Yields could continue to rise, but it may be time to think longer term.

By David Enna, Tipswatch.com

In the last week, I got calls from CNBC and Bloomberg reporters asking to talk about the rise in demand for short-term Treasurys, triggered by the recent surge in yield on a 26-week T-bill to 5+%.

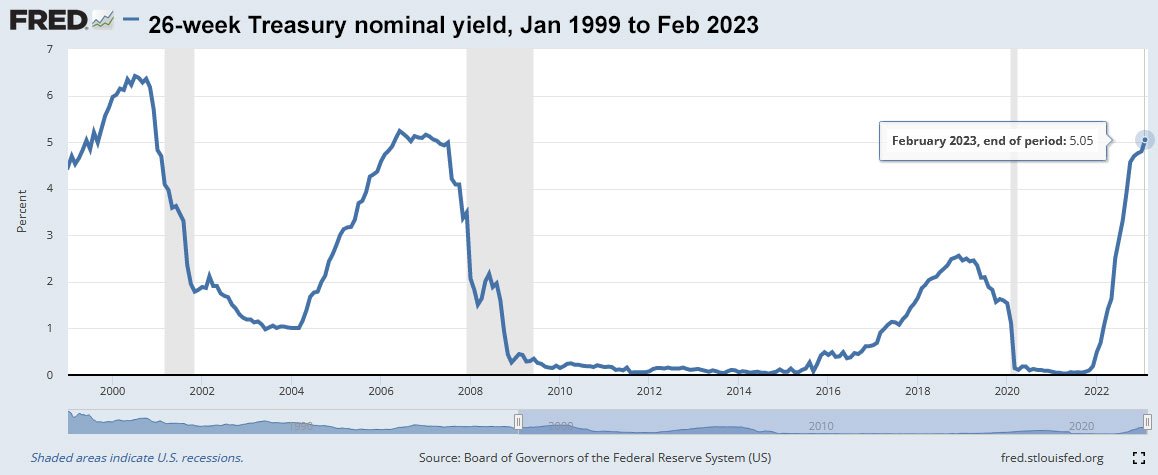

Why is that a big deal? Well, take a look at this amazing chart:

Last week, the 26-week Treasury bill crossed the 5% barrier for the first time since July 2007 — nearly 16 years ago. And for much of those 16 years, nominal yields on this ultra-safe investment were hugging very close to zero. Getting a no-risk, short-term return of 5% on your money is highly appealing, even if U.S. inflation continues to run at an annual rate of 6.4%.

Last July, I wrote an article detailing a strategy for staggering purchases of 13-week and 26-week Treasury bills, spacing out purchases and then rolling them over to capture rising interest rates, while also preserving easy access to your money. At the time, the 13-week was yielding 1.73%; today it is at 4.68%. The 26-week was yielding 2.62%; today it is 5.05%.

That strategy worked very well: It got money working immediately while also capturing future increases in interest rates. But at some point, possibly in the next six months, the Federal Reserve is going to call a halt to rate increases and move into “hold” mode. The rollover strategy would still work, but there will be no short-term rate increases to capture.

What’s the next move?

As interest rates near a peak — and I don’t claim to know when that will be — wouldn’t it be smart to begin allocating some funds to longer terms of U.S. Treasurys? Eventually, maybe sometime in 2024, short-term rates will begin moving lower (I think). At that point,the rollover strategy won’t be attractive.

Just look at the 26-week yield chart again. Notice how each time the yield peaks it begins a rather quick move downward? And notice how the past peaks have been followed rather quickly by a recession? Is that where we are heading?

Also, consider that if you buy a 26-week Treasury this week (the next auction is Monday), it is going to mature in August, possibly right at the peak of the U.S. debt crisis. Will that really matter? Probably not, but things could get a little crazy between now and then. And could that craziness make the Fed more cautious?

Longer-duration Treasurys will generally do well in a recession because interest rates are likely to fall, resulting in a higher value for your investment. Nothing is certain, of course, but the market seems to be shifting its focus toward medium-term Treasurys.

Here are January vs. February auction results for Treasury issues of various terms:

The chart shows that the 26-week T-bill is now the “sweet spot” investment, with the highest nominal yield across the entire maturity spectrum. But … notice how yields have been rising faster for the longer-term Treasurys, with the yield on a 5-year Treasury note rising 58 basis points in a month, versus 24 basis points for the 26-week. The 10-year Treasury note is now trading around 3.95%.

