Time redemptions to take full advantage of the recent 6.48% variable rate.

By David Enna, Tipswatch.com

First off, before I start talking about redeeming investments in U.S. Series I Savings Bonds, let’s take a moment to ponder just how worthwhile I Bonds have been as an investment over the last several years.

Back in late 2020, before U.S. inflation started surging, I Bonds had a six-month composite rate of 1.68%. That might not sound exciting, but at the time a 13-week T-bill was paying 0.11% and a 10-year Treasury note, 0.68%. The I Bond’s fixed rate of 0.0% was a whopping 83 basis points higher than the negative real yield of a 10-year TIPS.

And then, when inflation began surging into early 2022, the I Bond got a sensational six-month variable rate of 9.62%, towering over the yields of a 13-week Treasury bill (0.85%) and 10-year Treasury note (2.89%).

Through the dire period of pandemic-induced ultra-low interest rates, I Bonds delivered solid returns, tracking U.S. inflation as it soared higher. Investor demand also soared, causing the TreasuryDirect site to crash in October 2022 as the 9.62% rate was about to expire.

In my opinion, I Bonds remain a worthwhile, simple-to-track long-term investment, ensuring your savings will grow tax-deferred with future inflation. But if your investment timeline is shorter-term, you may want to shift money into Treasury bills, where the nominal returns are now 100+ basis points higher. Even if you are investing longer-term, you may want to look at Treasury Inflation-Protected Securities, where real yields are now 70+ basis points higher than the I Bond’s current fixed rate of 0.9%.

I know there are a lot of investors who jumped into I Bonds in October 2022 to get the 9.62% variable rate for six months, followed up by 6.48% for six months. That was a smart move. But now, those I Bonds (which have a fixed rate of 0.0%) are transitioning to a variable rate of 3.38%, well below the market for nominal Treasurys.

Create a strategy

Redeeming I Bonds is a tricky transaction, because an I Bond must be held for 12 full months and then there is a 3-month interest penalty on I Bonds held less than 5 years. Get this wrong and you could lose 3 months of 6.48% interest, or more. For those I Bonds, the best strategy is wait a full 3 months after the 6.48% rate has completed, then redeem early in the next month. That way the penalty will apply to the 3.38% rate.

Here is a guide to the optimal redemption dates for I Bonds purchased since October 2021:

If you bought in October 2021

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 3.54% (annualized) from October 2021 to March 2022

- 7.12% from April to September 2022

- 9.62% from October 2022 to March 2023

- 6.48% from April to September 2023

- 3.38% from October 2023 to March 2024.

- Optimal redemption date: Jan. 1, 2024.

If held until April 1, 2024, this I Bond will have earned an average annual return of 6.01%.

If you bought in November 2021

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 7.12% (annualized) from November 2021 to April 2022.

- 9.62% from May to October 2022.

- 6.48% from November 2022 to April 2023

- 3.38% from May to October 2023

- Optimal redemption date: Aug. 1, 2023

If held until Nov. 1, 2023, this I Bond will have earned an average annual return of 6.64%.

Purchase in December 2021: Optimal redemption date is Sept. 1, 2023.

Purchase in January 2022: Optimal redemption date is Oct. 1, 2023.

Purchase in February 2022: Optimal redemption date is Nov. 1, 2023.

Purchase in March 2022: Optimal redemption date is Dec. 1, 2023.

Purchase in April 2022: Optimal redemption date is Jan. 1, 2024.

If you bought in May 2022

Your I Bond has a fixed rate of 0.0% and is a candidate for redemption.

- It earned 9.62% (annualized) from May to October 2022.

- 6.48% from November 2022 to April 2023

- 3.38% from May to October 2023

- Optimal redemption date: Aug. 1, 2023

If held through Nov. 1, 2023, this I Bond will have earned an annual average return of 6.48%.

Purchase in June 2022: Optimal redemption date is Sept. 1, 2023.

Purchase in July 2022: Optimal redemption date is Oct. 1, 2023.

Purchase in August 2022: Optimal redemption date is Nov. 1 2023.

Purchase in September 2022: Optimal redemption date is Dec. 1, 2023.

Purchase in October 2022: Optimal redemption date is Jan. 1, 2024.

If you bought in November 2022

Your I Bond has a fixed rate of 0.4% and is not a good candidate for redemption if you are holding any other I Bonds with a fixed rate of 0.0%. Redeem those first. For this next series I am using the term “potential” redemption dates instead of “optimal” because the 0.4% fixed rate makes these attractive long-term holdings.

In addition, all I Bonds must be held for 12 months before they can be redeemed. For this series, your future redemption decision may depend on the I Bond’s new variable rate, which will be reset on Nov. 1, 2023.

- It earned 6.89% from November 2022 to April 2023.

- 3.79% from May to November 2023.

- Potential redemption date: Cannot be redeemed until Nov. 1, 2023.

If held through Nov. 1, 2023, this I Bond will have earned an average annual return of 5.33%.

Purchase in December 2022: Potential redemption date is Dec. 1, 2023.

Purchase in January 2023: Potential redemption date is Jan. 1, 2024.

Purchase in February 2023: Potential redemption date is Feb. 1, 2024.

Purchase in March 2023: Potential redemption date is March 1, 2024.

Purchase in April 2023: Potential redemption date is April 1, 2024.

