I’ve been gone three weeks. Did anything happen?

By David Enna, Tipswatch.com

Yes, I am now back home after a three-week adventure in Eastern Europe — Czech Republic, Slovakia, Hungary and Romania. In all, adding in a recent trip to southern Italy and Sicily, I have been in Europe for six of the last 10 weeks. It seems like a lot has happened in those three months, right?

One thing that didn’t happen: No one in my small traveling groups — 12 in Italy and 6 in Eastern Europe (down to 4 in Romania for an optional extension) — contracted Covid, which was a huge relief. You have to take a Covid test 24 hours before flying to the United States. We all got to go home, but we heard of many travelers forced to extend their vacations by at least five days in isolation.

Some impressions of these formerly Soviet-dominated lands in Eastern Europe:

- In Italy, which learned some harsh Covid lessons in 2020, nearly everyone wore face masks indoors — churches, museums, even restaurants until seated. A few weeks later in Eastern Europe, we saw close to zero face masks anywhere, even in Vlad the Impaler’s very crowded castle in Transylvania, attacked by hordes of school children. (Our group did wear face masks in crowded indoor places, but we didn’t see many others.)

- These Eastern European countries are all members of NATO and the European Union. The atmosphere and spirit is totally Western. People are heading to prosperity, loving newfound freedoms, wearing colorful and fashionable clothes, driving on traffic-filled streets. Always very friendly. Russia is almost universally considered the enemy. English is every young person’s second language.

- Nearly everyone in all the countries complained of corrupt governments, a legacy of the restrictive communist systems. “It’s going to take us another 30 years to develop a rule of law,” one young women told me in Brasov, Romania. “It will take Russia at least another 100 years, or more.”

- Hungary, a country I’ve visited twice before, is bucking against the European Union’s actions against Russia, mainly to get concessions on gas and oil shipments. Hungary’s nationalistic government has some grievances against Ukraine and Romania, and that is troubling. (Hungarian-speaking communities survive in both countries, and Hungary still complains about its borders.)

- Press freedoms are also under attack in Hungary, a troubling trend. Many of the dissident news outlets have shut down, not by direct action by the government, but from lack of funds.

- When the topic turned back to the United States, almost everyone asked us: “Why are there so many guns in your country?”

- These should all be tourist meccas, with magnificent UNESCO-protected towns dotting the landscape. but the combination of lingering Covid and the war in Ukraine is scaring tourists off. Our guide in Romania told us that Overseas Adventure Travel (our trip company) had planned for 40 tours this summer. Only two are now scheduled, and our group had only four people.

- Tourists should not fear. These are safe places full of friendly people who appreciate American travelers. The Ukraine war is on people’s minds, but is not any kind of threat right now.

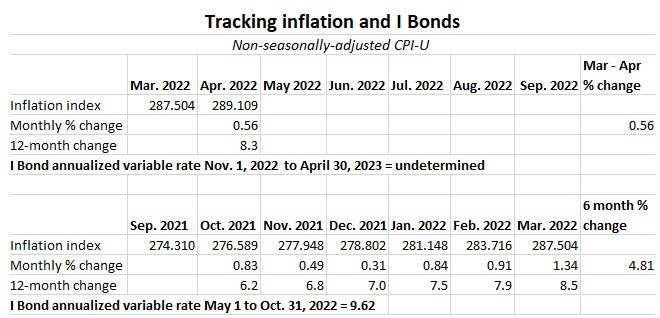

However … Inflation is a huge problem in these countries, which are suffering from soaring gas, food and housing prices. Grocery stores, however, are well stocked and life is going on. Here are some recent inflation numbers, much worse that the U.S. rate of 8.3%:

- Czech Republic, annual inflation of 14.2% (as of April)

- Slovakia, annual inflation of 11.8% (April), an all-time high

- Hungary, annual inflation of 10.7% (May)

- Romania, annual inflation of 13.7% (April), highest since Feb. 2004

The war in Ukraine has accelerated these inflationary trends, but inflation is clearly a global problem that is going to be difficult to get under control.

