Are declines in your TIPS funds stressing you out? Today’s article is a guest offering from Adam Collins, a Tipswatch reader and flat fee financial adviser. He explains why TIPS are needed in a portfolio, and which TIPS funds might work best.

By Adam Collins, Eversight Wealth

Inflation and higher rates wrecked bond funds in 2022. Treasury Inflation-Protected Securities are supposed to outperform in this environment, yet most TIPS funds are down.

Did TIPS fail? Or did some investors pick the wrong fund?

This post explains:

- How TIPS funds can have massively different performance.

- What surging real yields mean for future TIPS returns.

- Why passive investors need more inflation protection.

TIPS performance explained

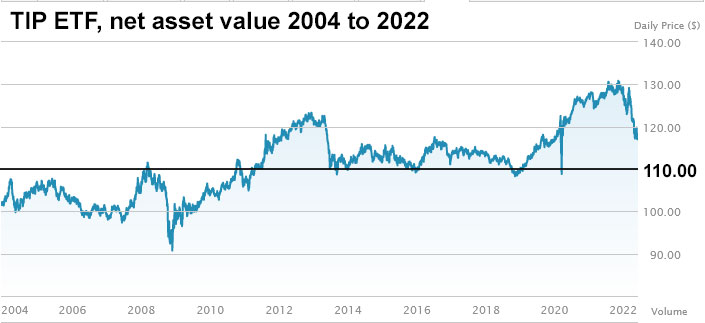

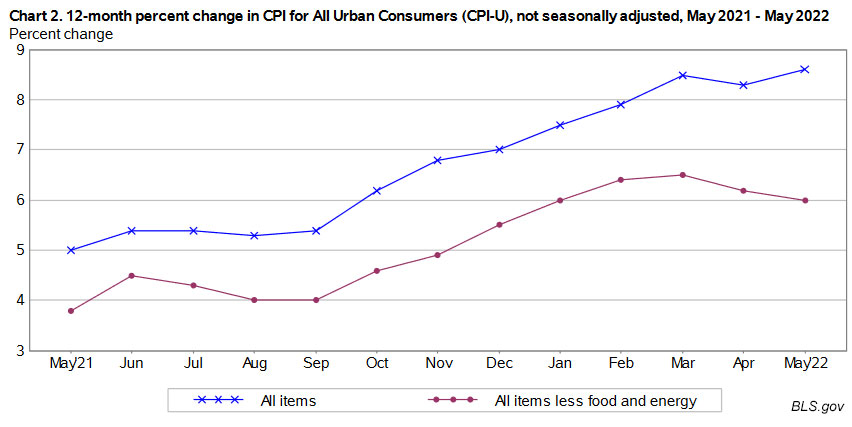

Inflation has increased 8.6% over the past year. TIP, the most popular inflation-protected fund with $30 billion in assets, fell 4%.

Here’s how that loss could have been avoided.

Besides inflation adjustments that increase their prices, TIPS also pay interest. This interest rate is a real yield because it’s how much the bond will return net of inflation. So a real yield of 1% means you will earn 1% above future inflation — but only if you hold the bond to maturity.

In the short-term, TIPS prices move opposite to yields. TIPS trailed inflation in 2022 because price declines due to rising rates exceeded inflation adjustments.

TIPS funds have different sensitivities to changing yields. Duration measures this and ranges from 3 for funds that own short-term bonds (like VTIP) to 20 for long-term funds (like LTPZ). For VTIP, short-term returns are more linked to inflation and less to yield changes.

In 2018, Vanguard found that short-term TIPS are more correlated to unexpected inflation. This aligns with performance in 2022.

