I am a customer of the Pentagon Federal Credit Union, also known as PenFed, and I jumped happily aboard when it offered an above-market 3% 5-year CD in December 2013 and January 2014. But since then its CD rates have dipped to U.S. market levels, which are very low.

Then I got this offer in an e-mail from PenFed yesterday:

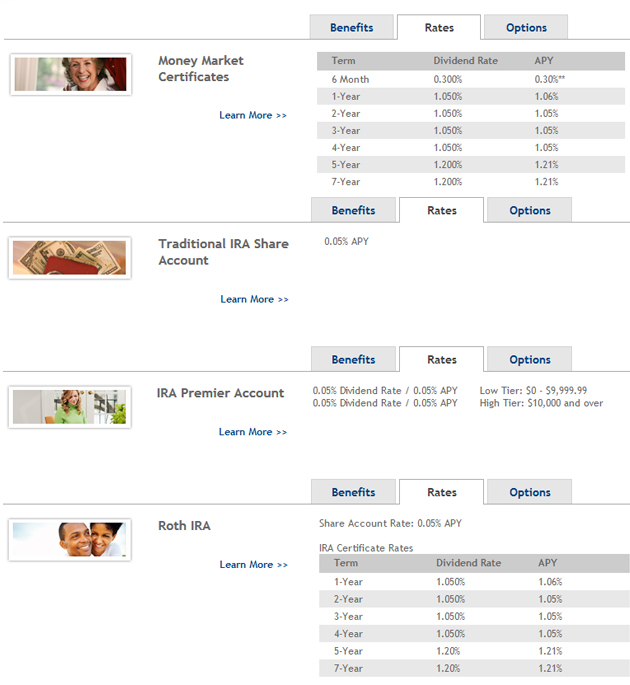

PenFed’s offer requires just a $1,000 investment for a 1-year CD, paying 1.06%. Early withdrawal forfeits six months of interest payments. That’s good; but not wildly good. The national average for a 1-year CD is 0.24%, but BankRate.com lists several institutions offering 1.10% today.

PenFed’s offer requires just a $1,000 investment for a 1-year CD, paying 1.06%. Early withdrawal forfeits six months of interest payments. That’s good; but not wildly good. The national average for a 1-year CD is 0.24%, but BankRate.com lists several institutions offering 1.10% today.

But here’s what’s intriguing about PenFed’s ‘promotional rate.’ That 1.06% offer is placed on every PenFed CD from 1 to 4 years, and bumps up to only 1.21% for 5- and 7-year. Here is rate information from its Website:

My conclusion is that PenFed expects to sell only one thing: 1-year CDs. There would be no reason for customers to accept that 1.05% rate on a 2-year, 3-year, 4-year CD, or just slightly higher on a 5-year or 7-year CD.

My conclusion is that PenFed expects to sell only one thing: 1-year CDs. There would be no reason for customers to accept that 1.05% rate on a 2-year, 3-year, 4-year CD, or just slightly higher on a 5-year or 7-year CD.

Consider this: A 5-year traditional Treasury is paying 1.79% today. That is 58 basis points higher than PenFed’s 5-year and 7-year CDs. It makes no sense; except to conclude that PenFed is pushing customers toward a 1-year CD.

Treasury yields are on the move

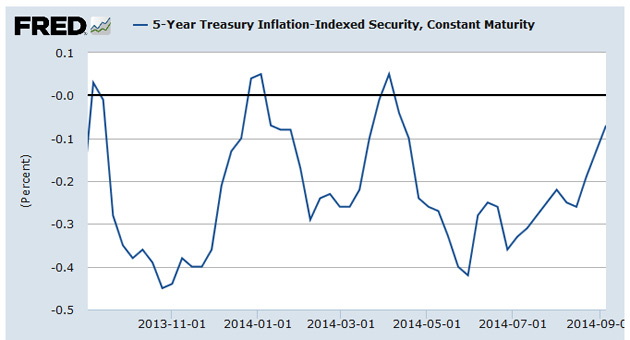

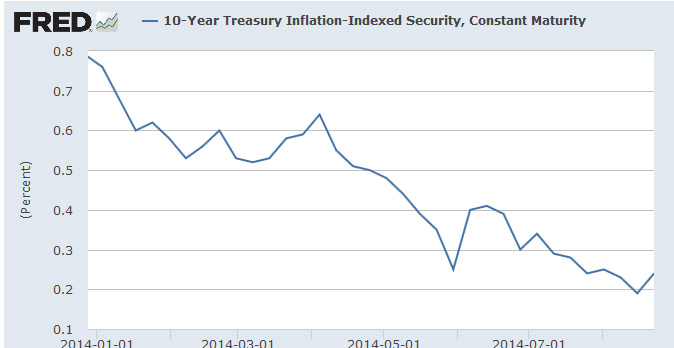

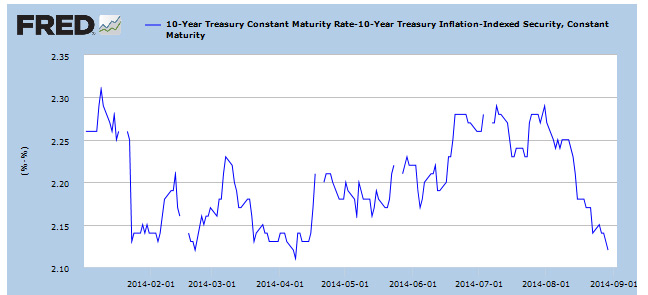

PenFed is demonstrating the ultimately flat yield curve, but in recent days yields across the Treasury market have been rising. This is a trend worth watching.

For example, the 5-year TIPS yield dropped to -0.28% on Aug. 15, but has since risen to 0.10%, based on the Treasury’s Real Yield Charts. This is the first time since April that the 5-year yield has moved into positive territory. Here’s a one-year chart, minus the last few days because the St. Louis Fed’s data has some lag time:

In reaction to rising yields, the price of the TIP ETF has been declining — very conveniently (!) since I posted Why TIPS aren’t a good buy right now: A story in charts on Sept. 4. Here’s the 5-day chart since Sept. 4:

In reaction to rising yields, the price of the TIP ETF has been declining — very conveniently (!) since I posted Why TIPS aren’t a good buy right now: A story in charts on Sept. 4. Here’s the 5-day chart since Sept. 4:

Long way to go to $110, which is still my target/prediction for when TIPS become more appealing. We probably won’t be seeing that anytime soon, but we can hope. Because I want to be a net buyer of TIPS, I am cheering for higher yields.

Long way to go to $110, which is still my target/prediction for when TIPS become more appealing. We probably won’t be seeing that anytime soon, but we can hope. Because I want to be a net buyer of TIPS, I am cheering for higher yields.

Dr, it's not clear to whom your comment addressed, nor clear (at least to me, sorry) what it's supposed to…