Just a heads up to readers: Right after 10 a.m. EDT Tuesday, the Treasury will announce the new composite rate for I Bonds issued between November 2022 and April 2023. Will the I Bond’s fixed rate go higher? We will find out … tomorrow.

Unfortunately, at that hour, I will be in a car heading down an interstate to a family-reunion vacation on Hilton Head Island, S.C. This reunion was rescheduled twice and unfortunately got moved to begin on November 1, the rate announcement day. Oh well …

I will post what I can from the car (I won’t be driving) as soon as I can tomorrow, then I will update that posting with more analysis later in the day.

Also tomorrow, we will get confirmation that the I Bond’s new variable rate will be an annualized 6.48% for six months for all I Bonds, no matter when they were issued. The fixed rate decision, however, is a great unknown. I have been saying the fixed rate should be boosted from 0.0% to 0.5%, but it could very well stay at 0.0% or go even higher than 0.5%.

In addition, we will learn if the Treasury will raise the fixed rate on Series EE Savings Bond from an embarrassingly low 0.1%, where it has been stuck since Nov. 1, 2015. The EE Bonds double in value if held for 20 years, creating an effective return of 3.53% a year. I doubt the Treasury will change the 20-year doubling term. Seems highly unlikely.

Wildly unlikely would be a Treasury decision to allow a higher purchase limit on Savings Bonds, currently $10,000 each for I Bonds and EE Bonds per person, per year. That would be huge news, but there is no indication this is coming.

See you tomorrow.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Over the last decade, I’ve been a defender of TreasuryDirect despite its dated website, awful tax forms and cryptic communications. In almost all cases, it has worked for me. Acceptable and most importantly, secure.

But now, weighed down this week by massive demand for U.S. Series I Savings Bonds, the site has repeatedly gone dead, failed to load, loaded a page or two and then stopped. Thousands of potential Treasury customers are furious, and some of them weren’t even looking to buy I Bonds. I’ve heard from people trying to place an order for a 4-week Treasury auction yesterday, but were locked out.

The Wall Street Journal reported yesterday that just in the final week of October, the Treasury issued $1.95 billion in I Bonds, more than the total for fiscal year 2021. In one year, 3.7 million new accounts were created on the site, more than the 2.4 million for the prior 10 years combined.

Why is demand so high? Because the I Bond’s variable rate will reset from 9.62% to 6.48% on Nov. 1. (The fixed rate could also change, but that is uncertain.) People who lock in an I Bond order before Nov. 1 will get 9.62% annualized for six months, and then 6.48% for six months. That adds up to a compounded return of about 8.2% over 12 months. Even if the investor sells after 12 months and takes a 3-month interest penalty, the return would be over 6.5%. That’s very attractive.

TreasuryDirect has responded to this overwhelming demand by posting this message on its homepage (viewable when you are lucky enough get to the homepage):

“We are currently experiencing unprecedented requests for new accounts and purchases of I Bonds. Due to these volumes, we cannot guarantee customers will be able to complete a purchase by the October 28th deadline for the current rate. Our agents are working to help customers who need assistance as quickly as possible.”

This message is typically cryptic, because it’s impossible to tell if it means all electronic orders are at risk of not being filled, or is it addressing issues with its customer service staff trying to answer phone calls dealing with purchases and account set ups?

Elsewhere on the site, TreasuryDirect says:

“You must complete your purchase and receive a confirmation email by October 28, 2022, at 11:59:59 PM ET. I Bonds purchased by this deadline will have an October 1st issue date. You will receive the published rate for six months (i.e., October – March).

“Due to high volumes, we cannot guarantee that your bond purchase will be completed before this deadline if your account or purchase requires additional customer support for issues such as identity verification.”

That statement seems to imply that it is people needing human customer support that are most at risk of not completing the purchase. But I’ve heard from many people with active TreasuryDirect accounts who have been able to get into the site, get all the way to the I Bond purchase confirmation page, and then have the site crash. Repeatedly. Those people haven’t completed the purchase and can’t complete the purchase. But they need to keep trying.

TreasuryDirect says you must receive a confirmation email to confirm your order has been placed.