Future Outlook for TIPS

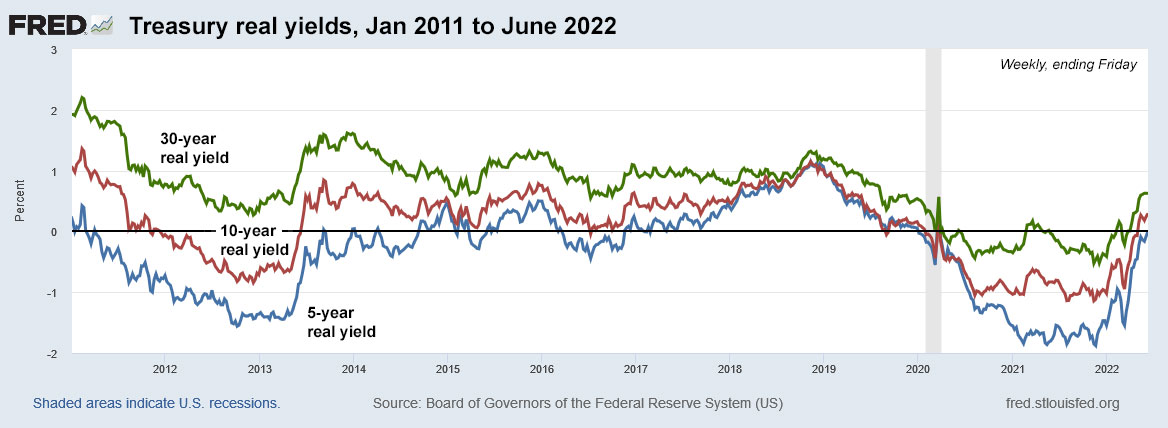

Rising real yields hurt short-term returns but benefit long-term investors. TIPS now offer more inflation upside despite the increase in inflation fears.

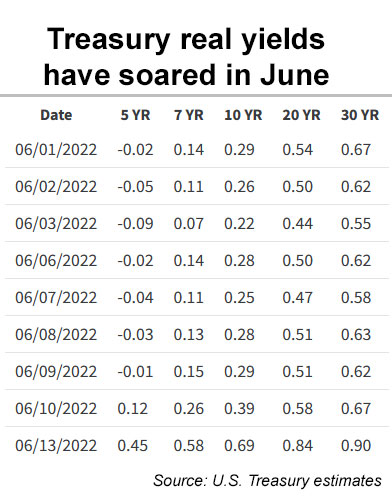

A 5-year TIPS bought today will return future inflation plus 0.36% per year, based on Friday’s market close. Compared that to last June’s yield of inflation minus 1.6% per year.

Tighter correlation to unexpected inflation is the main reason I prefer short-term TIPS, but they’re not without downsides. Long-term TIPS offer higher yields and lower breakeven rates. For example, the 5-year breakeven is 2.8% and the 30-year breakeven is 2.5%. This means there’s a higher inflation hurdle for short-term TIPS to outperform regular short-term bonds.

Retirees taking withdrawals are vulnerable to a long-term TIPS fund experiencing a bad sequence of returns like in 2022. This is another advantage of short-term TIPS: their lower volatility can decrease sequence risk and increase the odds of a sustainable retirement.

Passive Investors Need Inflation Protection

Nobody knows if inflation will keep rising. Expert predictions are often inaccurate, so I don’t have conviction in anyone’s ability to forecast inflation.

Even though inflation is unpredictable, investors should prepare for it. Yet TIPS are often missing from bond portfolios I review.

Passive bond funds tracking Bloomberg’s U.S. Aggregate Bond Index, including Vanguard’s $286 billion total bond fund, exclude TIPS. Now down 13% from its highs, the index is in its largest ever drawdown. TIPS could have helped.

I hope the next decade doesn’t evolve like the inflationary 1970s. But if it does, investors should consider investments correlated to unexpected inflation like short-term TIPS.

Summary

- Rising yields hurt TIPS prices. Short-term funds are less affected by yield changes and more correlated to inflation.

- Many passive bond funds exclude inflation-protected bonds.

- Higher real yields make today a great time to consider TIPS.

P.S. Want a deeper dive on TIPS? I wrote a 5-part series on them.

About Adam Collins

Adam Collins is a flat fee investment advisor. Through his company Eversight Wealth, he helps people build diversified portfolios, create a financial plan, and save money with a flat advisory fee. Eversight manages $75 million for 35 clients in 13 states and offers free consultations. Here are links to more info on their services and about Adam.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thank you Fred Bloggs for this coherent analysis, without undertones of personal agendas... a rarity on the modern www. It…