Since I’ve been gone …

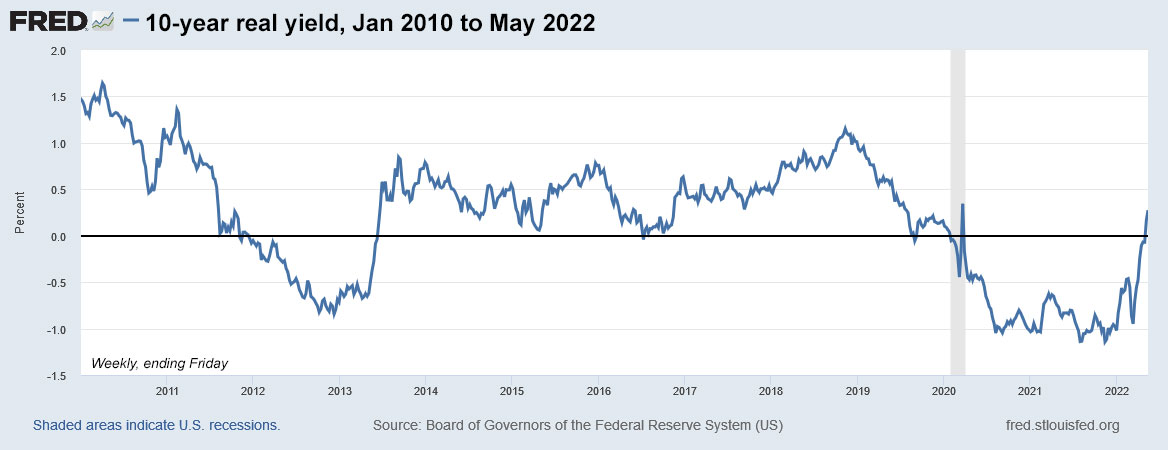

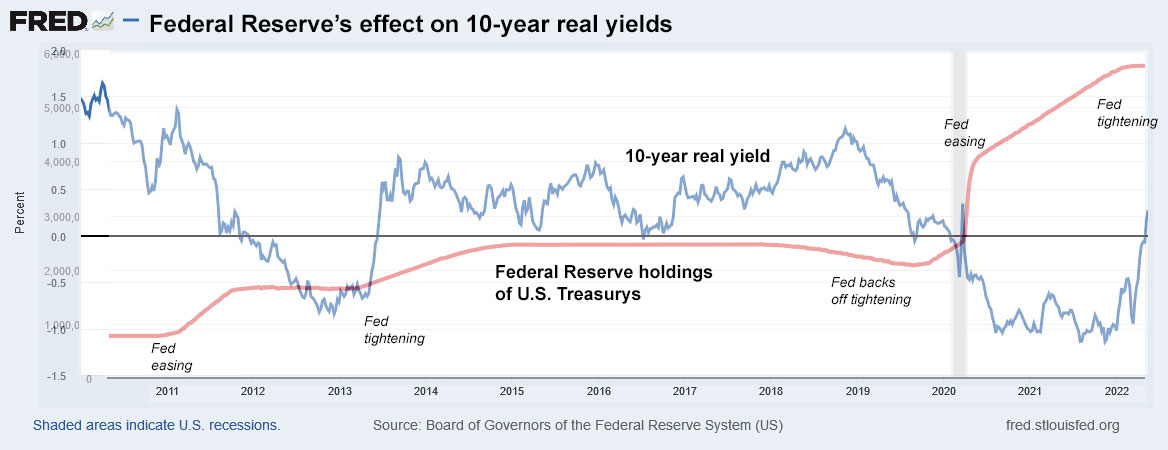

I left for Prague on Tuesday, May 17, and it seemed from a distance like financial markets started falling apart immediately. But I really wasn’t paying attention, other than to write my report on the April inflation numbers. In actuality, not much to to see here. The S&P 500 started that period at 4,088 and closed Tuesday at 4,156. All good. Here’s what happened to real yields in those three weeks:

- The 5-year real yield started at -0.12% and closed Tuesday at -0.04%

- The 10-year real yield started at 0.27% and ended at 0.25%.

- The 30-year real yield started at 0.65% and ended at 0.58%.

So, the yield curve flattened, and that is a sign that recession fears are increasing and also should mean that inflation fears are subsiding, a bit. The 10-year inflation breakeven rate now stands at about 2.76%, very close to where it was on May 17.

Nominal Treasurys are starting to get interesting, with the 13-week Treasury now yielding 1.26% and the 1-year at 2.26%. Is your bank paying 2.26% for a 1 year CD? Probably not. Treasurys are the way to go right now for short-term savings. The 5-year Treasury note slipped above 3% on Monday. It could be worth a look, too.

Coming up …

The May inflation report will be released Friday at 8:30 a.m. EST. The consensus estimate is for monthly inflation to run at 0.7% and year-over-year at 8.2%. These numbers — influenced heavily by rising energy costs — remain stubbornly and dangerously high.

I’ll be posting my inflation analysis, and its effect on TIPS and I Bonds, on Friday morning.

Also, a 5-year TIPS reopening auction is coming up on June 23. That auction could be attractive, and I will be posting a preview article on Sunday, June, 19.

So, yes, I am back.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas... a rarity on the modern www. It…