Today — Friday, Oct. 28 — is the day TreasuryDirect originally said would be the last day to place an order to be assured of getting an October-dated I Bond and that 9.62% for six months. I had been recommending making the purchase by Wednesday, Oct. 26, but unfortunately that is the day TreasuryDirect started crashing.

What happens after Oct. 28? This is what TreasuryDirect says:

“Due to processing and payment settlement timeframes, bonds purchased in TreasuryDirect October 29 through October 31 will be issued in November. As a result, these bonds will receive the rate announced by Treasury on November 1. This rate will still be applied for the next six-months (i.e., November – April).“

What TreasuryDirect needs to do

No. 1. Commit that all I Bond orders placed by midnight today will be recognized as October-issued I Bonds. This is an electronic system, so you know when the order was placed. You need to honor your statement that Oct. 28 orders would be completed before Nov. 1.

No. 2. Have Treasury staff work this weekend to continue helping customers set up accounts and complete orders. Make sure communications are going out to customers who have completed orders. Extend that Oct. 28 deadline for all people who have made good-faith attempts to complete the purchase by Oct. 28.

No. 3. Repair your website so that this sort of problem never happens again. TreasuryDirect is the only place an investor can buy an I Bond. It needs to work, no matter the demand.

TreasuryDirect is closing down for maintenance this weekend, but that still doesn’t mean that I Bond orders completed by 11:59 p.m. won’t be accepted as an October issue. This is from a Barron’s article:

The Treasury’s website will undergo maintenance this weekend after record demand for series I inflation-linked savings bonds strained the system. Work on the TreasuryDirect website will start at 12 a.m. Saturday and continue until 11:59 p.m. Sunday Eastern Time.

During that period, individuals won’t be able to use the account management system that allows purchases of I Bonds. The rest of the site will be up and running.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

With this strategy, you can bypass the $10,000 per person purchase limit, but there are potential drawbacks.

By David Enna, Tipswatch.com

Throughout this year, I have read with — at first, disbelief, and later, fascination — as devotees of U.S. Series I Savings Bonds discovered and successfully exploited a TreasuryDirect “gift box strategy” to accumulate I Bonds beyond the $10,000 per person yearly purchase limit.

Although the strategy is legit and perfectly legal, I haven’t written about it and I don’t intend to use it. But a lot of people have asked me about it. If you intend to use this strategy, I’d advise completing the process on TreasuryDirect by Wednesday, Oct. 26, if you are aiming to lock in the current 9.62% interest rate for a full six months, and then 6.48% for the next six months.

Update:The TreasuryDirect site was overwhelmed by I Bond demand Wednesday and almost all users experienced very slow loading pages, or no loads at all. I recommended making your I Bond transactions on Wednesday for this very reason, to avoid this sort of pitfall. Making a purchase on Thursday will be fine, and Friday will also be likely to be OK. Let’s hope the site returns to normal.

Friday morning:TreasuryDirect’s opening page is now loading. It took me two times but I was able to log into my account. Good luck to all.

Harry Sit of the TheFinanceBuff.com was the first to write about this strategy on Dec. 27, 2021, in an article titled “Buy I Bonds as a Gift: What Works and What Doesn’t.” When people ask me about the gift box, I point them to this article, which was well researched and thorough. So, go read that article if you don’t know about the strategy.

Another article was just posted this week by Jeremy Keil, a financial adviser who was an early advocate of the current I Bond surge (and has written a guest post for this site). His article is titled: “Buy more than $10,000 in Series I Savings Bonds through gifting with your spouse“. Keil, who recently completed an I Bond gift box purchase, includes links to TreasuryDirect content explaining how the gift box works. He details a strategy for a couple purchasing $60,000 in I Bonds before the end of October, with $20,000 being delivered in 2023 and $20,000 in 2024.

When you place an I Bond into the gift box, it begins earning interest in the month of purchase, just like any other I Bond, and continues earning interest just like any I Bond. However, this money is no longer yours. It belongs to the recipient of the gift.

The purchase does not count against your purchase limit for that year. It will count against the purchase limit for the recipient, in the year it is granted.

Gift purchases are limited to $10,000 for each gift, but you can make multiple gift purchases of $10,000 for the same person. But the recipient can only receive one $10,000 gift a year, and that gift counts against their purchase limit for that year.

