The U.S. Treasury announced today it will reopen CUSIP 912828B25 in a May 22 auction, creating a 9-year, 8-month Treasury Inflation-Protected Security with a coupon rate of 0.625%. Noncompetitive bidding closes at noon and competitive bidding ends at 1 p.m.

Read the announcement.

What to expect. Since this TIPS currently trades on the secondary market, we can get a pretty good idea of its yield to maturity, which will be set by the auction bidding. It was first auctioned on Jan. 23 with a yield of 0.661%, plus inflation. It was reopened March 20 with a yield of 0.659%. Since then, however, Treasurys have rallied and yields have declined.

- Bloomberg’s Current Yields shows this TIPS trading today with a yield of 0.29% and a price of about $103.18 per $100 of value.

- The Wall Street Journal‘s chart of TIPS closing prices shows that this issue closed yesterday with a yield of 0.350% and a price of about $102.62.

- The Treasury’s Daily Yield Curve site estimates that a TIPS with a full 10-year maturity is yielding 0.37%.

With that information, I’d say if the auction were today it would probably go off with a yield of about 0.32%, plus inflation, which is well below the coupon rate of 0.625%. That means buyers will have to ‘pay up’ to get that coupon rate bonus, probably somewhere around $102.75 per $100 of value.

The Treasury market has had a fairly strong rally this year, narrowing some of the gains in yield we saw beginning in mid-2013. This chart shows how the much yields have fallen since the beginning of 2014:

The upper two lines show the yield curve for nominal Treasurys and the lower two lines show the yield curve for TIPS, where the shortest maturity at auction is 5 -years.

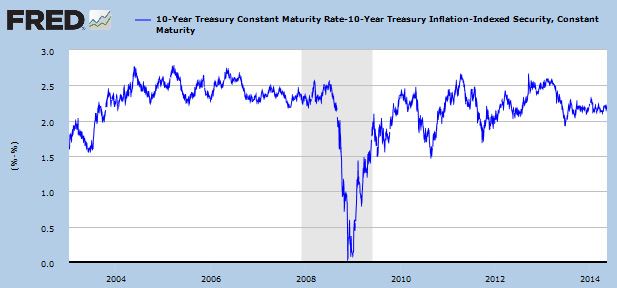

Inflation breakeven rate. Looking at the inflation breakeven point can give you an idea if TIPS are ‘expensive’ or ‘cheap’ versus a traditional Treasury of the same maturity. Using yesterday’s closing numbers – 0.37% for a 10-year TIPS and 2.54% for a 10-year Treasury – you get an inflation breakeven of 2.17%, a fairly attractive number. This means that if inflation averages more than 2.17% over the next 10 years, the TIPS will outperform a nominal Treasury.

Here is a chart showing that the breakeven rate historically tends to fall into the 2.0% to 2.5% range, with rates below 2.0% indicating TIPS are ‘cheap’ and above 2.5% indicating ‘expensive.’ Right now TIPS seem reasonably priced against Treasurys.

This auction: Yes or No? My personal strategy has been to be patient in buying TIPS, not adding lavishly to my holdings while yields are so low. This auction will generate a fairly disappointing yield and come at an above-par price. If it comes in with a yield around 0.30%, that will be lower than the last five 9- to 10-year TIPS auctions. Not good.

This auction: Yes or No? My personal strategy has been to be patient in buying TIPS, not adding lavishly to my holdings while yields are so low. This auction will generate a fairly disappointing yield and come at an above-par price. If it comes in with a yield around 0.30%, that will be lower than the last five 9- to 10-year TIPS auctions. Not good.

Here is a chart of recent TIPS auctions, which shows the yield trend has been on the rise since January 2013. Next Thursday’s auction could seriously break that trend, and I will be sitting this one out.

Dr, it's not clear to whom your comment addressed, nor clear (at least to me, sorry) what it's supposed to…