If you bought in May 2023

Your I Bond has a fixed rate of 0.9% and it is not a candidate for redemption. This is an excellent long-term holding. If you need the money and have any other I Bonds with a fixed rate of 0.0%, redeem those first.

In addition, all I Bonds must be held for 12 months before they can be redeemed. For this series, your future redemption decision may depend on the I Bond’s new variable rate, which will be reset on Nov. 1, 2023.

- It is earning 4.3% from May to October 2023.

- The variable rate will reset on Nov. 1, but the fixed rate will remain at 0.9%.

Purchase in June 2023. Potential redemption date is June 1, 2024.

Purchase in July 2023. Potential redemption date is July 1, 2024.

Purchase in August 2023. Potential redemption date is Aug. 1, 2024.

Understanding the pattern

The optimal redemption pattern is consistent for all I Bonds, no matter the year they were purchased. If you bought an I Bond any time within the last 5 years, here are the current ideal times to consider redemptions to minimize the three-month interest penalty:

- January: After Oct. 1, 2023

- February: After Nov 1, 2023

- March: After Dec. 1, 2023

- April: After Jan. 1, 2024

- May: After Aug. 1, 2023

- June: After Sept. 1, 2023

- July: After Oct. 1, 2023

- August: After Nov. 1, 2023

- September: After Dec. 1, 2023

- October: After Jan. 1, 2024.

- November: After Aug. 1, 2023

- December: After Sept. 1, 2023

Here is a chart I created for an article in November 2022 that demonstrates why the optimal redemption dates fall back six months for I Bonds purchased in May and November, when the new six-month variable rate is reset:

What about older I Bonds?

You may want to redeem older I Bonds, held more than 5 years with fixed rates of 0.0%. Of course, there will be no redemption penalty, so you simply want to make sure to complete the full six months of the 6.48% annualized variable rate, and then redeem early the next month. (You earn no interest on an I Bond you didn’t hold through the last day of a month.)

For example, let’s look at purchases for each month of 2017 (the same pattern would hold for other years, but make sure the I Bond truly has a fixed rate of 0.0% before you redeem). Some months are ready to redeem right now, but for some others you will want to wait to complete the 6.48% rate.

- Purchased January 2017. Redeem July 1, 2023.

- February 2017. Aug. 1, 2023.

- March 2017. Sept. 1, 2023.

- April 2017. Oct. 1, 2023.

- May 2017. May 1, 2023.

- June 2017. June 1, 2023.

- July 2017. July 1, 2023.

- August 2017. Aug. 1, 2023.

- September 2017. Sept. 1, 2023.

- October 2017. Oct. 1, 2023.

- November 2017. May 1, 2023.

- December 2017. June 1, 2023.

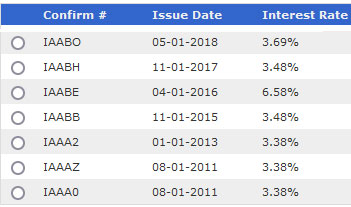

One caution: When you go to redeem an I Bond in TreasuryDirect, finding the correct month-of-issue can be difficult. From your account’s opening page, click on the Series I Savings Bond radio button near the bottom of that page and click “submit.” Then you will see your “Current Holdings” and issue dates.

For an older I Bond — held more than 5 years — look for the I Bonds listed with an interest rate of 3.38% — the current variable rate combined with a 0.0% fixed rate. That older I Bond is safe to redeem.

In this example, the lower three I Bonds have a fixed rate of 0.0% and have transitioned to the 3.38% interest rate. Those can be priorities for redemption. The others all have a better fixed rate and one is still paying 6.58%. Those are not the ones to sell first.

A reminder about taxes

When you redeem any savings bond, you are taking money out of a tax-deferred investment and you will immediately owe federal income taxes on your interest earnings. If you are doing a large number of redemptions, you could climb into a higher tax bracket or potentially trigger Medicare IRMAA surcharges.

An example: Let’s say you want to redeem $10,000 in an 0.0% fixed rate I Bond issued in May 2017. As of August 1, that I Bond had a value of $12,400, so if you redeemed today that decision would create taxable income of $2,400. If you are in the 22% tax bracket, the federal income tax would be $528.

You can easily check the current value of any I Bond using TreasuryDirect’s Savings Bond Calculator (which will automatically subtract 3 months interest for I Bonds held less than five years) or at EyeBonds.info, an accurate and extremely useful resource for information on I Bonds and TIPS.

Final thoughts

I am not advocating selling out of I Bonds. These savings bonds remain a very safe way to push inflation-protected cash into the future.

But I also don’t see the need to hold I Bonds for 30 years. As you enter retirement years, it makes sense to consider redeeming I Bonds to supply cash when you need the money. Or, for people with a shorter-term view, to switch to a more attractive near-term investment like a 1-year T-bill. Or, to use proceeds from a 0.0% I Bond to roll into a new I Bond investment with a 0.9% fixed rate, possibly using the gift box strategy.

As you ponder redemptions, remember to first target I Bonds with 0.0% fixed rates. And for I Bonds held less than 5 years, wait until you’ve transitioned into the 3.38% interest rate for a full three months.

If you got this far … This article contains a lot of numbers, months and years, subtracting six months here and not there. If you spot any errors, post them in the comments area and I will thank you and make a fix.

• I Bonds: A not-so-simple buying guide for 2023

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Dr, it's not clear to whom your comment addressed, nor clear (at least to me, sorry) what it's supposed to…