You must provide the recipient’s name and Social Security Number when you buy a gift. The recipient doesn’t need to have a TreasuryDirect account … yet. Only a personal account can buy or receive gifts. A trust or a business can’t buy a gift or receive a gift.

“I Bonds stored in your gift box are in limbo,” Harry Sit notes in his article. “You can’t cash them out because they’re not yours. The recipient can’t cash them out either because the bonds aren’t in their account yet.”

The recipient will need to open a TreasuryDirect account to receive the I Bond. Once it is delivered, the money is the recipient’s, who can then cash out or continue to hold the I Bond.

Here is TreasuryDirect’s video explaining the step-by-step process to complete a gift box purchase:

In his article, Harry Sit also provides a very useful step-by-step guide to completing a gift-box purchase.

Would this strategy trigger a gift tax?

Sit notes there is no limit on how much you can give your spouse as a gift, so this strategy works especially well for cross-gifting: Spouse 1 to Spouse 2 … and Spouse 2 to Spouse 1, each using their separate TreasuryDirect accounts. Rules are more complicated for gifts to a non-spouse, so refer to Harry’s article for more detail.

What are the potential negatives to this strategy?

Placing $10,000 in the gift box puts that money in limbo, awaiting future delivery. It is no longer your money, and it really isn’t the recipient’s money either until the gift is delivered. So if you stack up multiple $10,000 purchases for gifting well into the future, the potential downside is that your circumstances could change.

Also, what if the I Bond’s fixed rate rises dramatically in November 2022 or May 2023? You would probably want to bypass delivering the gift I Bond beyond 2023 to take advantage of the higher fixed rate, which is highly desirable. That means you would have to wait until the next time the I Bond’s fixed rate falls to 0.0%.

Sit also warns about forgetting about the gifts. His advice: “If you’re intentionally pre-purchasing gifts to take advantage of temporarily high interest rates, tell the recipient you’re holding a gift. Set recurring calendar reminders to tell yourself and the recipient you still have undelivered gifts in the gift box.”

What if the gift recipient dies?

When you register the gift, you can name a second owner or beneficiary for the I Bond. Sit says, “If the gift recipient dies before you deliver the gift, the designated second owner or beneficiary will inherit your gift. You can’t name yourself as the second owner of the gift but you can name yourself as the beneficiary of the gift.”

If you die before granting the gift, the recipient still owns it and will be able to claim it through TreasuryDirect.

Why didn’t I use this strategy?

I admit to being quite skeptical at first that TreasuryDirect would allow multiple, stacked $10,000 purchases in one account. But by all accounts, it has been working fine (except for a brief outage recently after a site update). I thought about doing this, but opted to just stay with my plan of buying $10,000 a year in our two accounts, every year, and hoping for a higher fixed rate in 2023 and beyond.

But is it a sound strategy? Yes, I think it is, especially for short-term investors interested in locking in a high rate of return over the next 12 to 15 months (taking into account the three-month interest penalty for redemptions within 5 years).

Why complete the gift purchase by Wednesday?

Thursday would probably be fine, but you want to make sure to complete any I Bond transaction early enough to ensure that TreasuryDirect logs it as an October 2022 purchase, which means you will receive 9.62% for a six months, and then 6.48% for six months. It’s wise to give TreasuryDirect a couple of business days to complete any transaction.

Feedback?

If you decided to use the I Bond gift strategy, feel free to post about your experience and thoughts in the comments section below.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Still, real yield was lower than expectedas inflation expectations surged higher.

By David Enna, Tipswatch.com

The Treasury’s offering of $21 billion in a new 5-year Treasury Inflation-Protected Security resulted in a mixed bag for investors: The real yield of 1.732% hit a 15-year high and was quite positive, but that yield was a bit below market levels right up to the auction.

This is CUSIP 91282CFR7, and the auction result set its coupon rate at 1.625%, the highest coupon rate for any TIPS of this term since an originating auction on April 24, 2007. Buyers paid an adjusted price of about $99.48 for about $99.98 of accrued value and interest. This TIPS will have an inflation index of 0.99982 on the settlement date of Oct. 31.

