which now has a yield 162 basis points higher. Same with the 13-week, which has a yield 178 basis points higher.

The 4-week and 13-week generally follow a similar trend line, but as the debt crisis gets closer, they have diverted:

Click on the image for a larger version.

To be clear: I am not saying that the United State will begin defaulting on its debt in June or August. That would be an utter disaster and I don’t think it will happen. But I also think there will be no resolution to this issue until we approach the brink of calamity. And that is going to cause market uncertainty.

For one thing, the yield on that 4-week T-bill will begin rising dramatically sometime in May, as we approach a potential government shutdown or debt breach.

This has happened before

2011. Back on March 6, 2023, I wrote an article (Debt-limit crisis: Lessons from the 2011 earthquake) looking back on a very similar crisis in mid-2011. This one was the most serious up to this year, but eventually was resolved on August 1. It triggered a frightening stock market collapse and solidified a near-decade of ultra-low Treasury yields. This chart shows the massive moves in Treasurys and the stock market in a single month, August 2011:

Click on image for a larger version.

The 2011 crisis went to the brink but was resolved. Nevertheless, Standard and Poors lowered its credit rating on U.S. debt from AAA to AA+, a rating that remains in effect today.

But here is the point I wanted to make in this article: The T-bill market began anticipating the approaching crisis, with both the 4-week and 13-week T-bill spiking higher in the days before a potential government shutdown.

Click on the image for a larger version.

Of course, at this time in 2011 the Federal Funds Rate was already as low as it goes, in the range of 0% to 0.25%. So the move higher in the 4-week was only 15 basis points, from 0.01% on July 20 to 0.16% on July 29. But then again, the yield on July 29 was 16 times higher than it was on July 20.

By August 8, two days after the S&P downgrade, the 4-week yield was back down to 0.2%. In other words, the S&P action had zero effect on the U.S. Treasury market. The yield on a 10-year Treasury note was at 2.82% on July 29 and fell to 1.89% on Dec. 30. So when you hear people say, “The 2011 crisis increased U.S. borrowing costs,” just realize this is not true.

2013. A similar debt-ceiling crisis erupted in 2013 after the debt ceiling was technically reached on Dec. 31, 2012. Eventually, the debt ceiling was suspended for a few months, then reinstated. The crisis reached a peak in early October and was resolved on Oct. 16.

Click on the image for a larger version.

The chart shows the extreme, but short-lived, spike in the 4-week T-bill yield as the crisis reached a high point. Again, at the time the Federal Funds Rate was in the range of 0% to 0.25%. The 4-week T-bill yield rose from 0.1% on Sept 9, 2013, to 0.32% on Oct 15, and increase of 32 times.

What happens in a debt-lock?

I don’t think the U.S. is going to default on its debt, but there’s a real possibility we will see a short-term government shutdown and disruption to government payments. No one knows exactly how this would play out.

“Once again, the debt ceiling is in the news and a cause for concern. If the debt ceiling binds, and the U.S. Treasury does not have the ability to pay its obligations, the negative economic effects would quickly mount and risk triggering a deep recession.”

In speculating on how a debt-lock could be handled, the authors note that the U.S. government created a contingency plan in 2011 at the height of the crisis:

“Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.”

Also in March, Moody’s Analytics published a paper titled, “Going down the debt limit rabbit hole.” It predicts the actual “X-date” of potential breach is Aug. 18. It notes:

Investors in short-term Treasury securities are coalescing around a similar X-date, demanding higher yields on securities that mature just after the date given worries that a debt limit breach may occur.

Unless the debt limit is increased, suspended, or done away with by then, someone will not get paid in a timely way. The U.S. government will default on its obligations.

In discussing worst-case scenarios, Moody’s notes:

A more worrisome scenario is that the debt limit is breached, and the Treasury prioritizes who gets paid on time and who does not. The department almost certainly would pay investors in Treasury securities first to avoid defaulting on its debt obligations.

But Moody’s also notes the potential political fallout, saying, “Politically it seems a stretch to think that bond investors, who include many foreign investors, would get their money ahead of American seniors, the military, or even the federal government’s electric bill.”