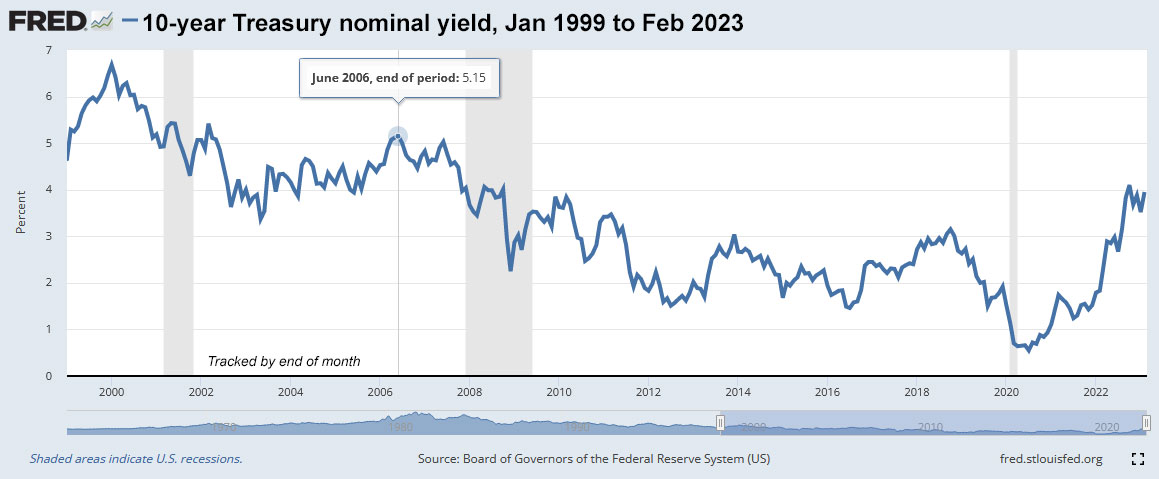

These longer-term yields may continue to rise, but they are starting to get attractive, matching the highs of October 2022 and closing in on the highs of June 2006. Here are long-term views for the 2-, 5- and 10-year Treasury notes:

What’s the strategy?

My idea is to add some medium- or even longer-term nominal Treasurys if I can find attractive rates, as a hedge against future recession and eventual declines in interest rates.

Keep in mind that 4-week to 26-week Treasury bills will remain the ideal investment for your short-term cash needs. Another sensible option for cash is a top-of-class money market fund, such as Vanguard’s Treasury Money Market Fund (VUSXX), with a 7-day SEC yield of 4.55%.

Are bank CDs an option? Sure. Online banks often offer promotional rates to lure your investment. You can probably find a 6-month CD paying 4.75% or a one-year at 5%. Those rates are competitive. Also, you can find 5-year CDs paying around 4.65%, also competitive. But do you really want to open another new account at an unknown bank? Plus, interest from these accounts face state income taxes, while Treasurys are free of state taxation.

So this week I decided to hunt through the secondary Treasury market to see if I could find a 5-year Treasury yielding close to 5%, or a 10-year at 4%. (I’d prefer to see the 10-year at 5%, but I decided to be realistic.) My plan was to nibble into these nominal investments as a backstop to my ladder of TIPS investments.

As of Friday afternoon, my search failed but the market is getting close, at least for the 10-year:

Market conditions right now remind me a lot of late September and October 2022, when nominal and real yields were peaking. At that time, I bought a 5-year Treasury note at auction with a yield of 4.22%, very close to today’s market. But by early November, yields began falling in reaction to a series of weak inflation reports.

I doubt that yields will plummet in the near term, and the Federal Reserve seems strongly committed to raising short-term interest rates another 50 to 75 basis points before summer. So let’s be realistic, I’ll admit I have no strategy. I just want to hedge my inflation bets with some reasonable nominal yields.

After hunting around Friday, I ended up making a “nibble” investment in CUSIP 91282CAE1, which matures Aug. 15, 2030. It has a coupon rate of 0.625%. The price was 78.453, resulting in a yield to maturity of 3.99%. This is how it would work if I had invested $10,000:

- Cost of investment: $7,845.30

- Future interest: about $471

- Paid at maturity: $10,000

- Total return about $10,471.

Not spectacular, I admit. I think we may see better opportunities in coming weeks.

Conclusion. As the Federal Reserve nears the end of its rate-hiking cycle, it could be wise to look at stretching out the term of your Treasury investments, at least a bit. If recession strikes, interest rates are likely to fall, boosting the value of a nominal Treasury.

However, “this time could be different,” especially if inflation continues at high levels. Then the Federal Reserve would have to continue pushing rates higher. Nothing is certain.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dr, it's not clear to whom your comment addressed, nor clear (at least to me, sorry) what it's supposed to…