This is the first 4- to 5-year TIPS auction to result in an adjusted price below $100 since April 26, 2010. The price means than a person who bought $10,000 in par value for this TIPS paid about $9,948 for about $9,982 in accrued value, plus a very small amount of accrued interest, about $7.

So all in all, this is a very positive result for investors. It’s baffling, though, that the Treasury had estimated the real yield of a 5-year TIPS at 1.89% at yesterday’s market close, and the most recent TIPS of this term had been trading all morning on the secondary market with a real yield of about 1.85%.

One factor is that inflation expectations seemed to surge higher, which would indicate strong demand for this TIPS, even though the bid-to-cover ratio was a mediocre 2.38. At yesterday’s market close, the Treasury estimated the five-year inflation breakeven rate at 2.46%, but this auction resulted in a breakeven rate of 2.67%. That’s a big move higher and would explain a lot of the gap between yield and expectations.

Also interesting is that non-competitive bids — made by small investors like us — totaled $256 million, nearly double the bids of $131 million for a new 5-year TIPS issued in April. But that surge higher probably had zero effect on a $21 billion offering.

Here is the trend in the 5-year real yield since the beginning of 2020, showing the remarkable surge higher after the Federal Reserve announced tightening intentions in March 2022:

Inflation breakeven rate

With a 5-year Treasury note trading at 4.40% at the auction’s 1 p.m. close, this TIPS gets an inflation breakeven rate of 2.67%. As I noted earlier, the 5-year inflation breakeven rate has been lingering around 2.45% for several days. A 22-basis-point jump is quite a move, and it indicates that investor demand for inflation protection is increasing.

Here is the trend in the 5-year inflation breakeven rate since January 2020:

Reaction to the auction

Source: Yahoo Finance

Over the last year, we’ve had a lot of upside surprises at the close of TIPS auctions, but this one was the reverse. While the real yield of 1.723% was a 15-year high and very attractive, it came in a little below expectations. (My expectations, anyway.) As you can see in this chart, the net asset value of the TIP ETF, which holds the full range of maturities, actually declined after the auction’s close at 1 p.m. That indicates higher yields.

And now, at 1:48 p.m., the real yield of the most recent TIPS traded on the secondary market has surged to 1.91%. Doesn’t make a lot of sense. I’ll look around for a logical explanation, but I don’t expect to find one. The bond market can humble you. It’s always a good reminder: never assume anything.

But I refuse to be disappointed with my purchase of a 5-year TIPS with a real yield at a 15-year high of 1.732% and a coupon rate also at a 15-year high of 1.625%. That’s a significant real yield after nearly a decade of ultra-low yields. And it means, most likely, that this TIPS will earn a return that will beat inflation, after taxes, if you are holding it in a cash or traditional tax-deferred account.

“(T)he U.S. Treasury auctioned $21 billion in five-year Treasury Inflation-Protected Securities, with the high yield of 1.732% stopping short of the expected rate at the bid deadline, which suggested increased demand.

“Analysts said demand was fueled by strong participation from direct bidders. According to investment bank Jefferies, direct bidders took down 17% of the auction, which is about six percentage points higher than the average of the last four auctions. In dollar terms, Jefferies said this is the biggest takedown since December 2019.

FYI, the Treasury defines direct bidders as: “Non-Primary dealer submitters bidding for their own house accounts.” And another worthless definition, from Investopedia: “Direct bidders include primary dealers, hedge funds, pension funds, mutual funds, insurers, banks, governments and individuals.” Doesn’t that include just about everyone? More research is needed.