I highly recommend reading through the entire Moody’s report. It presents an unpolitical and unvarnished point of view.

Final thoughts

My main point here was to show that the short-term Treasury market is already being affected by the looming crisis, and things are likely to get a lot more volatile. I don’t have answers to the “What would happen if …” questions readers often ask. We are moving into an uncertain time and the financial markets don’t like uncertainty.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

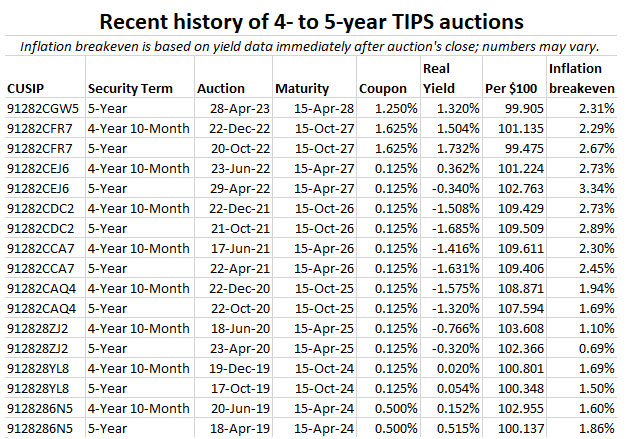

The Treasury’s auction of $21 billion in a new 5-year Treasury Inflation-Protected Security — CUSIP 91282CGW5 — resulted in a real yield to maturity of 1.320%, a bit higher than looked likely through the morning.

Demand appears to have been fairly weak for this 5-year TIPS. The bid-to-cover ratio was 2.34, the lowest for any TIPS auction of this term for as long as I’ve been recording this data (back to June 2019). A similar TIPS was trading on the secondary market all morning with a real yield around 1.29%. So … 1.32% looks good.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above (or below) inflation.

Pricing: The coupon rate for this TIPS was set at 1.25%. Because the real yield was higher, investors paid an unadjusted priced of about 99.664 for $100 of par value. The inflation index will be 1.00241 on the settlement date of April 28, and that means investors will pay an adjusted price of about 99.91 for about $100.24 in principal. (Plus about 4 cents for accrued interest.)

It’s a small thing, but a lot of TIPS investors tell me they relish the idea of buying a TIPS below par value, because par value is guaranteed to be returned at maturity, even if we hit a period of extended deflation. This TIPS delivered.

The yield. Real yields for all TIPS have risen sharply over the last year, but peaked in fall 2022 and have slid a bit lower since then. Here is the one year trend in the 5-year real yield:

Click on the image for a larger version.

The auction’s result of 1.320% looks in line with the trading range we’ve seen over the last several months. As recently as March 8, the 5-year real yield hit 1.87% but began falling in reaction to the U.S. banking turmoil. It dipped as low as 1.06% on April 6.

Inflation breakeven rate

At the auction’s close, a 5-year nominal Treasury note was yielding 3.63%, giving this TIPS an inflation breakeven rate of 2.31%, which is historically high but looks attractive with U.S. inflation currently running at 5.0%. I’m a bit surprised we didn’t see higher demand for this auction, because the nominal 5-year at 3.63% isn’t very attractive. At least the TIPS protects against unexpected inflation.

Here is the one-year trend in the 5-year inflation breakeven rate, showing that 2.31% is on the low end of recent rates:

Click on the image for a larger version.

Reaction to the auction

How did the market react to the auction results? With a yawn. The TIP ETF, which holds the full range of maturities, barely budged after the auction’s close at 1 p.m. EDT. So it looks like things went as expected, even though demand was weak.

For investors, getting 1.32% above inflation for the next five years is attractive. Just one year ago, on April 29, 2022, a new 5-year TIPS auctioned with a real yield of -0.340%. Times have changed, huh?

I was a buyer at this auction, fulfilling my wish to bolster the 2028 rung of my TIPS ladder. This TIPS will get a reopening auction on June 22 and then a new 5-year TIPS will be auctioned in October and reopened in December.

Here is the recent history of TIPS auctions of this term:

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thanks!