U.S. inflation continued at a mild pace in May, rising just 0.1% on a seasonally adjusted basis and creating a ‘headline’ inflation rate of 1.4% over the last 12 months. Here’s the summary report.

The non-seasonally adjusted number was 0.2%, resulting in the same 1.4% number over the last 12 months.

Non-seasonally adjusted ‘headine’ inflation – technically called Consumer Price Index for All Urban Consumers (CPI-U) – is important to TIPS investors because it used to adjust the principal balance on Treasury Inflation-Protected Securities and determines future interest rates on US Savings I Bonds.

Energy prices have been a key factor in keeping inflation muted, but the overall energy sector rose 0.4% in May (after strong declines in March and April). However, gasoline prices held steady and fuel oil was down 2.9%. Food prices fell 0.1%, and medical care commodities fell 0.5%. Housing was up 0.3%.

The medical care index has risen 2.2% over the last 12 months, its smallest increase since September 1972.

‘Core’ inflation, which strips out food and energy, rose 0.2% in May after rising 0.1% in both March and April, resulting in 1.7% inflation over the last 12 months, still below the Federal Reserve’s ‘danger’ area of 2.5%.

What’s does it mean? Inflation remains muted, which has two contradictory effects on Treasury Infation-Protected Securities: 1) Investors see little need for inflation protection, keeping a lid on demand for TIPS, and 2) The Federal Reserve will feel no inflationary pressure to slow its bond-buying, which helps lower the yield on TIPS and props up prices.

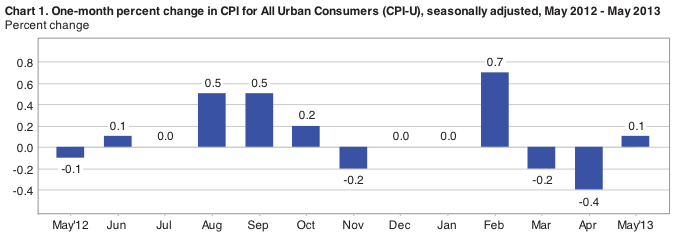

While a rise of 0.1% is mild, it also offsets fear of deflation, which consumers had seen in March and April, when energy prices declined sharply. Here is the trend over the last 12 months:

Here is additional insight from Michael Ashton’s E-piphany blog:

The important part of this CPI report is that CPI-Housing is finally turning up again, as I have been expecting it would “over the next 1-3 months.” Hands down, the rise in housing inflation (41% of overall consumption) is the greatest threat to effective price stability in the short run. Home prices are rising aggressively in many places around the country, and it is passing through to rents. ….

We have not changed our 2014 expectation that core CPI will be at least 3.0%.

Dr Matt....Sell and buy options