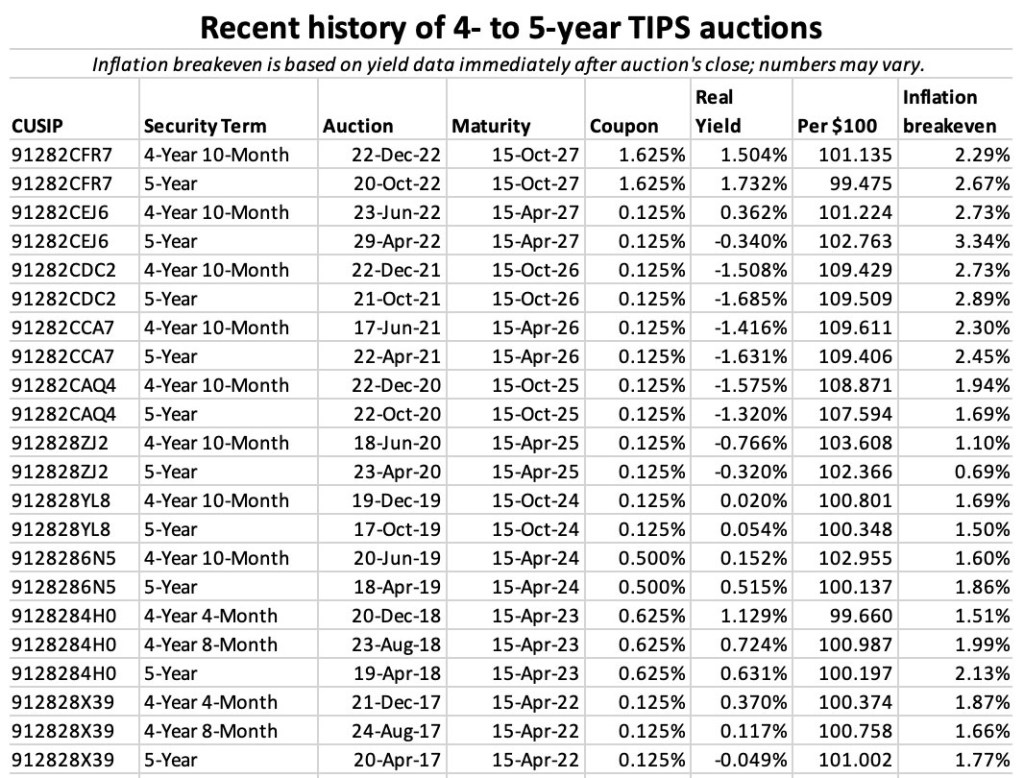

CUSIP 91282CFR7 will be reopened at auction on Dec. 22, 2022. Here’s a history of auctions of this term since 2017, showing the long string of negative real yields, including the record low real yield of -1.685% just one year ago.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

The U.S. Treasury on Thursday will offer $21 billion in a new 5-year Treasury Inflation-Protected Security, CUSIP 91282CFR7. This auction will be so unusual in so many ways — based on the last decade of TIPS auctions — that I am calling it a “unicorn,” rarely seen and rarely captured. But here it comes.

Just how unusual? Let’s take a look:

This TIPS is likely to generate a real yield to maturity of about 1.80%, the highest for this term since October 2008, when a reopening auction got a real yield of 3.270% amid the depths of the U.S. financial crisis.

One year ago — one year! — a new 5-year TIPS was auctioned with a real yield of -1.685%, the lowest in history for any TIPS of any term. That is an incredible 348 basis points lower than Thursday’s likely result.

The coupon rate could end up being 1.75%, which would be the highest for this term since April 2007. In fact, the last 12 new and reopening auctions of this term have had coupon rates of just 0.125%. No TIPS auction of any term has had a coupon rate at 1.75% or above since a 30-year auction in February 2011, more than 11 years ago.

This new TIPS will have an inflation index of 0.99982 on the settlement date of Oct. 31, which means it is highly likely to have an adjusted price of less than or close to $100 par value. That hasn’t happened for a new issue of this term since April 2010.

The reason the adjusted price could drift slightly above $100 is accrued interest, which has been negligible through all those auctions with 0.125% coupon rates. Investors will be purchasing 16 days of accrued interest on the settlement date of Oct. 31. If the coupon rate is 1.75%, accrued interest would be about 7 cents per $100, which could cause the adjusted price to rise slightly above $100. But this isn’t accrued principal or par value, and the interest will be returned to the investor at the first coupon payment on April 15, 2023.

The auction size of $21 billion is the largest in history for a 5-year TIPS. In October 2019 the Treasury offered $17 billion in this term, which rose to $19 billion in 2021 and now $21 billion in 2022. That’s an increase of 24% in auction size in three years.

So, what’s not to like? Thursday’s auction of CUSIP 91282CFR7 is likely to generate a historically high yield, with a high coupon rate, at a lowish cost to par value. Meanwhile, the Treasury is pumping up the size of the offering, which should help keep the real yield high. (But I always note: Things can change.)

