By David Enna, Tipswatch.com

Update: This TIPS matured Jan. 15, 2023. How did it work as an investment?

Just about every month, I get emails or comments from readers pointing out what appears to be extremely attractive real yields on very short-term TIPS — especially those maturing in less than a year. My usual response is that these real yields get highly exaggerated as maturity nears and only one coupon payment remains.

I’ll admit I don’t fully understand the mechanics of the quoted real yields when TIPS are down to the final months. But I assume — and I am pretty sure I am right — that the market is pricing these TIPS correctly. This month, we have another example, and I decided to take a walk-through look at this possible investment, CUSIP 912828UH1:

CUSIP 912828UH1 was originally issued as a 10-year TIPS on January 15, 2013. I wrote about this TIPS back then, believe it or not. It was in the early years of misery for TIPS investors, with this TIPS getting a real yield of -0.630% and a coupon rate of 0.125%. Now, as it is approaching maturity, it has built up an inflation accrual index of 1.28372 as of September 1. And on Thursday it was trading with an “apparent” real yield of 4.047%, according to the Wall Street Journal’s closing statistics.

So, an investor in this TIPS will be purchasing 28.3% of additional principal above par, and that principal is not protected against deflation in future months. In fact, the principal balance of this TIPS will decline 0.01% in September, based on non-seasonally adjusted inflation in July. We could see more declines in October and November, if falling gas prices create deflationary numbers for August and September, which seems possible.

I went onto Vanguard’s trading platform and entered a $10,000 purchase of this TIPS (for example purposes only — I didn’t complete the purchase). Here is what the order sheet showed Thursday afternoon:

Note that a purchase of $10,000 of par value will cost an investor $12,660.82. Here’s a rundown on the basics of that investment, and note that my total cost is off from Vanguard’s by 5 cents, and I have no idea why:

Because of the discounted price, an investor is getting $12,837 of principal from a $12,661 investment, which is attractive. But just how attractive? It’s hard to say, because the final payment at maturity on January 15, 2023, is going to depend on how hot or cold inflation runs through November. The Treasury market is speculating that inflation will decline or at least remain muted through the end of the year, which could be accurate. Or could this be recency bias based on the recent collapse in oil prices?

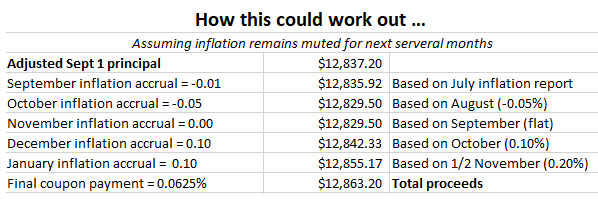

Here is my speculation on a “muted inflation” scenario for this TIPS, with inflation falling -0.05% in August, then remaining flat in September, rising 0.1% in October and then 0.2% November. (This TIPS will get an inflation adjustment of 15 days from November inflation in its final month.)

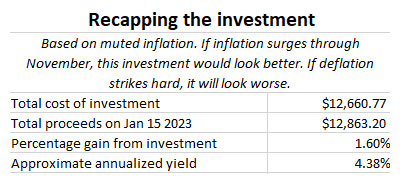

If things work out this way — pure speculation — the investor on September 1 will have invested $12,660 and will get a return of about $12,863 on January 15.That’s a gain of $203, which isn’t shabby for a 4 1/2 month investment. It’s an annualized return of about 4.38%. Not quite up to I Bond standards, but better than similar nominal Treasury yields, which are hanging just above 3%.

Based on this rough look at CUSIP 912828UH1, it seems like a reasonable investment, given the discounted price. The investor picks up the risk of the 28% inflation accrual, which could get depleted if deflation becomes a “thing” in the next several months. My example may be too optimistic. Who knows? The market is clearly signaling a belief that inflation will be very low, or negative, through November.

Would I buy it? No, I am not interested. It’s just too complex to be worth the trouble. This example was simply meant to demonstrate the “logic” of today’s market, which might be logical, or possibly crazed.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas... a rarity on the modern www. It…