Definition: The “real yield” of a TIPS is its yield above official future U.S. inflation, over the term of the TIPS. So a real yield of 1.80% means an investment in this TIPS will exceed U.S. inflation by 1.80% for 5 years. If inflation averages 2.5%, you’d get a nominal return of 4.3%, pretty much on par with a nominal U.S. Treasury. But if inflation averages 4.5%, you’d get a nominal return of 6.3%.

Things can change by Thursday, but if the real yield holds at 1.80%, the coupon rate would be set at 1.75% and the unadjusted price would be somewhere around $99.75 for $100 of par value. But, because the inflation index is less than 1.0, the adjusted price will probably be something like $99.75 for $99.98 of accrued value (par value would remain at $100). All of this is a rough estimate, and that doesn’t include the accrued interest. The key is that investors at Thursday’s auction will be paying slightly less than par value.

For the buy-and-hold-to-maturity investor, this TIPS is a prize. The term is short. Sure, yields could continue rising higher, but you will have locked in a historically strong real yield over the next five years.

Here is the trend in 5-year real yields over the last 13 years, showing that the current real yield has surpassed the highest level of the Federal Reserve’s last tightening cycle, which peaked late in 2018. It’s a bit ominous, though, to see how quickly real yields declined in 2019 when the Fed changed course:

Click on the image for a larger version.

Inflation breakeven rate

With a nominal 5-year Treasury note now yielding 4.25% (which I think is attractive, by the way) a 5-year TIPS currently would have an inflation breakeven rate of 2.45%, which seems reasonable at a time when U.S. inflation is running at 8.2%, and only inching lower over the last two months. Historically, though, that is a high number and would indicate that a 5-year TIPS is expensive versus a nominal Treasury. Here is the trend in the 5-year inflation breakeven rate over the last 13 years:

Click on the image for a larger version.

This trend-line chart ends on Thursday, Oct. 13, the last day Fred had data. But the breakeven rate popped 10 basis points higher on Friday, possibly influenced by the release of a University of Michigan report on consumer attitudes. That report found U.S. consumers expect inflation to run at 2.9% over the next 5 years, up from 2.7% last month.

As the chart shows, however, market expectations of 5-year inflation have fallen fairly dramatically from a high of 3.59% on March 25, 2022. In span of 2009 through the post-pandemic surge higher in March 2020, the previous high was 2.45% on April 19, 2011, matching today’s number. Back in April 2011, U.S. inflation was running at 3.2%, versus 8.2% today.

Yes, I think a nominal 5-year Treasury yielding 4.25% is attractive, but I would still rather invest a 5-year TIPS with potential for a decent return, along with insurance against unexpectedly high inflation in the future. (Unexpected inflation is what we are experiencing today.)

Final thoughts

Unless market conditions change dramatically in the next few days, CUSIP 91282CFR7 is going to be an attractive purchase. If the real yield to maturity holds at around 1.80%, it has a 180-basis-point yield advantage over the U.S. Series I Savings Bond, if both are held for five years. But the TIPS lacks the I Bond’s sexy 9.62% annualized return for six months — I Bonds get that advantage because they track trailing inflation numbers. Nevertheless, over the next 5 years, this TIPS is likely to out-perform an I Bond with a fixed rate of 0.0%.

If you are considering investing in this TIPS, remember that things can change. You can track the Treasury’s estimate of the real yield of a full-term 5-year TIPS on its Real Yields Curve page, which updates after the market close each weekday. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline. I’ll be posting the results soon after the auction closes at 1 p.m. EDT.

Thursday’s auction will be the first of four consecutive monthly auctions that are likely to be very attractive:

Oct. 20, new 5-year TIPS

Nov. 17, 10-year TIPS reopening

Dec. 22, 5-year TIPS reopening

Jan. 19, new 10-year TIPS

And of course, on January 1, you can again purchase I Bonds up to the $10,000 per person limit.

Here is a history of recent 4- to 5-year TIPS auctions, showing the long string of recent auctions with a coupon rate of 0.125%. Thursday’s result should be much higher:

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dr Matt....Sell and buy options